Global| Sep 15 2020

Global| Sep 15 2020ZEW Macro-expectations Reach for the Sky

Summary

Meanwhile, back on earth, conditions remain weak and mixed ZEW expectations rose in September in five of the six countries surveyed; the United Kingdom was the exception. Current conditions improved everywhere up and down the line but [...]

Meanwhile, back on earth, conditions remain weak and mixed

Meanwhile, back on earth, conditions remain weak and mixed

ZEW expectations rose in September in five of the six countries surveyed; the United Kingdom was the exception. Current conditions improved everywhere up and down the line but still remain at very weak levels. In contrast, expectations are uniformly very strong. Inflation expectations rose quite substantially everywhere and everywhere except in Japan inflation expectations are above their historic median readings. Yet, interest rates are still tabbed to be lower –even lower than before in the euro area but less low in the U.S., Japan and the U.K. Still, all interest rate readings are below their historic medians. Longer term interest rate expectations are higher as these other attributes suggest they should be. With conditions improving and expectations high and expectations for rates to be cut even as inflation expectations are rising, yield curves globally are expected to steepen. All stock market gauges are somewhat stronger…in the case of the U.K. that means less ‘weak.’

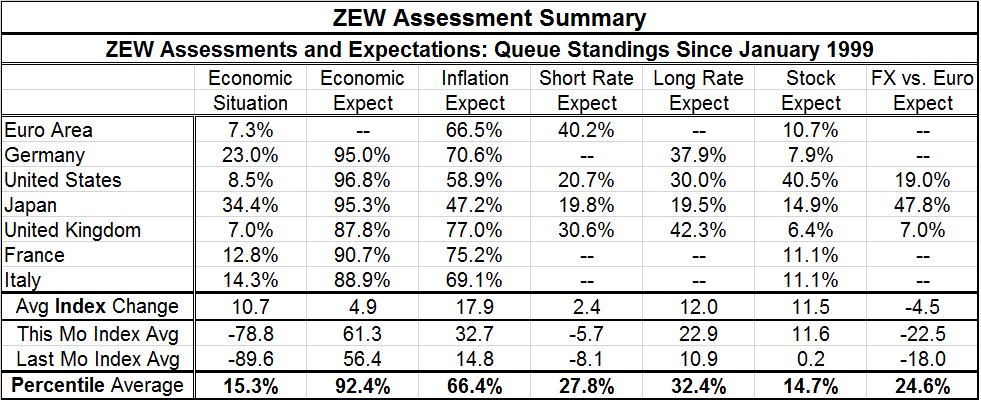

The table below presents a summary of these trends by listing the queue percentile standings for each cell and, as a summary statistic, the average change on the month for the group, the average diffusion reading for the group for both this month and last month, and the average of the percentile standings in the table. The summary data are unweighted.

Economic expectations were up on the month and that was surprising because they already were at such a high-water mark. The monthly gain was only 4.9 points on average, a small change. By comparison, the 10.7 diffusion point rise in the economic situation is much larger and the rise in inflation expectations is clearly the biggest change on the month, gaining 17.9 diffusion points. Even with this rise in inflation expectations (which saw a near doubling in the U.S. as expectations rose from 22.5 to 43.1), the short-term rate metrics remained below their respective medians across the survey. In the EMU area, expectations for lower rates moved lower from a reading of -4.6 to -6.6 as inflation expectations more than doubled (rising to 31.0 from 14.3). Inflation expectations tripled or nearly so in France, Italy and in Japan. These readings moved the average queue standing for inflation expectations above the 50 percent mark, the only category to do that. The impact of all those monthly shifts on long-term interest expectations was to boost them by a modest 12.0 points, as they still more than doubled. Still, it is not clear how or when – of even if -- this will happen.

One thing driving inflation expectations is some new language at the Federal Reserve in the U.S. that has mostly confused financial experts since the language has been introduced but it is purposely vague so vague that it has no literal meaning. In the end, though, it has convinced experts that the Fed is ‘serious’ about getting the inflation rate higher but does not wish to reveal too much about how it will go about doing that – nor to tie its hands to only one approach or method. There is also the disruption of the international trade system and renewal of tariff barriers that should act to raise business costs and thereby also contribute to inflation.

At the same time, inflation remains low and unemployment is high especially in the U.S.; in other places, labor remains underutilized but not necessarily unemployed. Spending is substantially being supported by various government programs globally. And yes central bank balance sheets are bursting at the seams, but this is in reaction to economic distress. The heightened tensions about future inflation are able to be understood in this context and yet they also ring hollow under current conditions. It is not clear to me, for example, that the change in Federal Reserve language actually means anything just yet. By the time it begins to have meaning, it is entirely possible that the Fed will change it again.

On this same background, stock market expectations are muted with percentiles at an average of 14.7. It is hard to square the conditions for inflation rising with such weak stock market performance. Long-term interest rates have only a 32.4 percentile standing on average. This is no inflation pressure cooker.

Clearly, the ZEW survey participants feel this is some sort of a turning point or at least and inflection point for policy. The virus has been around for a while and people appear to cope with it. But the main response to outbreaks of the virus remains the same, to use mitigation strategies or outright lockdowns that slow growth. The virus is still circulating and there are vaccines in various stages of trial. The feeling is growing that ‘our’ capacity to deal with the virus is about to change – rightly or wrongly. But at the same time, attitudes toward the virus remain the same and most of the public is still very wary about getting it. It seems to me that expectations are leaping ahead on any likely reality. As always, time will tell about that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief