Global| Jan 17 2017

Global| Jan 17 2017ZEW Shows Improvement in German Current Conditions and Expectations

Summary

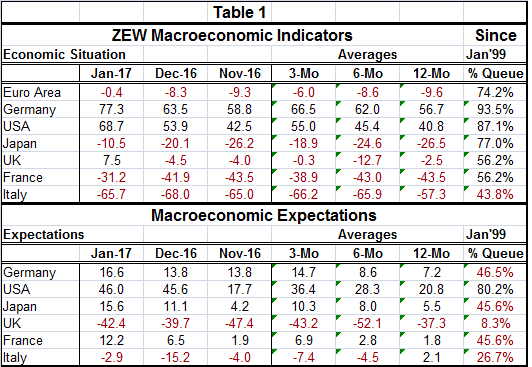

Table 1 shows a sharp improvement in German current conditions and a rise in German expectations. The German current index has been better historically less than 7% of the time while expectations are better about 54% of the time. [...]

Table 1 shows a sharp improvement in German current conditions and a rise in German expectations. The German current index has been better historically less than 7% of the time while expectations are better about 54% of the time. While German expectations moved up, the expectations indicator stands below its historic median. With the current conditions reading so strong, the position of the expectations indicator is harder to interpret. Are Germans becoming less enamored with future prospects? Or are current conditions so good that pragmatists are realizing that such strong conditions simply can't last?

Table 1 shows a sharp improvement in German current conditions and a rise in German expectations. The German current index has been better historically less than 7% of the time while expectations are better about 54% of the time. While German expectations moved up, the expectations indicator stands below its historic median. With the current conditions reading so strong, the position of the expectations indicator is harder to interpret. Are Germans becoming less enamored with future prospects? Or are current conditions so good that pragmatists are realizing that such strong conditions simply can't last?

Current conditions are in a positive Zone for all countries/areas in the table except Italy. Italy stands in its 43rd queue percentile, below its median and is better off than this month's reading some 57% of the time. France and the U.K. are near midrange with conditions that are better only about 44% of the time. Conditions in Japan are better only 23% of the time. In the U.S., conditions are better only 13% of the time. For all of the euro area, conditions are more like Japan, better only 26% of the time, but with the heterogeneity implied buy the gaps between the German, French and Italian readings at least. Heterogeneity continues to be a policy problem for the ECB.

Expectations reading are uniformly lower than for current readings with only the U.S. clocking a reading above its median (50% level for queue standing). The U.K. has a -42.4 raw diffusion score and an 8.3 percentile standing as it continues to erode. Italy also has a negative diffusion reading and posts a 26th percentile standing. Germany, Japan and France all have percentile standings about 5 percentile points below their medians. The U.S. is the class of the future with an 80th percentile standing and nowhere in these tables is any country close to that.

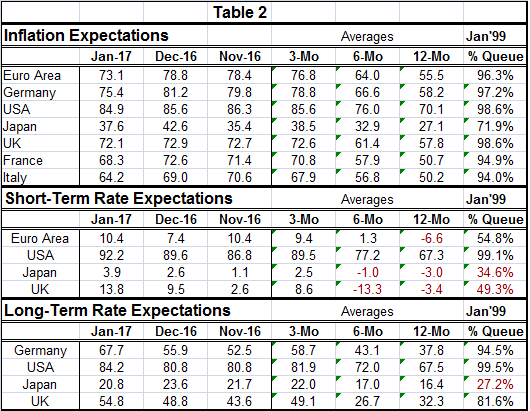

Table 2 below provides inflation expectations readings and interest rate expectations for select monetary regions. What is clear is that while diffusion readings vary somewhat, the queue standings show inflation readings are elevated and well above countries' respective medians everywhere. The standings in fact are at or above the 94th percentile (in the top 6%) everywhere except Japan where they are in the top 30%. I take this to be a statement about rising oil prices. Notice how much more in sync are the long-term rate expectations compared to the short-term rate expectations - especially their queue standings. This reflects differing central bank circumstances.

Rate expectations readings show two clear assessments. First, only in the U.S. are short rates strongly expected to rise (99.1 percentile standing!). Secondly, everywhere the probability of rates rising has been increasing compared to 12 months ago and generally from 12-month ago to six-month to three-month.

The ZEW financial experts are right now riding three trends: (1) the tide of economic momentum; (2) Donald Trump's election and changed prospects that implies in the U.S.; and (3) higher oil prices from the OPEC cartel and others. The ZEW outlook is more or less a mainstream view of how growth is developing. And while current readings are quite elevated, the ZEW perspective on expectations, except for the U.S., of course, should be a real wake up call to optimists everywhere. The ZEW experts are not being drawn in hook line and sinker to an ever improving outlook. Their enduring pessimism on the U.K. over Brexit has not wavered even as U.K. economic performance has continued to be strong. The ZEW experts are concerned about Italy and have only recently begun to be positively impressed by France. They see Japan in a slow work out but do see it as making progress. Germany is also showing some progress but slow progress and not from such an elevated level regarding expectations. In the U.S., the assessment jumped after the elections and has hovered at high readings ever since. There is still a lot to sort out over the future. The glowing Trump future is going to have to start paying real time dividends or even this optimism will be pared back.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief