Asia| Nov 10 2025

Asia| Nov 10 2025Economic Letter from Asia: As the Dust Settles

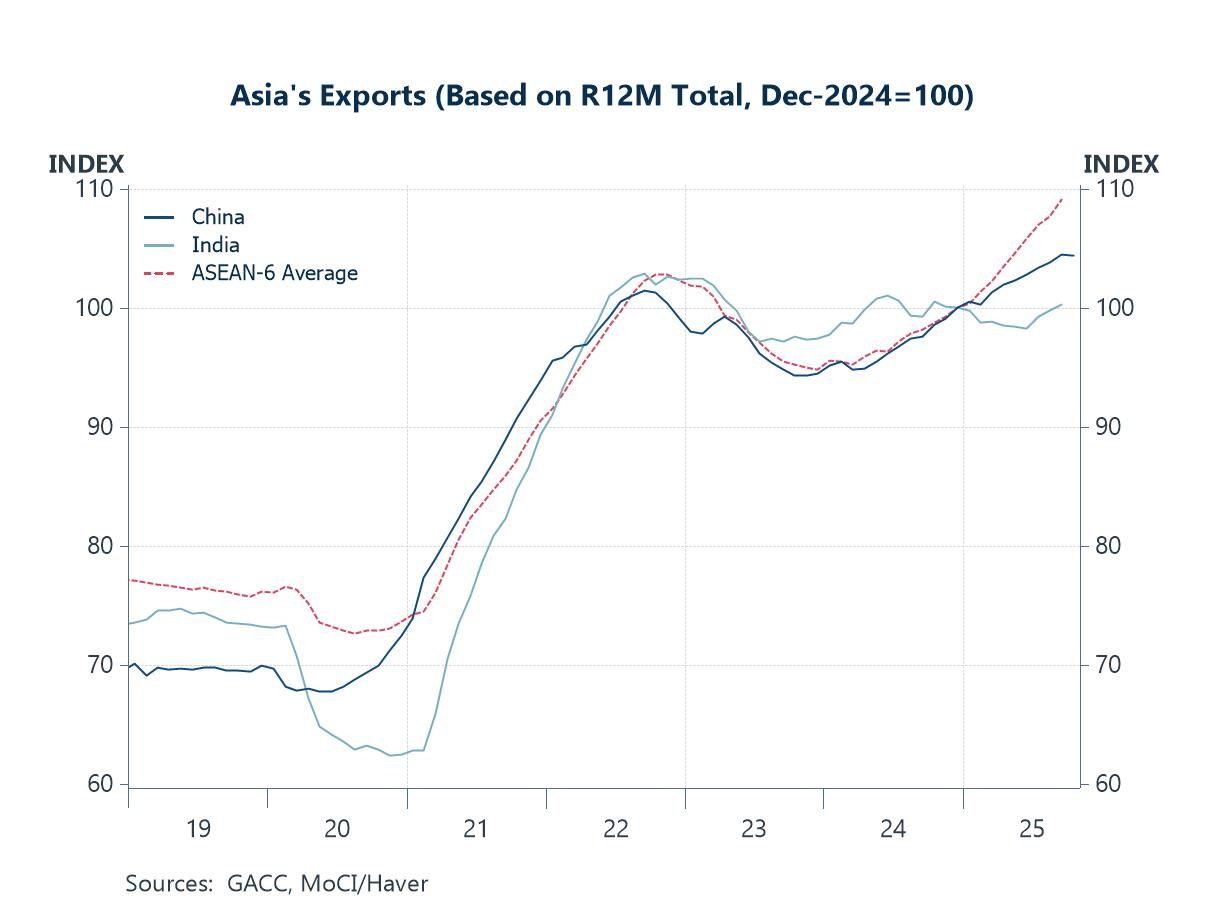

This week, we review key developments across several Asian economies as the year nears its close. On balance, many of investors’ and policymakers’ worst fears did not materialize. Despite US tariffs, regional exports have shown resilience (chart 1), partly supported by stronger intra-Asia trade, even as exports to the US declined in some cases.

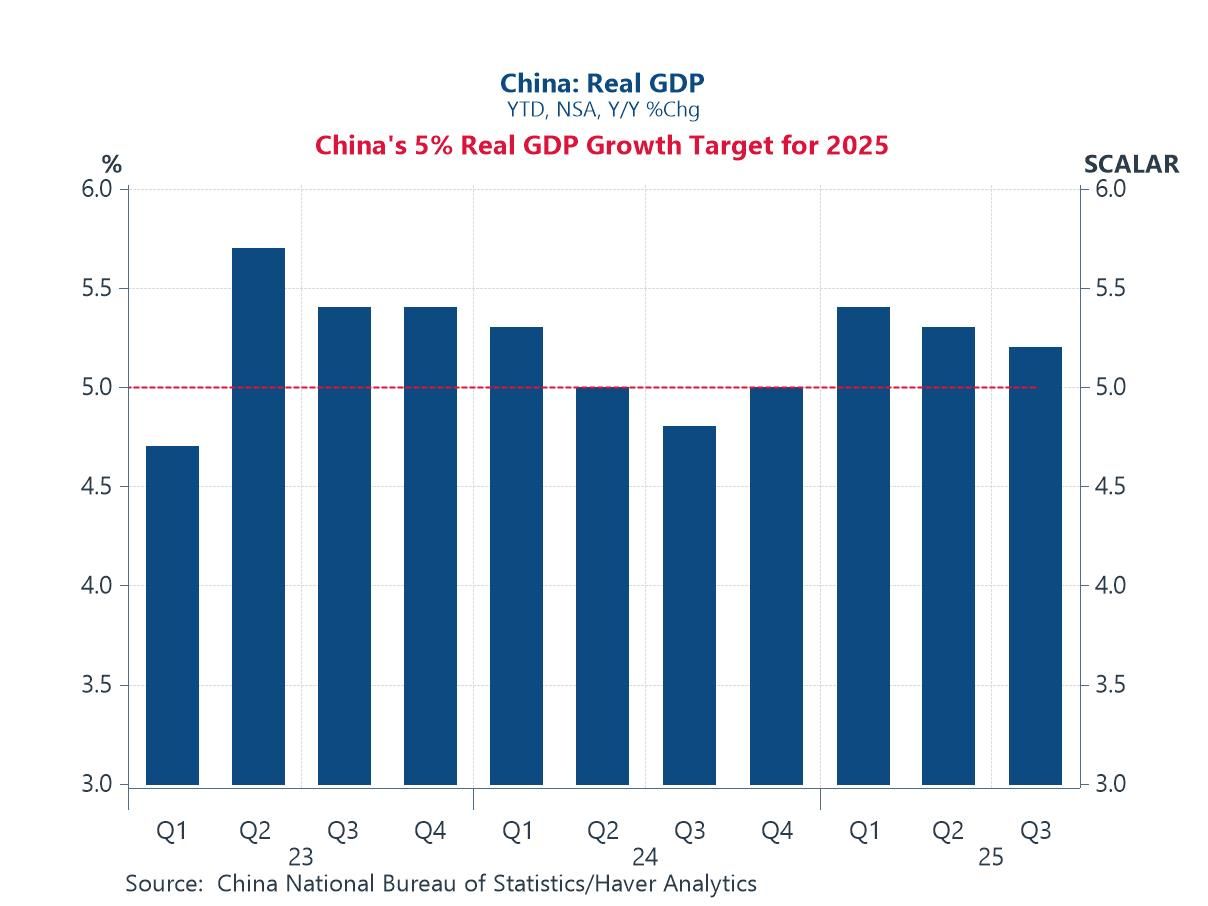

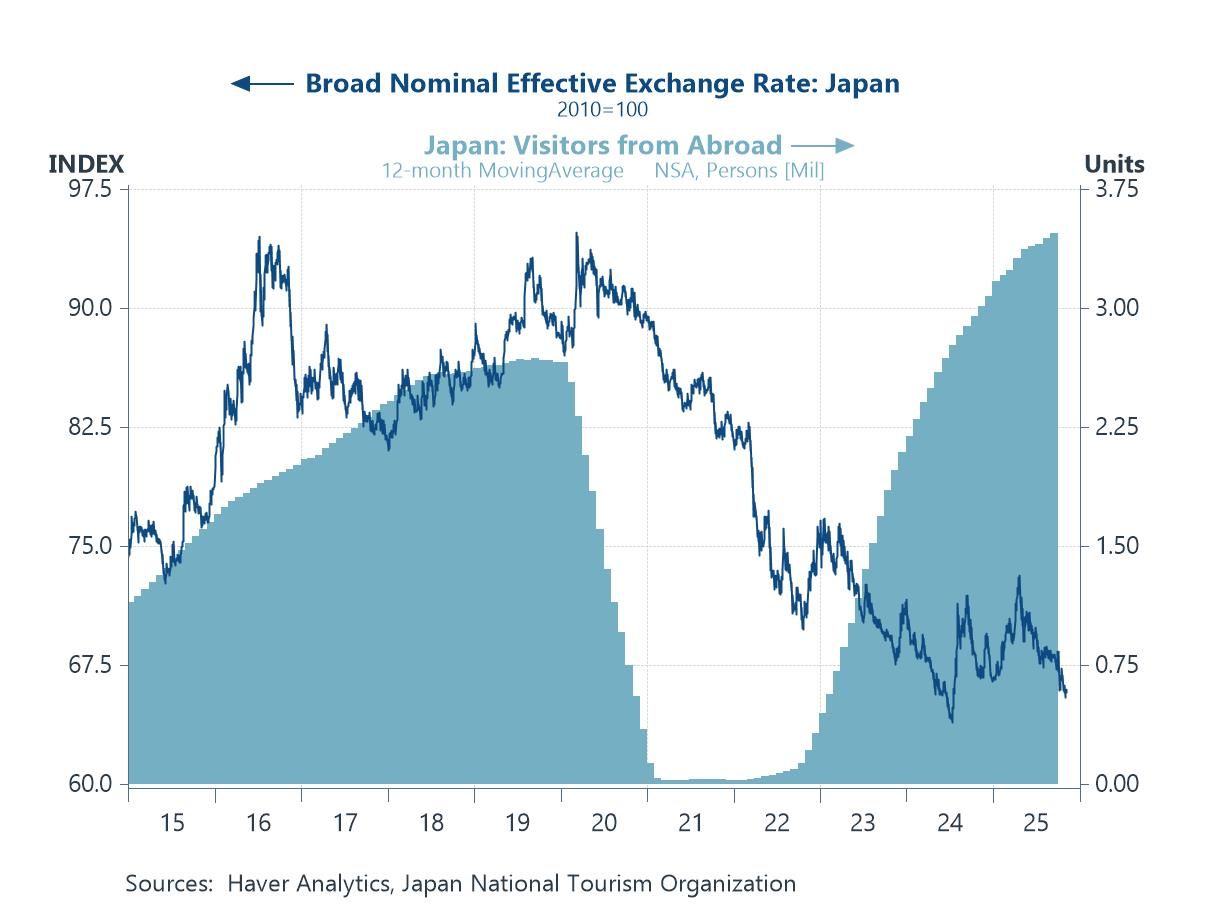

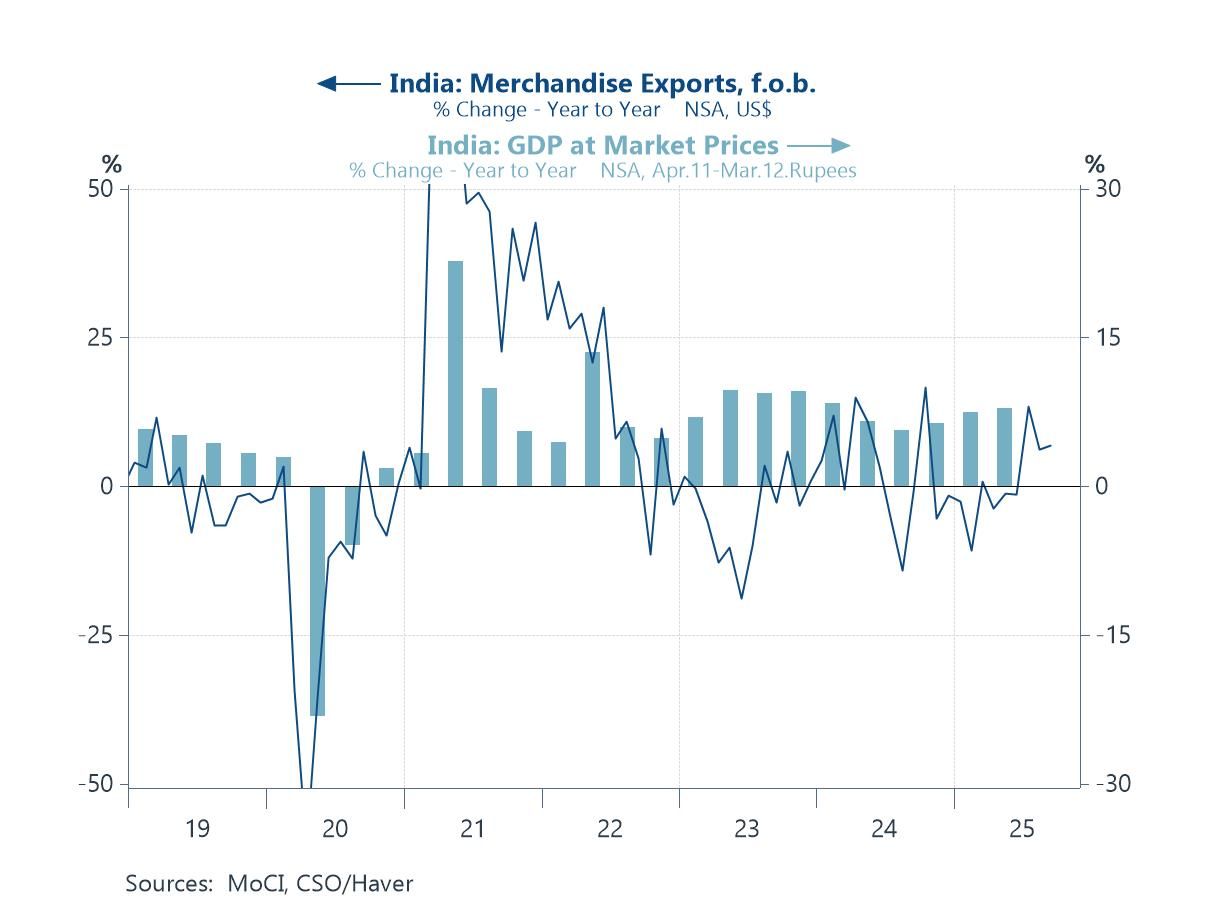

In China, factors including importer front-loading, stronger exports to non-US markets, and government efforts to boost consumption—albeit with potentially one-off effects—have kept the economy on track to meet its 5% growth target this year (chart 2), barring a substantial slowdown in Q4. In Japan, political uncertainty has eased following Prime Minister Takaichi’s rise, though her pro-growth, pro-loose monetary stance has contributed to further yen weakness (chart 3). India, while still likely Asia’s fastest-growing major economy this year, has seen trade setbacks (chart 4) as US–India discussions continue, though recent progress suggests a deal may be near.

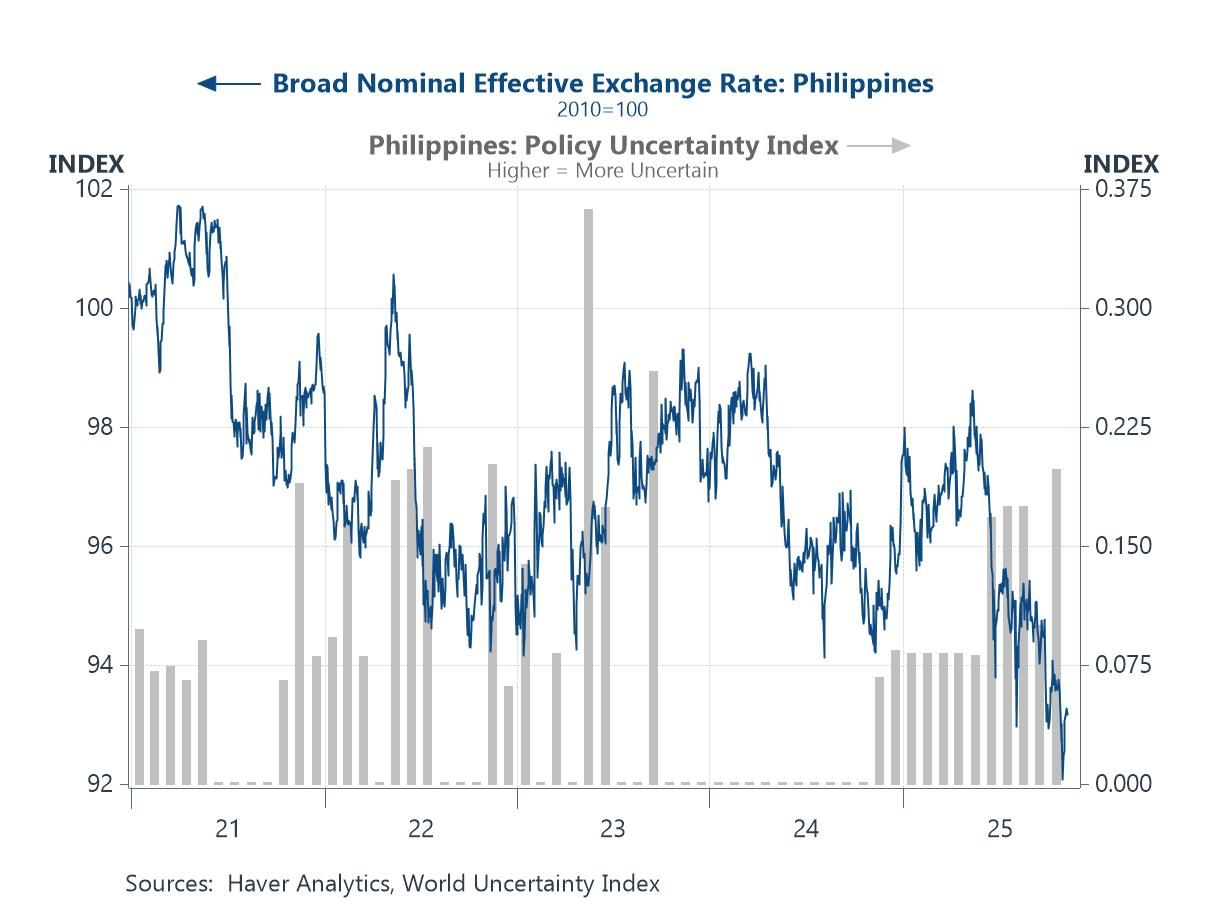

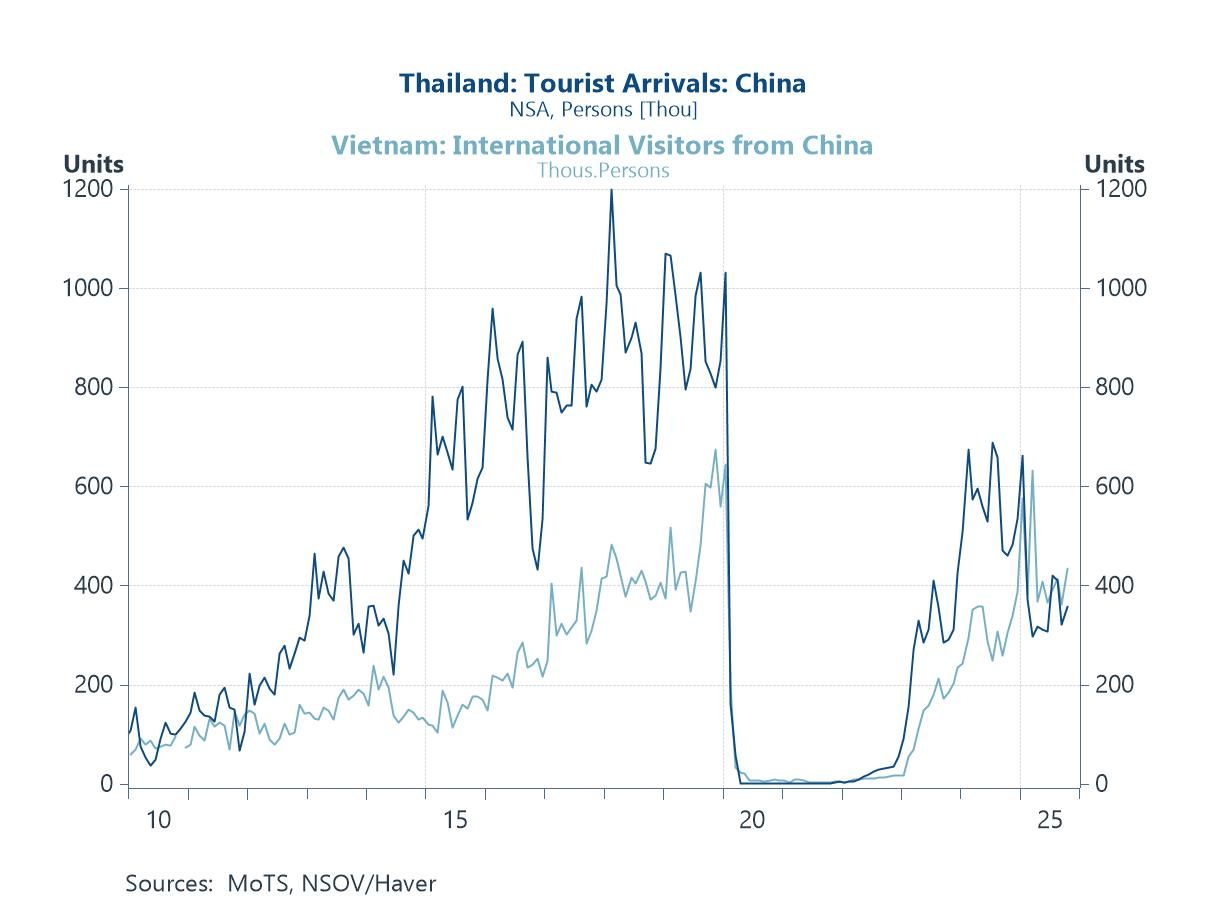

However, not all developments in Asia have avoided worst-case outcomes. For example, the Philippines, which has already been hit by a string of storms this year, continues to reel from the effects of Typhoons Fung-wong and Kalmaegi. These storms have highlighted corruption in the Philippines’ flood control systems, rattling investors and pressuring the peso (chart 5), in a manner reminiscent of the rupiah’s decline during Indonesia’s political turmoil earlier this year. In Thailand, political uncertainty continues ahead of general elections eyed at next March, while the expected full return of Chinese tourists has yet to materialize (chart 6).

Trade in Asia For Asia, the year has ultimately not played out as bleakly as investors once feared, particularly on the trade front. Despite US President Trump’s tariffs and a persistent backdrop of uncertainty, export performance in several Asian economies has proven more resilient than expected. This is most clearly reflected in export growth readings for China and key Southeast Asian economies (chart 1), which have remained firm—and at times exceeded expectations—even as China’s shipments to the US fell sharply. Much of this resilience reflects a redirection of exports toward other markets, often within the region. India, however, has seen more limited gains, with exports in US dollar terms struggling to materially surpass last year’s levels.

Chart 1: Asia’s exports

China Among the main investor concerns earlier this year was China, which once again came under close scrutiny as President Trump sought to address issues ranging from the large US–China trade imbalance to intensifying AI competition and perceived overcapacity. Yet China’s growth—particularly on the export front—has proven more resilient than expected, with increased shipments to other markets more than offsetting reduced trade with the US. Earlier front-loading by importers ahead of anticipated tariff hikes also temporarily supported export figures. Domestically, government initiatives to stimulate consumption led to a brief lift in retail spending, though signs suggest these effects may be fading, indicating their largely one-off nature. Even so, China has maintained year-to-date growth above its 5% annual target (chart 2), keeping that goal within reach provided momentum does not weaken significantly in Q4. Meanwhile, the more conciliatory tone in recent US–China discussions, including the halving of US fentanyl-related tariffs, offers a modest further relief. That said, longer-term structural issues still loom, including the difficult shift toward a more consumption-led economy, demographic pressures, and questions around sustained overcapacity in key industries.

Chart 2: China’s year-to-date real GDP growth

Japan In Japan, the political uncertainty that followed the Liberal Democratic Party’s weak election performances earlier in the year has largely eased with Takaichi’s appointment as the country’s first female Prime Minister. Attention now turns to her supplementary budget—reported to be around $65 billion—which aims to address the rising cost of living while also bolstering defence and diplomatic capabilities. Investors, however, are already contemplating the policy implications. In particular, expectations that Takaichi’s agenda could make it harder for the Bank of Japan to pursue further significant tightening have added renewed pressure on the yen, pushing it to multi-year lows (chart 3). And while a weaker yen could, in theory, support tourism, forthcoming measures to curb overtourism—such as Kyoto’s planned 900% increase in accommodation taxes—may act as offsetting factors.

Chart 3: Japanese yen and visitor arrivals to Japan

India Turning to India, the economy remains on track to be the region’s fastest-growing major economy. Growth forecasts were downgraded earlier in the year by the IMF and Blue Chip survey panellists, but these revisions were later reversed. These early-year downgrades reflected India’s heavy exposure to US trade, a concern that materialized when the US raised its reciprocal tariff rate on India from 25% to 50%. This contrasts with the situation of many other Asian economies, who successfully negotiated lower rates below the “Liberation Day” baseline. Although India managed to expand exports to other trading partners, this gain resulted in only a muted net impact on overall exports and, in turn, GDP growth. That said, US–India discussions have made some progress over the year, particularly on previously contentious issues such as India’s purchases of Russian crude. While these developments bring India closer to a potential trade deal, the benefits are likely to materialize beyond this year, meaning current growth readings still largely reflect the impact of the steep US tariffs in place today.

Chart 4: India exports and GDP growth

The Philippines Moving to the Philippines, the country is grappling with the impact of Typhoon Fung-wong, which struck the northern regions on Sunday, forcing over a million people to evacuate and causing widespread landslides and damaged roads. Fung-wong follows a string of storms this year, including Typhoon Kalmaegi, which also inflicted substantial damage just a few days ago. The disasters have reignited concerns over longstanding corruption in the country’s flood control systems, spooking investors and prompting capital outflows, which have weighed on the Philippine peso (chart 5). The currency’s weakness has been compounded by the central bank’s ongoing easing, which has cut the policy rate from last year’s peak of 6.5% to 4.75%—nearly 200 basis points—and with markets still pricing in further cuts.

Chart 5: The Philippine peso and policy uncertainty

Thailand Lastly, Thailand’s economy continues to struggle to regain the footing it had before the pandemic, weighed down by both domestic and external factors. Politically, the country remains in a transitional phase, with new Prime Minister Anutin under scrutiny to deliver on his pledge to hold general elections soon. Deputy Prime Minister indications suggest March 29, 2026 as a likely date, leaving a period of uncertainty in the meantime, as the durability of policies enacted during this interim phase remains unclear. Externally, tourism—which should have been a key growth driver—has underperformed, as the return of Chinese visitors to pre-pandemic levels did not materialize, partly due to tourism-related scares. In contrast, Vietnam appears to have captured a larger share of Chinese tourists this year (chart 6).

Chart 6: Thailand and Vietnam tourist / visitor arrivals from China

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief