Global| Nov 12 2019

Global| Nov 12 2019ZEW Survey: Sharp Revival in Expectations

Summary

The ZEW survey in November has month-to-month increases in most macroeconomic, interest rate and stock market readings. But it is not just this breadth that is impressive; it is the breadth on top of a strong change in individual [...]

The ZEW survey in November has month-to-month increases in most macroeconomic, interest rate and stock market readings. But it is not just this breadth that is impressive; it is the breadth on top of a strong change in individual expectations. While the average expectation in the ZEW survey has only a 21st percentile standing, all six surveyed countries show month-to-month improvements that were so large that they have only been greater 4% of the time or less across each surveyed participant. On data back to 1991, there were only two-months - and those were nearly back-to-back in 2009 when the global economy was reviving from a deep recession- when the average ranking on the monthly change in macroeconomic expectations was greater than it is this month for these six countries: Germany, the United States, Japan, the United Kingdom, France and Italy.

The ZEW survey in November has month-to-month increases in most macroeconomic, interest rate and stock market readings. But it is not just this breadth that is impressive; it is the breadth on top of a strong change in individual expectations. While the average expectation in the ZEW survey has only a 21st percentile standing, all six surveyed countries show month-to-month improvements that were so large that they have only been greater 4% of the time or less across each surveyed participant. On data back to 1991, there were only two-months - and those were nearly back-to-back in 2009 when the global economy was reviving from a deep recession- when the average ranking on the monthly change in macroeconomic expectations was greater than it is this month for these six countries: Germany, the United States, Japan, the United Kingdom, France and Italy.

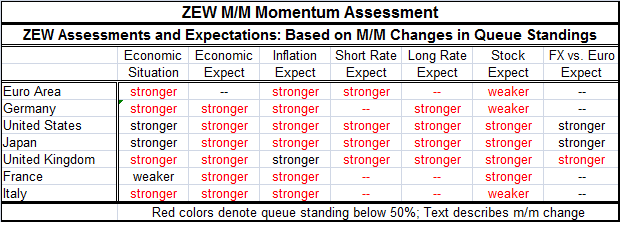

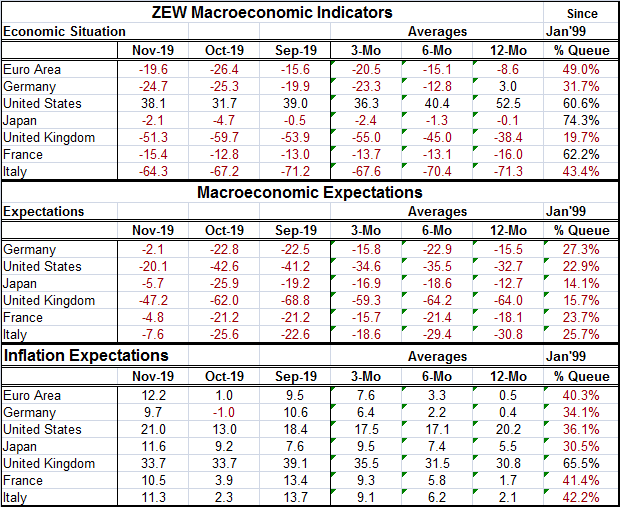

The ZEW economic situation shows net negative readings everywhere except in the U.S. Only three countries, the U.S., Japan and France, have readings above their medians since 1999. The U.K., facing Brexit issues, has the lowest standing. Germany, with the most international exposure, has a 31st percentile standing. As a whole, the euro area has a near median 49th percentile standing.

Macroeconomic expectations made near record-breaking improvement in one month's time. Still, the resulting queue standings for expectations are surprisingly uniform in November in the regions of the 20th percentile and 30th percentile, with Japan and the U.K. as exceptions having expectations in their lower 15th percentile region.

Inflation expectations have risen everywhere except the U.K. as economic conditions and expectations have improved. Still, expectations are below their median rankings everywhere except in the U.K.

The ZEW Survey on Current Conditions, Expectations and Inflation

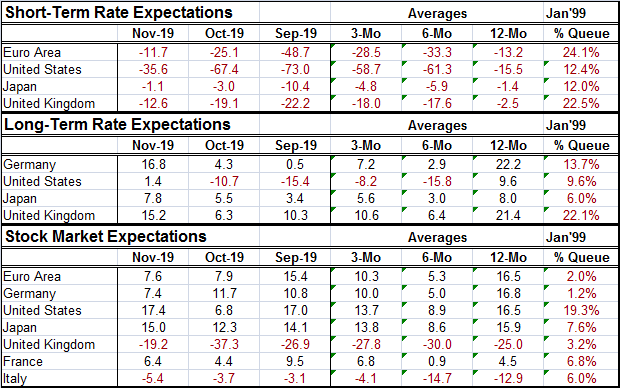

The ZEW survey on interest rates and stocks shows short-term rates still have net negative assessments. Their queues rankings across the board are below their 25th percentile and lower still with a 12th percentile assessment for the U.S. and for Japan.

Long-term interest rate expectations are net positive readings with low percentile queue standings and queue standing below those for short-term rates.

Stock market assessments are still very weak with the U.S. assessment leading the pack on a low 19th percentile standing. After the U.S., the highest stock-market percentile standing is for Japan at a very depressing 7.6 percentile standing. This is not an ‘all- clear' or ‘all is well' report this month.

Market Expectations

The summary table highlights in black those readings whose percentile standings are at or above their respective 50th percentile standing. Despite the proliferating of improving readings, few are above the median.

The surveyed ZEW financial experts have become much more upbeat. There is hope that Brexit is in its final glide path or something like it. And there is hope that the U.S. and China will have a phase one trade deal that will be passed and take some of the pressure off trade and manufacturing globally. Markets are up, expectations are up, and interest rates have risen; expectations have arisen of a sizeable positive impact on the global economy. This rising tide has lifted all boats. Still, there remains a lot of economic and geopolitical dislocation globally. If the U.S. and China do reach a trade deal, there will be changes in the terms of trade and it will be interesting to see the way trade flows respond to a new trade deal because it will not revert to business as it used to be ‘usual'. But global trade conditions should improve. The very weak readings on various global stock market expectations should serve as a reminder not to get too optimistic about what some of these changes might be able to achieve.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief