Global| Jul 17 2013

Global| Jul 17 2013Zew Index Backtracks Instead of Making Progress

Summary

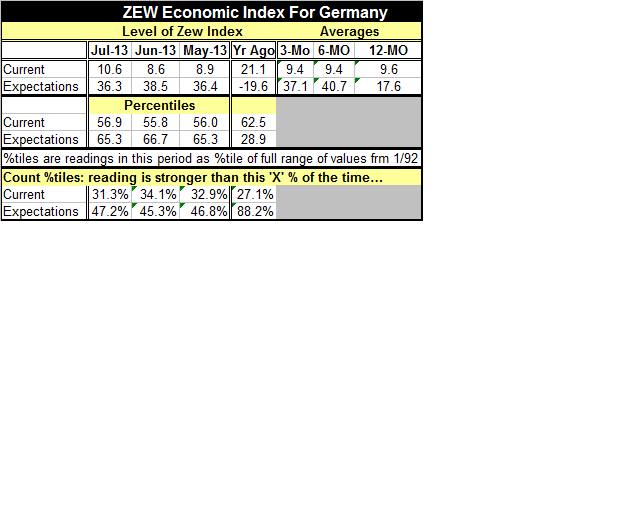

The expectations index of the ZEW survey backed off to 36.3 in July from 38.5 in June. One year ago the index stood at -19.6. Current index continued to advance rising to 10.6 from 8.6 in June. While markets were mostly unnerved by [...]

The expectations index of the ZEW survey backed off to 36.3 in July from 38.5 in June. One year ago the index stood at -19.6. Current index continued to advance rising to 10.6 from 8.6 in June.

The expectations index of the ZEW survey backed off to 36.3 in July from 38.5 in June. One year ago the index stood at -19.6. Current index continued to advance rising to 10.6 from 8.6 in June.

While markets were mostly unnerved by the backtracking in expectations, especially against a consensus belief that expectations were improving, the fact is that the reading is very little changed in July. In fact the change on the month was quite small, in the bottom 25 percent of all monthly changes by size (in absolute value). The reaction to the Zew reading is probably more of a statement about German nervousness than about actual conditions.

The current Zew reading of 10.6 is stronger than its current value only about 31% of the time. Thus the German economy is still performing at about the top third of what it normally does. Expectations at 36.3 in July are better than this about 47% of the time. That's a coin toss sort of standing. And given that the economy is performing so well it should be somewhat reassuring that it's putting in top-third quality of performance and expectations are more or less that it will continue to do just that.

However, with the backing off of the Zew expectations index there is a lot of talk of concerns about problems in the Eurozone and how they are starting to dog Germany. That may be true, but the investment professionals that contribute to this survey rated stocks slightly better in July than in June at a +5.5 reading compared to +4.4 in June. They downgraded bonds to -6.4 after a -6.2 in June; although both of these bond ratings are generally better ratings than we have been seeing from them since September of last year.

The profit expectations by industry continue to weave an uneven path higher.

Unless there is some far more negative development it's hard to take the small setback in the German ZEW expectations index as any sort of negative harbinger for the economy.

One thing we do have to admit is that the trade data that have been filled out for a number of countries in the euro-Zone are not pointing to very robust growth. Performance for the euro-Zone and for a number of countries in terms of the impact on their trade account has been positive largely because of drops in imports. Italy, for example, posted a very out-sized drop of 10% in imports year-over-year. Countries in the euro-Zone are really struggling to mount some kind of domestic demand.

There are an increasing number of stories about how Germans are becoming disillusioned by their participation in the Euro-Zone. Oskar Lafontaine, a well-known German figure from the political left, has recently joined criticism of the euro-Zone, a position that had principally been that of the German right. With national elections on tap in Germany later this year it is not likely that Germany's position on the euro-Zone is going to become an election issue. Angela Merkel is doing whatever she can to try to keep that in the background. However, there is boiling discontent in Germany to add to the questioning elsewhere in the euro-Zone. And to top it off there continues to be disappointing economic results. When countries are improving their trade positions largely because of weak imports it's not a good sign. And that has been one of the hallmarks of European membership recently.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief