Global| Sep 17 2013

Global| Sep 17 2013ZEW Spurts! Europe Falters?

Summary

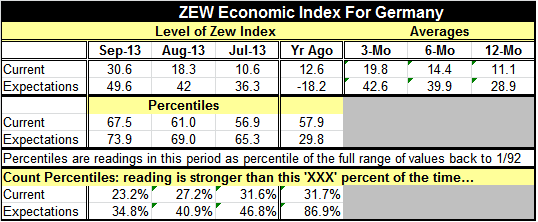

The ZEW index for Germany showed a very sharp increase in its current conditions index, rising to 30.6 in September from 18.3 in August. The expectations index moved up sharply too, it has reached 49.6 from a level of 42.0 in August. [...]

The ZEW index for Germany showed a very sharp increase in its current conditions index, rising to 30.6 in September from 18.3 in August. The expectations index moved up sharply too, it has reached 49.6 from a level of 42.0 in August. The current index is stronger than this only 23.2% of the time that compares to a similarly calculated standing of 27.2% for August. The expectations index is stronger than this only 34.8% of the time, compared with a standing of 40.9% back in August. Both indices have made appreciable improvement in the month.

The ZEW index for Germany showed a very sharp increase in its current conditions index, rising to 30.6 in September from 18.3 in August. The expectations index moved up sharply too, it has reached 49.6 from a level of 42.0 in August. The current index is stronger than this only 23.2% of the time that compares to a similarly calculated standing of 27.2% for August. The expectations index is stronger than this only 34.8% of the time, compared with a standing of 40.9% back in August. Both indices have made appreciable improvement in the month.

The current index was last stronger in June 2012. The expectations index was last stronger in April 2010 (when the current index stood at-39.2). In March and February of this year it came close to this value is it peaked out that time at 48.5%. But the combination of the current and expectations indices has been higher than this month's sum only 10% of the time.

The change on the month is also quite large. For expectations the increase ranks as the 56th largest increase in the last 241 monthly changes leaving it in the top 23% of all monthly changes. However, the current index is most striking: it's the ninth strongest month-to-month change in the current index over the same span leaving it in the top 4% of the historic queue of monthly changes.

To the Germans, something significant seems to have changed. Their assessment of current conditions has jumped substantially while the expectations for the future have jump significantly at the same time. So not only are things believed to be better and is that belief held extremely strongly, but the future is still expected to continue to improve.

Not surprisingly with this kind of assessment, the ratings of the various German stock sectors have improved uniformly in the month of September. Every single sector is expected to have better performance with the exception of insurance. If we assess the various sectors compared to their historic values we find that, for Germany, consumption and trade ranks as the highest sector in the top 14% of all its historic readings. It is followed by construction in the top 79.9 percentile, electronics stand in the 75.1 percentile and chemicals and pharmaceuticals rank in the top 73.2 percentile. Lagging sectors are utilities where the ongoing it denuclearization program is hitting the industry hard, telecoms (in the bottom 33.9 percentile of their range) and insurance which was the sole sector to deteriorate this month and its assessment is in the bottom 37.2% of its historic range.

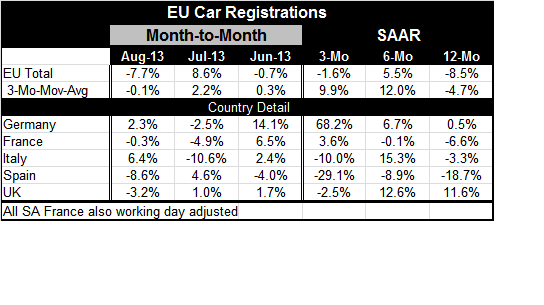

We can contrast that upbeat response to the Zew report for September with the EU-wide report on auto registrations. The data appear in the table below and demonstrate ongoing weakness.

While Germans may think that the German economy is "on fire," the rest of the EU seems to have had a bucket of cold water thrown over its head. Auto sales in the EU fell by 7.7% in August after trying to firm up on an 8.6% gain in July. The three-month annual rate change in car registrations in EU is -1.6%. There is a +5.5% gain over six months but also -8.5% drop over 12 months. The percentage changes calculated on three-month moving averages of registrations are somewhat more favorable.

Looking at some individual countries, we can see why Germans are upbeat, as registrations in Germany are up at a 68.2% annual rate over three months, up from a 6.7% annualized increase over six months bringing auto registrations up 0.5% year-over-year. Even though France has declines in each of the last two months, it has an increase over three months of 3.6% (saar) but declines of 0.1% over six months and of 6.6% over 12 months. It's still unclear if this is volatility for France of if it is really digging itself out of a deep hole. Italy's monthly registrations are very erratic but over three months sales are falling at a 10% annual rate; over six months they are declining at a 15% annual rate and over 12 months at a 3.3% annual rate. While it's hard to pick up any trend there, it's clear that registrations in Italy are still weak. Spain shows registrations down at a 29.1% annual rate over three months at a 8.9% pace, over six months and by 18.7% over 12 months. The Spanish economy is struggling and so are auto registrations. The UK showed a setback in registrations on the month and a decline of 2.5% over three months; over six months UK registrations are up at a 12.6% annual rate and over 12 months up and 11.6% annual rate.

The UK has not had a year-over-year drop in registrations since February 2012. Germany has posted its first year-over-year gain this month June 2012 France has not had a year-over-year gain since October 2011. Italy had a brief year-over-year increase in March 2013. While Spain had a year-over-year increase in July 2013 and one in April 2013, but it has not had a sustained string of increases since June 2010. The EU itself posted a year-over-year increase in its July 2013 data but in August we see its return to declines of about the same magnitude that we have been seeing over the last seven months or so. Previous to that, the last year we saw an increase in EU registrations was in September and August of 2011.

Although we see that over the broader haul the EMU index on business climate seems to move broadly with the current Zew index from Germany, in this month's data we see potential evidence of a disconnect. While Germany's current index in the Zew survey has moved up very strongly, and as its expectations index continues to advance, car registrations throughout Europe continue to lag - except in Germany. German car registrations are up very sharply and they agree with the assessment of the Zew survey for Germany. It remains to be seen if the rest of Europe is going to follow and if Germany will exercise much of a locomotive effect on the rest of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief