Global| Mar 19 2013

Global| Mar 19 2013Zew Index Rises Again in Germany

Summary

Germany's Zew index which surveys the assessments of select financial experts in Germany continued to rise in March. This Zew expectations index rose to 48.5 in March from 48.2 in February. While continuing a series of gains, the [...]

Germany's Zew index which surveys the assessments of select financial experts in Germany continued to rise in March.

Germany's Zew index which surveys the assessments of select financial experts in Germany continued to rise in March.

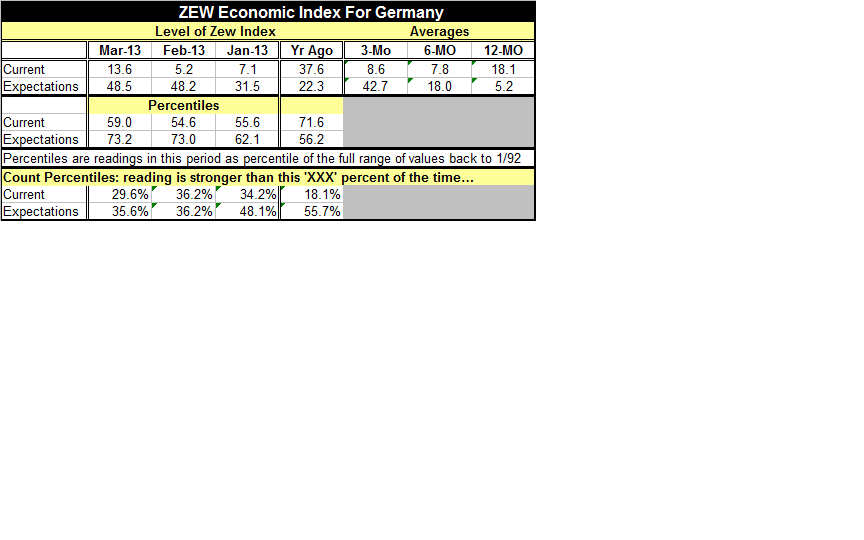

This Zew expectations index rose to 48.5 in March from 48.2 in February. While continuing a series of gains, the expectations index has really slowed its rate of change. In March the index is up by mere tenths of a point whereas between January and February the index rose by some 17 points. At its current level the expectations index is stronger than its current level about 35.5% of the time.

The current index also moved up this month and its rise accelerated. The current index stands at 13.6 in March, up from 5.2 in February. It had backed off in February to a reading of 5.2 from a level of 7.1 in January. At its present level the current index is higher roughly 30% of the time.

In broad terms the current Zew expectations indices reside at about the same relative position of their respective ranges. Historically the expectations index does tend to bounce around quite a bit. There are rises and falls in expectations in the middle of business cycles; the turnout seems to reflect the surveyors anxieties even more than their perceived realities. But the current index tends to move in broader more stable cycles. In that regard the current index has made its traditional rise in the recovery, after the financial crisis. It has reached a nice strong peak and it has proceeded to move to lower levels with some pausing and then a move to still-lower levels. Now it's engaged in a minor uptick; the rise in the current doesn't seem particularly significant in the history of the series.

The Zew expectations index continues a four-month run of improving expectations. Yet, it also has increased in six of the last seven months. However, the slowdown in the change in expectations has become clear in the recent pattern. In December expectations increased by 22 points from November, in January that monthly rise accelerated to about 24 points, and y February that settled down to around 16 points. Now, in March, the month-to-month gain is less than one point. During this period the change in the current index has been quite contained with monthly changes of less than two points until this month when the current index rose by 8.4 points. The topical readings both for the current and the expectations indices from the Zew financial experts are quite solid; however, there is not much in the report to cause us to think that the past pace of improvement is continuing. Meanwhile, conditions in the zone around Germany remain as tangled and dodgy as ever and actually seem to have worsened.

Still, economic data on the day reflect the same kind of mix performance in the Eurozone that we have been experiencing. As we report here, the Zew index rose. The OECD cut its outlook for France, urging France to do more to increase its competitiveness. Italy, although in political turmoil, posted a relatively sharp gain in its industrial production index. In the UK, where growth has remained scarce, inflation has tipped back up again. And for all of Europe, new car registrations continue to be weak. Car registrations in February fell by 10.5% year on year faster than their 8.7% decline in January.

Of course investors and policymakers are very interested in trying to figure out where the German economy and the European economies are going. Recent events in Cyprus have raise anxieties about the Eurozone as well as about the intentions of the people who were driving its policies. There is a strong German bias the policy of the European Union that demands punishment for bad behavior. We see this strongly in the initial policy toward Cyprus. But, sensing the market reaction, we are also seeing some significant backtracking. Cyprus is not sure it can pass the plan as it was proposed. The ECB has distanced itself from the tax-all deposit policy. A new policy is being mooted with no tax on relatively small bank accounts.

Many commenters on the Cyprus plan have exhibited assessments that range from being shocked to being dismayed. There has been very little support for the program. Calling it a one-off affair has not rehabilitated it or blunted criticism. The bigger issue is that it raises this new policy approach as a potential to be used elsewhere in the Eurozone despite protestations of those who have tried to implement this plan and who argue that is not the case. It also raises questions about the judgment of those making policy and about whose interests are being foisted upon whom...

The treatment of Cyprus is a warning shot across the bow of any of the smaller EMU nations that membership will not necessarily be a safe harbor for them. Neither is there any indication that joining the monetary union will bring anymore economic or financial stability. It is important for any nation considering membership in the Eurozone area to remember that this is an area that is named after the currency, "the euro". This union appears to put the success of and preservation of the single currency above all else. This is not a union that will use its currency policy to achieve prosperity but a union that will subjugate economic policy to protect and defend the solidity of the euro currency itself. There has been very little cross-border 'sharing' and what occurred has been out of necessity and often only after tooth-pulling. If ever we wondered what the euro would be, with the Germans mixed in with others holding very different values, polices and tendencies, now we know. So let this be an observation or a warning to all who enter here. Those who would enter will be subjugated.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief