Global| Jul 16 2020

Global| Jul 16 2020EMU Trade Surplus Is Back in Style; What's Next? Spin the Wheel of Misfortune!

|in:Viewpoints

Summary

The coronavirus has distorted everything and that is not going to stop. It is also hard to tell what kind of rebound to expect and once we get one to tell if it will last. This is because of the hokey-pokey policy of deferring to the [...]

The coronavirus has distorted everything and that is not going to stop. It is also hard to tell what kind of rebound to expect and once we get one to tell if it will last. This is because of the hokey-pokey policy of deferring to the virus. You shut the economy down; you open the economy up. You damp the virus down, then you spread it all around…It's the virus hokey pokey! It creates a back and forth motion that gyrates and reverberates and cascades across the economic landscape making waves of infection and withdrawal but no clear progress. Without a vaccine or herd immunity (which almost no one is trying to get) this is going to go on and on. For this reason, I am skeptical about engaging in a lot of discussion about 'trends.' Trends in economics are important. But right now, we cannot be sure if today's trend is a lasting trend or a fad soon to be swamped by the next corona twist and turn.

The coronavirus has distorted everything and that is not going to stop. It is also hard to tell what kind of rebound to expect and once we get one to tell if it will last. This is because of the hokey-pokey policy of deferring to the virus. You shut the economy down; you open the economy up. You damp the virus down, then you spread it all around…It's the virus hokey pokey! It creates a back and forth motion that gyrates and reverberates and cascades across the economic landscape making waves of infection and withdrawal but no clear progress. Without a vaccine or herd immunity (which almost no one is trying to get) this is going to go on and on. For this reason, I am skeptical about engaging in a lot of discussion about 'trends.' Trends in economics are important. But right now, we cannot be sure if today's trend is a lasting trend or a fad soon to be swamped by the next corona twist and turn.

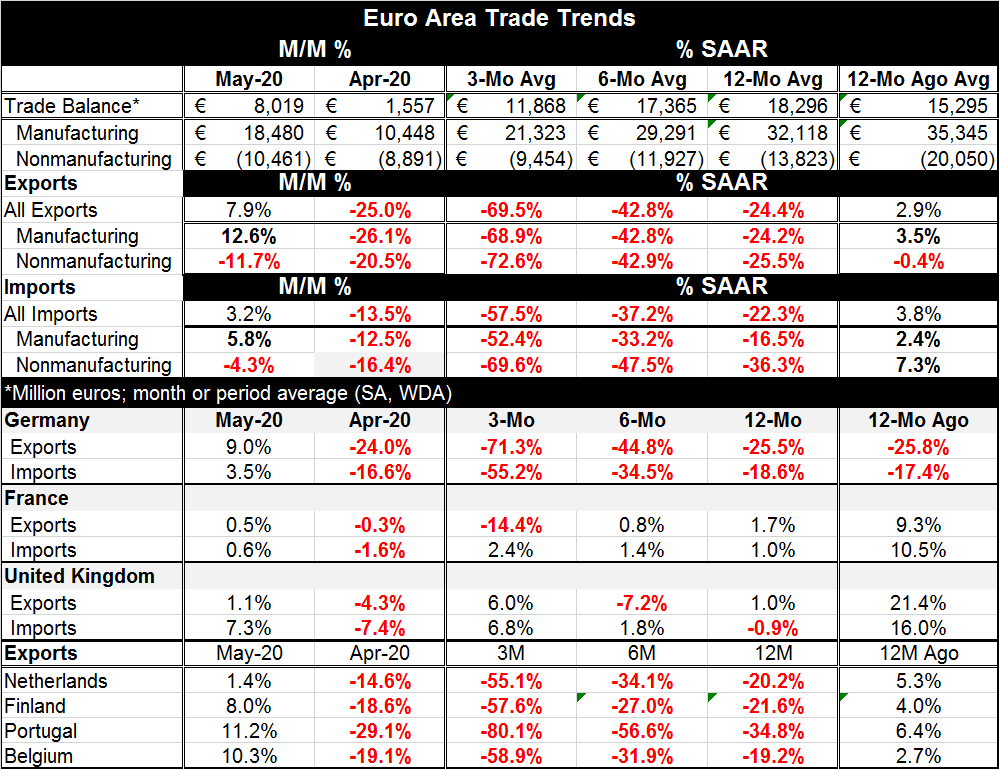

Corona responses slammed the EMU trade surplus in April, dropping it to €1.6bln from €26.0bln in March. Now in May, it is back up to €8.0bln. Ignoring last month, it is still the smallest surplus since May 2012 – a decade ago. Still, it's a rebound. But we do not know if it will last- if the improvement will continue or not. We simply do not know because the path of the virus is impossible to work out and a decision has been made to avoid it and not to 'brave it' – except of course in Sweden.

Fear trumps infection

I keep pumping these numbers out so that someone might latch onto them. Jim Bullard, President of the St. Louis Fed, has just given a presentation citing how exaggerated the virus risk has been and he is projecting better growth in the second half of the year because of it. Will things really go back toward normal quicker as Jim says? Probably not. These numbers and trends are NOT NEW. I have been promoting these same numbers for a long time and they simply do not resonate with anyone in 'power.' The Dr Fauci's of the world have scared everyone to death and there is now fear which can be worse than actual infection.

The true risks

Let me present some virus statistics. I will use NYC data. Why, you say, use NYC data in an article about EMU and EMU trade? The answer is simple: the virus is essentially the same everywhere and NY city has a set of data that are very complete and that highlight several important characteristics of the virus that NO ONE LOOKS AT. Dr Fauci has NEVER uttered a word about the most important aspect of the NYC data. And those data offer a way out of the crisis. So please take a moment to assimilate these data and their meaning.

A lesson from NY

In a City of 8.8mln through July 15 of 2020… 18,734 people had been declared dead because of the coronavirus. Of these 16,451 had at least one significant preexisting illness. An additional 2,177 died with unknown medical histories. In NYC over a period of 6-months the coronavirus killed 105 (one hundred and five, to repeat for accuracy) previously healthy people in NY (data source here).

This is a smaller number than the number of traffic-related deaths in NY over such a period. The coronavirus has been LESS RISKY to healthy people in NYC than crossing the street! And for this, 'they shut down the greatest city in the world' and it continues on a path to ruination. Why are these data and their clear implication that economies SHOULD NOT BE SHUT DOWN ignored? Why are not resources devoted to protecting those people with preexisting conditions who are at risk (40% of U.S. deaths nationwide are at nursing homes)? Why do we encourage anyone who is 'afraid' to stay at home? Why is the tracking of a spread in infections the litmus test of danger when infecting healthy people has less risk than crossing the street AND it advances progress toward herd immunity? Who is advancing this agenda? Why are the facts that underlay any science being ignored by those who demand that we follow the science? Simply put why do heath officials ignore the fact- FACT- that healthy people are really not at much risk of dying at all?

EMU trade- what to think

Well, those are good questions, but for now they will go unanswered. We can see EMU-area trade is being affected. And while there is some rebound this month, we have no way of knowing if the data will stay on some sort of 'recovery path or not' because the virus and the reaction to it is unpredictable.

EMU data show exports and imports both rising in May on relatively strong monthly gains but gains that are twice as large for exports as for imports (7.9%> 3.2%). We also see that 'recovery' seems to be an artifact of manufacturing where export gains again are about twice those of import gains (12.6%> 5.8%). Both exports and imports show ongoing decline for nonmanufactured goods with (of course) export declines larger than import declines for nonmanufactures (-11.7%< -4.3%).

Sequential growth rates do not show any turn in trend with three-month declines larger than six-month declines that in turn are larger than 12-month declines for each of these categories in the case of both exports and imports. We cannot be sure what these trends mean or if they are really about to turn. But some turning or blunting of them does now seem likely based on the sharp turn of the May results.

Turning to country data, we find Germany and France with the same trends as those above with the exception that French import growth is actually positive and accelerating on a sequential basis. German export and imports sequentially deteriorate. Both German and French exports and imports rise in May. German exports in May are more than twice as strong as German imports; not so for French exports vs. imports.

The United Kingdom has its own idiosyncratic trends. But the trends for exports in the Netherlands, Finland, Portugal and Belgium all follow the EMU pattern for overall exports.

The fact that the EMU trends seem to carry through to many EMU members gives its result a greater veracity but still does not give us any more or less confidence in how the trend turns next. Trade has been greatly affected by the pandemic if this really is one. The fear and reaction to infection outbreaks have massive effect on global growth and therefore on global trade.

Let me share one last report on the virus that emphasizes how dangerous our current approach to it has become. This is an actual Reuters news story.

"Canada's efforts to flatten the curve of coronavirus cases have put the country on the cusp of zero deaths from COVID-19 for the first time since March, but officials see worrying signs of a new spike as provinces lift restrictions" (source here).

According to this news report, Canada's success has flattened the infection curve and stopped deaths. But now as Canada gets ready to reopen, there are concerns of reinfection...so? Does this turn victory into the fear of defeat? Every time a country reopens there is new infection. According to this story, when we are at the apex of success (no deaths), we are also at the brink of failure since economies are getting ready to open up and the infection process will restart. Has anyone stopped to think how devilish this is? How undermining to our mental health? How, well, preposterous this is as a public health policy? And all that is quite apart from the massive collateral damage the shutdown has had on people's economic lives and their heath (5.4mln Americans just lost health care because of CV caused job losses). I am beside myself trying to make sense of it. This is not only because the policy makes no sense in medical terms; this policy simply is not logical. But this is where we are today and this is what public health protocols have become and that is why no economist can forecast anything, let alone EMU trade flows.

Viewpoint commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.