Global| Aug 13 2013

Global| Aug 13 2013ZEW Index Rises on Both of Its Legs

Summary

Last month Germany's ZEW index rose on only one leg while this month it rises on two, as both current conditions and expectations have improved month-to-month. Last month, as the current index advanced to 10.6 in July from a reading [...]

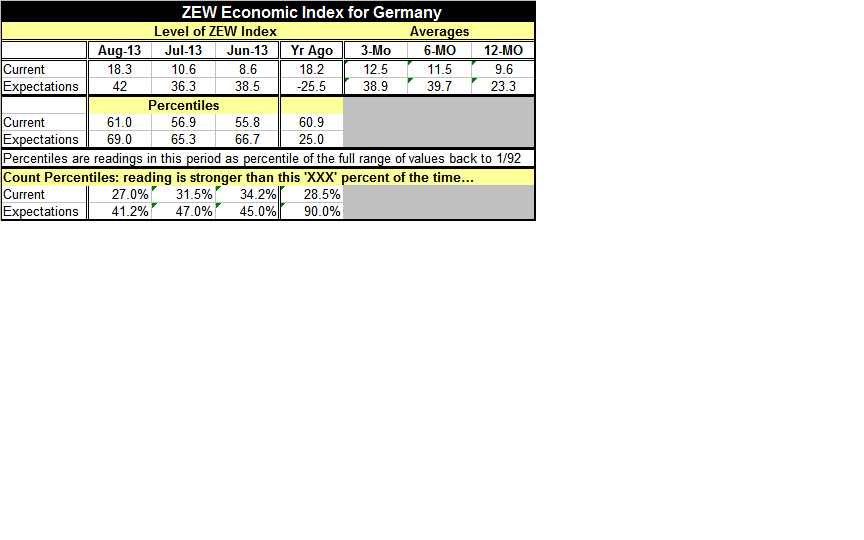

Last month Germany's ZEW index rose on only one leg while this month it rises on two, as both current conditions and expectations have improved month-to-month. Last month, as the current index advanced to 10.6 in July from a reading of 8.6 in June, the expectations index fell from 38.5 to 36.3. This month, both the current and expectation indices are advancing and they are both advancing fairly sharply. The current index has risen to 18.3 from 10.6. The expectations index has risen to 42 from 36.3. The current index has moved up to the 27th percentile of its queue from the 31.5th percentile back in July, a gain a 4.5 points in its percentile standing. Expectations have moved up nearly 6 points in their percentile standing to the 41st percentile from the 47th percentile. The percentile readings tell you how often the readings posted this month tend to be stronger than their current values. Lower percentile standings denote stronger readings.

Last month Germany's ZEW index rose on only one leg while this month it rises on two, as both current conditions and expectations have improved month-to-month. Last month, as the current index advanced to 10.6 in July from a reading of 8.6 in June, the expectations index fell from 38.5 to 36.3. This month, both the current and expectation indices are advancing and they are both advancing fairly sharply. The current index has risen to 18.3 from 10.6. The expectations index has risen to 42 from 36.3. The current index has moved up to the 27th percentile of its queue from the 31.5th percentile back in July, a gain a 4.5 points in its percentile standing. Expectations have moved up nearly 6 points in their percentile standing to the 41st percentile from the 47th percentile. The percentile readings tell you how often the readings posted this month tend to be stronger than their current values. Lower percentile standings denote stronger readings.

If we look at momentum we see that both the current and expectations indices are moving up compared to the values the past months. The current index is moving up the most steadily with a 9.6 average over 12 months, which moves up to an 11.5 average reading over six months to a 12.5 average reading over three months. These compare with its current standing at 18.3. Those are all progressively stronger numbers.

Expectations have moved up from a 23.3 average over 12 months to a 39.7 average over six months; then there was a setback, as over the last three months expectations have only averaged 38.9. However, with another gain this month to a level of 42, expectations may be back on the rise once again-- that is going to be something to watch.

We show the chart of the ZEW expectations index vs the DAX stock market index. While the statistical correlation between the ZEW expectations index and the stock index is not very high, there is a clear message in the way the expectations index maps consistently into the performance of the stock market.

When the ZEW expectations index hits zero or breaks through zero that tends to be a signal that the stock market advance is going to pause and give way to a decline. The signal from the expectations index to the stock market generally leads it by more than six months. It's clear that the expectations index below zero is a bad signal for the German stock market. On the other hand, an index that rises and breaks up through zero is a strong signal, and a positive development for the German stock market. Therefore the more that the expectations index moves away from zero the more comfort we can have about the performance of the German stock market in the months to come. Since 2003 there been no instances of any major setback in the DAX without the expectations index sitting at or below zero or falling sharply and headed for breaking zero. None of those signals are now present.

Of the 13 sectors that the German financial experts evaluate, only five are evaluated lower in August than they were in July those five include 'chemicals and pharmaceuticals,' 'steel and metals,' electronics, construction and info-tech.

Apart from their monthly changes, the most strongly evaluated sectors for their expected profitability this month are 'consumption and trade' which has been assessed as stronger than this only about 20% of the time. Construction also ranks high for expected profitability; it is evaluated as stronger than this only about 25% of the time. The relative weakest sectors are utilities, a sector that still has that negative impact of Germany moving away from nuclear power hanging over its head, followed by telecoms a sector that is evaluated as weaker only about one third of the time.

By and large however profit expectations by industry are continuing to move up in a sort of saw-tooth pattern from their recent lows. The current recovery in expected profits dates back to December 2011. In keeping with the more upbeat view of the future, the evaluation of bonds turned slightly more negative this month producing a -1.7 reading, weaker than the -6.4 reading of last month, showing its weakest reading since March 2013.

The German financial experts are well aware that the German economy is different from that of the European Monetary Union's economy. But they also are aware that the performance of the German economy will depend on the performance of the area around it. Germany is after all in the same union with its fellow members and has important trade ties with them. As economic data have become somewhat more upbeat for the surrounding euro-Zone, it is not surprising that the German financial experts are raising some of their expectations for the German economy. As they do that they also get more upbeat on the outlook for equities and have been scoring the fixed income market more harshly.

The jury is still out on how sustained this improvement in the European economy --and in Germany-- will be. But, for now, the impact of the improvement in European circumstances on Germany appears to be positive as the German economy itself continues to perform somewhat better. All of this is reflected in stock and bond market developments as well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief