Global| Oct 14 2014

Global| Oct 14 2014ZEW Plummets; Putting Germany on the Recession Threshold

Summary

The ZEW current index, which had been so resilient, fell sharply in October, dropping to 3.2 from 25.4 in September. The expectations index fell into negative territory for the first time since November 2012. The current index is [...]

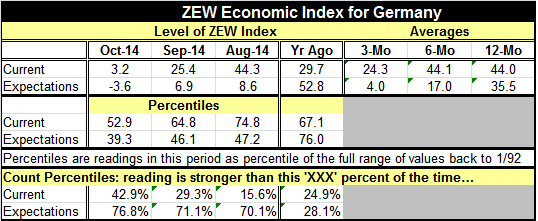

The ZEW current index, which had been so resilient, fell sharply in October, dropping to 3.2 from 25.4 in September. The expectations index fell into negative territory for the first time since November 2012.

The ZEW current index, which had been so resilient, fell sharply in October, dropping to 3.2 from 25.4 in September. The expectations index fell into negative territory for the first time since November 2012.

The current index is sitting on the threshold of zero where German recessions typically start. Its 3.2 point cushion is small, especially when weighed against the recent momentum in this index. The current index fell hard this month; its month-to-month drops are bigger than this less than 5% of the time.

The percentile standings of the current and expectations indices have fallen significantly from where they were. One year ago the current index was stronger only about 25% of the time while the expectations index was stronger less than 30% of the time. Now current conditions are stronger 42% of the time and expectations are stronger over 75% of the time.

The assessment of stocks is being cut this month to reading of 2.1 from 3.0 in September. The assessment of bonds has risen to -3.6 from -5.4. The stock assessment was last weaker in September 2012. Of the 13 sectors that ZEW to participants rate, only three of them saw improvement month-to-month; those sectors were utilities, banking and insurance. Eight of the 13 sectors have assessments that rank below the 50th percentile of their historic range of values. The average stock market assessment by ZEW professionals is weaker than it is in October only 25% of the time. There is a great deal of weakness in this report.

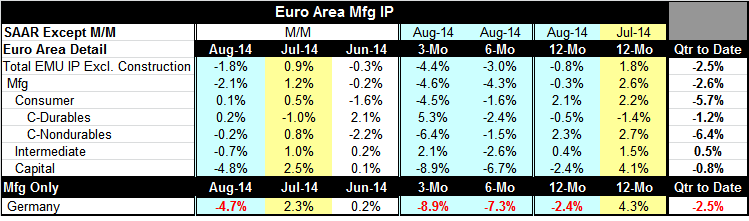

At the same time the euro area manufacturing data for August, released today, show a sharper-than-expected drop in August with the overall EMU index falling by 1.8% and dropping in two of the last three months. The European Monetary Union's industrial production path shows sequentially bigger drops, measured at an annual rate, moving from 12 months to six months to three months. This kind of progressive deterioration is a bad sign. We see that same trend echoed in the German report for its manufacturing sector, at the bottom of the table.

The participants to the ZEW survey are financial experts. They can see the deterioration in Germany and in the European region as a whole. We see that European manufacturing output is getting progressively weaker; that the consumer sector is weakening progressively and that the capital goods sector is also weakening progressively. Some resilience has been shown for intermediate goods and even within the consumer sector for consumer durables, but weakness predominates.

We had seen some signs of weakening conditions in Europe ahead of the imposition of sanctions on Russia. But the imposition of sanctions itself has clearly worsened the state of economic activity in Europe and especially in Germany. While Russia has tried to hide some of its weakness, it's quite clear that there's a good deal of turmoil on the Russian side of the ledger. The recent inability of the Russian central bank to stop the progressive deterioration in ruble is evidence of this. However, sanctions are hurting both parties. There is no sense that either side is backing off or capitulating. In fact, given the demeanor of Vladimir Putin, the weaker that the Russian economy gets more dangerous the situation becomes. This, of course, is very bad for economic events and especially for Europe that depends on Russia for its basic energy needs. As bad as things are, they could get worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief