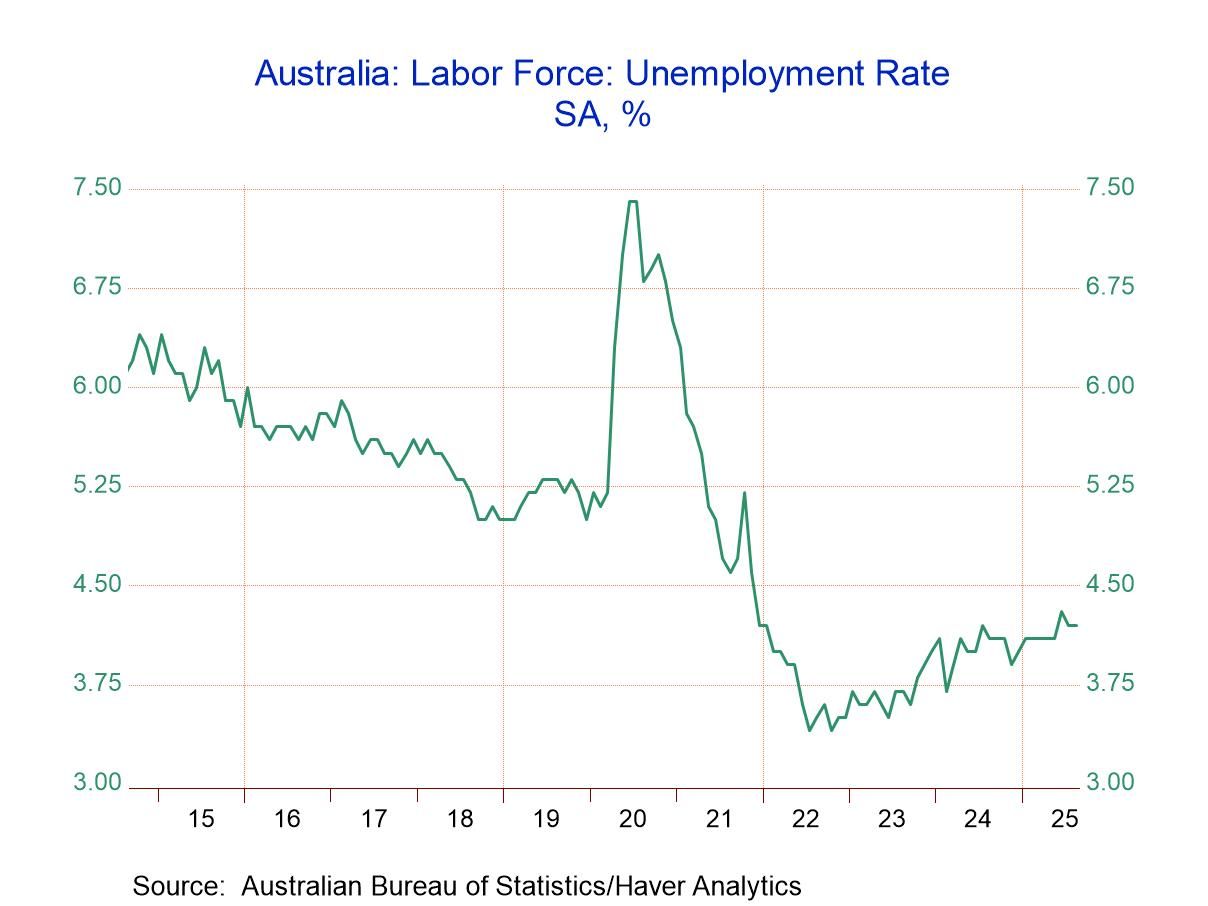

Australian Unemployment Steady and Low Despite a Broader Rising Trend

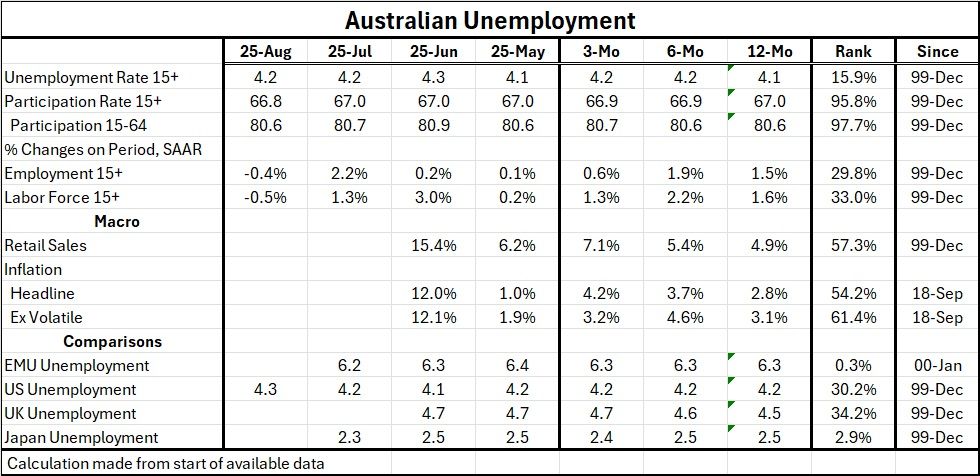

Unemployment in Australia in August remained low, standing at 4.2%, the level it dropped to in July. June brought a rise in unemployment to 4.3% after posting 4.1% in May. However, at 4.2% the unemployment rate in Australia is low, since about 2000 the unemployment rate has been lower only about 16% of the time.

The labor force participation rate in August fell to 66.8 from 67.0 where it had been for the previous several months. The participation rate, however, is high on historic comparison at about the 95th percentile; the participation from people ages 15 to 64 is even higher with a 97.7 percentile standing on the participation rate of 80.6%.

However, employment gains in Australia have been slowing. The year-over-year gain is 1.5%, over six months, employment speeded up, gaining a pace of 1.9% at an annual rate, but over three months the growth rate for employment has fallen to a sharply lower 0.6% annualized.

Australia's labor force fell by 0.5% in August after rising robustly in previous months. The labor force was rising by 1.6% over 12 months, at a 2.2% annual rate over six months and at a 1.3% annual rate over three months. There's been some variability in labor force growth, but it still seems to be relatively solid. The year-over-year growth rate, however, has a ranking only in its 33 percentiles historically back to the year 2000- a lower one-third standing.

In terms of the overall economy, retail sales have picked up; some of this is inflation. The growth rate for retail sales over three months is 7.1%; over 12 months it's 4.9%. Headline inflation grew by 2.8% over 12 months, but it's rising over three months at a stronger 4.2% annual rate. Inflation excluding volatile measures has been relatively stable over three months, six months, and 12 months. However, it picked up quite considerably in June, rising at a very rapid double-digit pace.

Australia's low and consistent unemployment rate is in step with what's going on internationally. Globally there is stability or some small backtracking on unemployment gains made since COVID. In the European Monetary Union, we're looking at unemployment rates consistently low over 12 months, 3 months, and 6 months at a historically low level. Japan's unemployment rates are consistent and low near historically low levels as well. In the United States and in the United Kingdom, unemployment rates are relatively stable. The U.K. shows some drift up in its unemployment rate. But both the U.S. and the U.K. have unemployment rates that have been lower only about 30% of the time.

Globally unemployment rates remain low. Inflation remains slightly over target in most countries that target inflation. Inflation is more stuck at a percentage point or so above the target rate than accelerating. However, inflation has been excessive for some time and central banks generally are not taking steps to rein in inflation. Instead, they seem to take the policy tack that they're going to continue to cut rates and they're going to forecast that inflation is going to fall in the period ahead.

This is more monetary policy by wishful thinking than it is Keynesianism or anything else- that's for sure. Whether it's going to pay off, we're going to have to keep an eye out for that. But with U.S. tariffs in place, we certainly expect U.S. inflation to be rising and perhaps rising faster with the Federal Reserve getting ready to cut rates more rapidly than it was earlier.

So far, the tightness in global labor markets hasn't created any backlash on the inflation front or substantial increases in domestic wage rates. However, that might be something to pay attention to as we look ahead. Since central banks have taken the policy tact that they will forecast lower inflation rates rather than do things to make them come true, it makes sense to be somewhat more vigilant about what happens on the inflation front.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global