Global| Aug 12 2014

Global| Aug 12 2014ZEW Index Drops Sharply

Summary

Germany's ZEW current index fell sharply in August to 44.3 from 61.8 in July. The current index had peaked at 67.7 in June in this cycle. It's now on a two-month drop. Expectations, the more closely watched component, fell to 8.6 in [...]

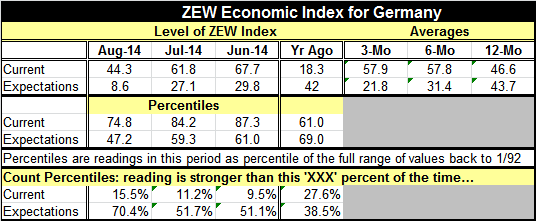

Germany's ZEW current index fell sharply in August to 44.3 from 61.8 in July. The current index had peaked at 67.7 in June in this cycle. It's now on a two-month drop. Expectations, the more closely watched component, fell to 8.6 in August from 27.1 in July. This index had peaked at a level of 62 back in December.

Germany's ZEW current index fell sharply in August to 44.3 from 61.8 in July. The current index had peaked at 67.7 in June in this cycle. It's now on a two-month drop. Expectations, the more closely watched component, fell to 8.6 in August from 27.1 in July. This index had peaked at a level of 62 back in December.

The current index is stronger than its current value only 15% of the time; the current reading reflects a still-strong standing. However, the expectations index with its recent tumble is stronger than its current value about 70% of the time. This month's drop pushed it down into the lower portion of its historic queue of readings.

The assessments of stocks by sector oversaw declines in each of the sectors except utilities. Industrial stocks assessments were hit particularly hard. The profit expectations by industry have fallen sharply this month.

The sharp drop in the ZEW index means that there is more attention to the fact that German growth estimates are pointing to declining GDP in the second quarter. The weakness, of course, is being blamed on fallout from events in Ukraine. Those events both adversely affect current German business as well as dampen expectations for the future.

We've also seen activity weakness in other European Monetary Union countries, particularly Italy that has now seen GDP drop for two consecutive quarters. It's a difficult time for Germany and the EMU to have to deal with the fallout from the Russian sanctions.

The European Central Bank has been promoting a special credit enhancement program in the wake of what have been very weak inflation numbers in the euro area. However, Portugal has just reported out an accelerated drop in its HICP inflation, which has accelerated to -0.7% year-over-year. Italy's inflation rate is still stuck at 0.2% year-over-year. Sweden, an EU member but not an EMU member, has its inflation flat year-over-year in a report just released today. But Bulgaria consumer prices are declining in July. Croatia's PPI continues to decline in July. There continue to be strong anti-inflationary forces both in and around the euro area, at a time when economic activities are tailing off, apparently, for various reasons. This has to present the most perplexing challenge for the ECB.

Germany's economy is currently faltering and its economic barometers remain weak. Its consumer sentiment indexes, however, have continued to be quite strong. We know that Germany's business connections with Russia, while the largest in Europe, only recently surpassing Finland, are nonetheless not large in the context of the entire German economy. It may be that the culmination of the effect of the sanctions hit Germany particularly hard this quarter and it will be able to rebound in the coming quarters. That, of course, is a view focused mostly on the impact of the Russian sanctions. There is another aspect to consider, and that's the encroaching weakness in other euro area countries as exhibited by Italy falling into recession again. This is a time when the euro area could really benefit from Germany as the juggernaut of growth. Germany does not always have the highest growth rate in Europe, but it tends to have the steadiest. This is a difficult time for Germany to be flirting with a negative growth rate.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief