Global| Mar 17 2015

Global| Mar 17 2015ZEW Index Advances with Some Caution

Summary

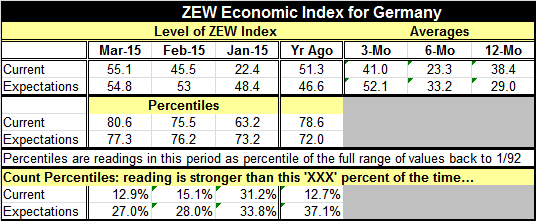

Germany's ZEW index saw increases in both its current index and its index of expectations. Both are in `good shape' in terms of their levels and in terms of their momentum. The current index is higher than its March value historically [...]

Germany's ZEW index saw increases in both its current index and its index of expectations. Both are in `good shape' in terms of their levels and in terms of their momentum.

Germany's ZEW index saw increases in both its current index and its index of expectations. Both are in `good shape' in terms of their levels and in terms of their momentum.

The current index is higher than its March value historically only 12.9% of the time. The expectations index is a bit less robust but is higher only 27% of the time. The current index was last higher in July 2014. Expectations were last higher in February 2014.

Despite the apparent good news in this report, the takeaway here is that the ZEW expectations index rose by less than expected. That index advanced by just 1.8 points month-to-month; still, it did advance and holds a relatively high level. But the slowing in the advance to a pace likened to crawl is not what had been expected. Hence that is the take-away. But let's not elevate that bit of inside-the-market analysis above the basic good news of the March readings themselves, which are still quite good.

Recent EMU and especially German economic data have been mostly upbeat. Various German agencies have been increasing their forecasts for growth in 2015, albeit not to strikingly higher growth rates but to slightly better numbers. The smallness of the advance in ZEW expectations seems to take the German economy off the fast track expansion onto a side rail.

ZEW financial experts gave stocks a slightly worse reading in March. The equity assessment is tied for its weakest reading since December 2014. The bond outlook was hiked to a still negative value but the best bond assessment since February 2009.

Stock profit expectations have been lifted in March compared to February in 12 of 14 sectors of the German market, led by vehicles. The outlook for vehicle profitability is at its relative highest reading historically. One thing to bear in mind is that Germany does export a number of high-end autos to China and that China has a corruption crackdown in place. There have been concerns that this crackdown could be negative for German car exports, but that does not seem to loom as a factor to the ZEW experts.

The German stock market sectors of chemicals/pharmaceuticals, electronics, machinery, and consumption/trade all are sectors with profit expectations that are assessed to be in their top 10% historically (in addition to vehicles, of course). Knocking on the door to this club is the German construction industry. Utilities, largely because of the phase out of nuclear power, and banking are the two relative weakest sectors by profitability expectations.

Germany and the EMU still have challenges. At the end of Q4 2014, EMU employment growth slowed to gain 0.1%, weaker than its 0.2% gain in Q3. Looking ahead, the financial experts' assessment of financial conditions obviously has a lot to do with perceptions of how the ECB's QE program will play out and how effective it will be. There is also some tacit assumption about Greece. For a time, Greece seemed to settle down. But since exiting direct negotiations with Europe, we have found the Greek leadership asking for Nazi reparations from the war years, something the Germans did not even address except to say that those issues were settled long ago. In news today, Greece is telling us it is planning to use the proceeds from its government asset sales to fund social benefit programs instead of to retire debt. This seems an unwise decision since asset sales produce a one-time lump sum payment while social benefits create a never-ending flow of payments for the future. Perhaps indicating the next card it can play in this game there is a Greek meeting with Russia now on the docket.

On balance, it seems Europe still has a number of unresolved issues. Greece is a never ending comedy/tragedy and I'm not sure it has a clear cut final act. The economic and financial climate in Europe is still very much in flux. Germany has seen some improvement in expectations, but the pull back in momentum for expectations may indicate a new wait-and-see attitude on the part of German financial experts. We think some pullback and reassessment makes sense, especially in this off-kilter environment with so much policy experimentation afoot.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief