Global| Mar 17 2020

Global| Mar 17 2020Zew Zig Zags Toward Zilch; Zew and What to Do

Summary

Welcome to the wild wacky world of economic analysis during a global contagion with national policies slamming the brakes on at different speeds to head off the spread of the virus in different regions around the globe. As you can see [...]

Welcome to the wild wacky world of economic analysis during a global contagion with national policies slamming the brakes on at different speeds to head off the spread of the virus in different regions around the globe.

Welcome to the wild wacky world of economic analysis during a global contagion with national policies slamming the brakes on at different speeds to head off the spread of the virus in different regions around the globe.

As you can see in the Zew report, the corona backlash is finally being captured in Western data. We already saw Chinese data register a plunge in China’s PMI index. But until the last few days, western data releases have been whistling past the grave yard. Well, no more is that the case. Not all reports are affected, but the Zew report is a survey of the opinions and perceptions of financial experts; it is on top of the breaking news.

Current conditions developments

In February 2019, the euro area began to register a negative current macroeconomic assessment. At that time, the United Kingdom, France, and Italy were negatively assessed. And they had been negative through most of the post financial crisis period. But in February the EMU assessment turned negative in July 2019 Germany turned negative and in the current report for March 2020 the U.S. has just dropped to a negative assessment from +48.1 last month, a stunning one month drop. Still, after turning negative in February 2019 conditions deteriorated to an October/November local low then began to improve. For example the EMU reading bottomed in 2019 at -26.4 in October and improved to -9.9 in January slipping only very slightly to -10.3 in February before being crushed in this report at a reading of minus 48.5 as the impact of corona began to register.

The clear message is that the Zew experts that in the wake of the U.S.-China trade deal conditions were improving or were expected to improve. Instead, the virus came it spread for a while it was denied and now its impact is undeniable, ubiquitous, and bad.

Macroeconomic expectations

Macroeconomic expectations changed more or less parallel with the experience of current conditions. In April 2018 macroeconomic expectations turned to negative readings across most of the countries in the table. By June the U.S., Japan and France also took on negative readings joining the rest of the pack. Macro-expectations were hard hit in December 2018 and for many that was their low reading at the time; a few countries slipped to lower readings still in January or February of 2019. There was a revival though April-May and then a worsening to new low readings for this episode around August. The movements largely followed U.S.-China trade news. By December with a U.S.-China Phase-One trade deal pending the euro area, Germany and Japan shed their negative readings. The U.S. shed its negative reading in February. And that was just in time for all of these countries to see macroeconomic expectations tank to low readings in March 2020, in the current report. The one-month change is astonishing.

Inflation

Inflation expectations readings also have cycles to some extent, but inflation expectations now are at extremely weak readings in March across the board.

Interest rates

Short-term interest rate expectations that eroded slightly and unevenly in February have plunged in March. There are now large negative expectations across the board. Long-term interest rate expectations are weaker across the board with negative assessments everywhere except in Germany where fiscal stimulus is expected and that has lifted rate expectations there on balance.

Stocks

Oddly with stock markets in total pandemonium and much of the recent extreme selling probably coming AFTER these surveys were filled in, the Zew experts had become quite positive on the outlook for equities in March. Oddly they also apparently foresaw a Russia-OPEC oil deal (that did not happen) since they also have oil prices expected higher when in fact both WTI and Brent oil grades have recently traded below $30/barrel.

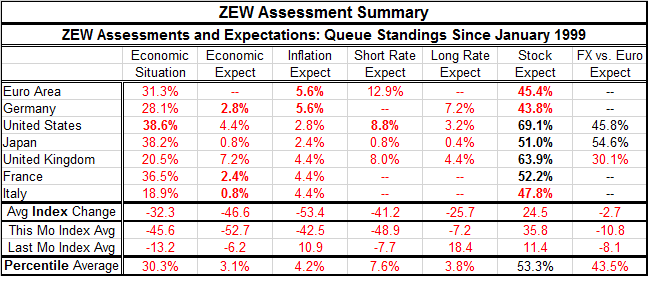

Percentile standings

The table below registers percentile standings of the underlying diffusion survey data. It was the diffusion data I cited in the above paragraphs. The percentile rankings assess and rank the diffusion readings in a queue of data back to 1999 to give the current readings perspective.

The economic situation averages an unweighted 30.3 percentile reading in March. That means that the average reading in March is historically lower only about one-third of the time. That is a very weak marker. The U.S. and Japan have the ‘best’ relative current standings at a 38th percentile standing for each; France is at a 36.5 percentile standing compared to all of EMU at a 31.3 percentile mark. Italy and the U.K. have the weakest standings at 18.9% for Italy and 20.5% for the UK.

Economic expectations are so pathetically weak; there is not much point talking about who is doing better since all the rank standings are in the lower 10th percentile cohort. While the current economic index average fell by 32 points month-to-month, the macro-expectation index fell by 46.6 diffusion points to an average percentile standing of 3.1% - rarely ever lower.

The inflation expectation average fell by even more diffusion points in March shedding 53.4 points to fall to a 4.2 percentile standing average across members. Inflation is not on the radar and not even in the dictionary freeing policy to take whatever aggressive measures it may choose.

Short-term interest rate expectations fell by 41.2 diffusion points on average while long-term rates fell by 25.7 on average. Short-term rates have an average standing at their 7.6 percentile compared to long-term rates with an average standing at their 3.8 percentile.

Stocks have this odd reaction based on the dissonance between the Zew expectations and what stock markets have been doing over the last five trading sessions (falling!). However, Zew financial experts have four of seven stock markets with percentile standings above their historic medians (above a rank of 50%) with no index rated weaker than a 43.8 percentile standing.

This will be an INDUCED recession

The main point to bear in mind is that there is a recession coming that will be caused by these various national polices. The virus is NOT causing the recession. The recession is being caused by programs put in place by governments to mitigate the spread of the virus. This is a self-induced recessionary process. As such, it is controlled. I read some articles in which people talk of this cascading to a depression. Since this is like a controlled burn that is not likely, but a thing like this can always spin out of control. Still, policy is still in control of this modulation and so far the early imposition of these measures internationally and with different degrees in different countries makes it unlikely that a doomsday scenario would take hold. Also policy is geared to try to and mute economic knock-on effects. There are safety nets for people, for business, and medical care. Few crises ever come with such mechanisms put in place before the crisis becomes severe. All indications are that in most places governments are ahead of the curve. Italy and Iran are struggling the most internationally, but Italy’s clamp down is slowing the spread and showing progress.

The downturn may be severe, but it will be limited and reversible

My recommendation is to view this as a temporary and ‘soon to be reversed’ policy period. It is still open-ended. No one knows how long it will take. But the more that people respect the mitigation protocols, the sooner this will end and when it does the economic fabric should be in good shape and growth should return more or less on path. When restaurants reopen, people will eat there. When sports events are on, people will attend again. When travel is allowed, people will drive, fly and take trains. But as long as those activities are closed, those actions are confined to zero or near-zero activity. That is the fact of the induced recession.

No room for conventional monetary and fiscal stimulus

Another fact is that governments can issue policies to mitigate the adverse impact on growth. But that is all. Policies can mitigate. They cannot reverse since the medical protocol policies themselves are meant to reduce contact among economic agents; that slows growth. So governments can reduce the pain of this process on people and prepare to keep the economic fabric strong so that growth can progress back to normal once –once- that is feasible. Conventional macroeconomic monetary and fiscal policies are not useful because they work to stimulate output and spending in general and many of those activities have been purposefully shut down by policy. Fiscal actions should be targeted and calibrated not across the board. This is should be a hands-on process not a process run on the advice some now malfunctioning statistical model.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief