Global| Jan 21 2020

Global| Jan 21 2020ZEW Experts See Improvement...But Is There Really That Much?

Summary

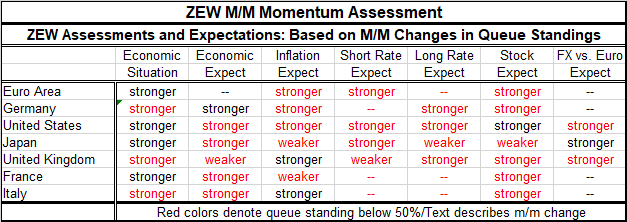

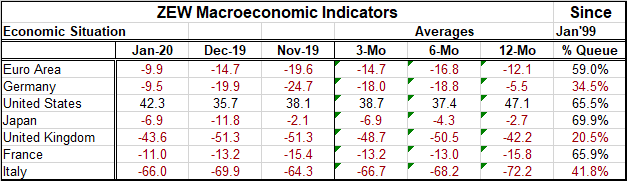

The ZEW financial experts, out of 38 assessments, find that there is more strength in 32 of them. The sweep of the change in assessments is undeniably higher in January. The economic situation has four above 50 percentile standings [...]

The ZEW financial experts, out of 38 assessments, find that there is more strength in 32 of them. The sweep of the change in assessments is undeniably higher in January. The economic situation has four above 50 percentile standings (above median). However, only the United States has a net diffusion reading that is positive.

The ZEW financial experts, out of 38 assessments, find that there is more strength in 32 of them. The sweep of the change in assessments is undeniably higher in January. The economic situation has four above 50 percentile standings (above median). However, only the United States has a net diffusion reading that is positive.

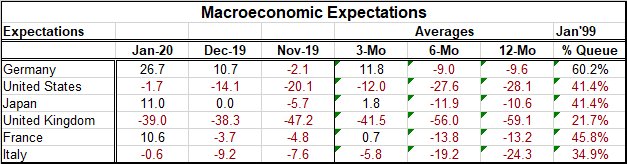

Macroeconomic expectations show improvements this month compared to December in all countries except the United Kingdom where a small further deterioration has been posted. Macroeconomic expectations have an above 50 queue standing only in Germany (60.2%) while Germany, Japan and France show positive net diffusion readings with the U.S. and Italy logging only very small negative diffusion readings.

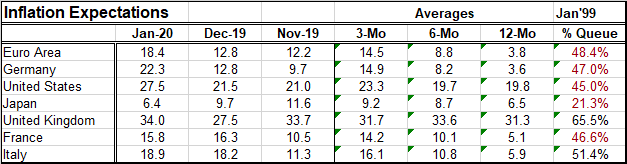

The ZEW experts remain hopelessly Keynesian in their apparent thinking as improved expectations and improved growth are going hand-in-hand with higher inflation expectations. Inflation is tipped to be lower in only two countries, France and Japan. The queue standings for inflation are, however, still below their historic medians everywhere except in the U.K. and Italy. Compared to a year ago, inflation expectation diffusion values are higher by double digits in the euro area, Germany, the U.K., France, and Italy. They are higher by 30 or more diffusion points in the euro area, Germany, Italy, and nearly so in France. Inflation expectations are now near normal (near historic median values) in the euro area, Germany, France, the U.K., and to a slightly lesser extent in the U.S. Japan, still striving to hit a 2% inflation objective, has its inflation standing in the lower 21st percentile of its range. It is not part of the inflation love-fest.

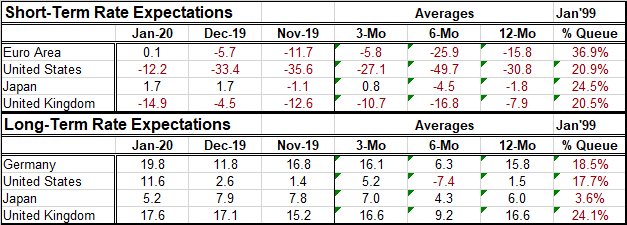

Interest rate expectations have uniformly lower standings than inflation standings for both long-term and short-term rates (where applicable). As such, the ZEW standings continue to envision a world in which real interest rates are going to remain below historic norms. Long-term and short-term rate expectations still were raised across the board except for a weakening in short-term rate expectations in the U.K. and weakening in long-rate expectations in Japan (Japan's short-term rate expectations were kept unchanged as well). ZEW forecasters continue to see anomalies but apparently believe that this configuration of lower interest rates will be enough to move growth higher as we see in the large shifts in current conditions and expectations assessments.

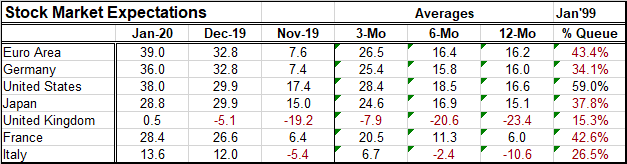

ZEW experts also see stock markets improving across the board except in Japan. The U.K. and Japan log very small stock market technical changes rather than any true 'economic' improvements. The U.S. has the most substantial stock market improvement even though Germany and France each log larger month-to-month changes in expectations and Germany and the U.K. have larger improvements in their month-to-month economic situation changes.

Much of the ZEW improvement is laid at the feet of the U.S.-China trade resolution, the so-called Phase-One deal.

"The continued strong increase of the ZEW Indicator of Economic Sentiment is mainly due to the recent settlement of the trade dispute between the USA and China...." (Source here).

However, this is only a phase-one deal and it leaves many high tariffs in place. While it does end the cycle of escalation between the U.S. and China, it is unclear how much growth is going to be improved from its current state. The U.S. and China still have more to do, the U.S. and the EU have yet to negotiate on trade, the U.S. and France have a tiff over a new French 'tech-tax' and, of course, the U.K. and the EU need to finalize their Brexit arrangement. In one short sentence, I want to make it clear that there is a lot yet to be done even has the vaunted U.S.-China deal itself has really done so little and leaves so much on the table to be finished. Still, we see a large impact in the ZEW assessments, much larger than any gains we are seeing in GDP reports (which are still deteriorating) and in sensitive PMI gauges (that are only hovering near their lows). Only time will tell if the ZEW experts have been unduly swayed by this closely-watched and much-written-about trade deal that did not get any of the hard work done, gathered only the low-hanging fruit, and left substantial punitive tariffs in place.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief