Global| Oct 13 2020

Global| Oct 13 2020ZEW Experts Reduce Expectations: The Thrill Is Gone?

Summary

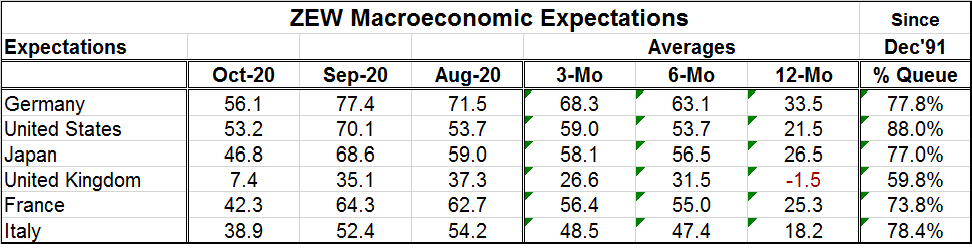

ZEW experts cut their expectations for Germany by 21.3 points in October. They slashed them by 16.9 points in the United States. They lopped 21.8 points off the outlook in Japan. The French outlook is weaker by 22 points in October. [...]

ZEW experts cut their expectations for Germany by 21.3 points in October. They slashed them by 16.9 points in the United States. They lopped 21.8 points off the outlook in Japan. The French outlook is weaker by 22 points in October. Italy is only 13.5 points light of its September assessment. The United Kingdom is weaker by 27.7 points. Despite these substantial decrements, the queue standings are still in the top 30 percentile of their respective queues of values except the U.K. The U.S. outlook is still in the top 12 percentage points of its historic queue of data. Still, there is a clear step back in October.

ZEW experts cut their expectations for Germany by 21.3 points in October. They slashed them by 16.9 points in the United States. They lopped 21.8 points off the outlook in Japan. The French outlook is weaker by 22 points in October. Italy is only 13.5 points light of its September assessment. The United Kingdom is weaker by 27.7 points. Despite these substantial decrements, the queue standings are still in the top 30 percentile of their respective queues of values except the U.K. The U.S. outlook is still in the top 12 percentage points of its historic queue of data. Still, there is a clear step back in October.

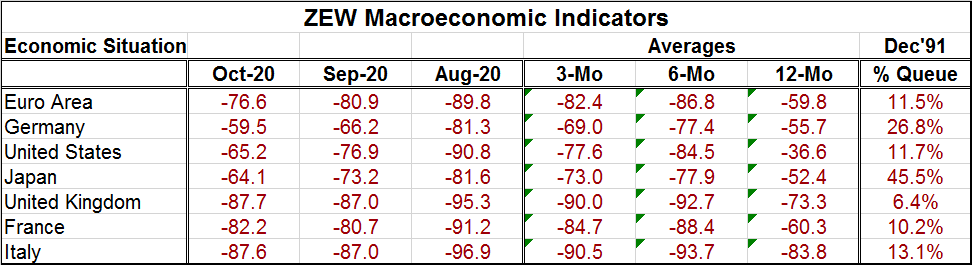

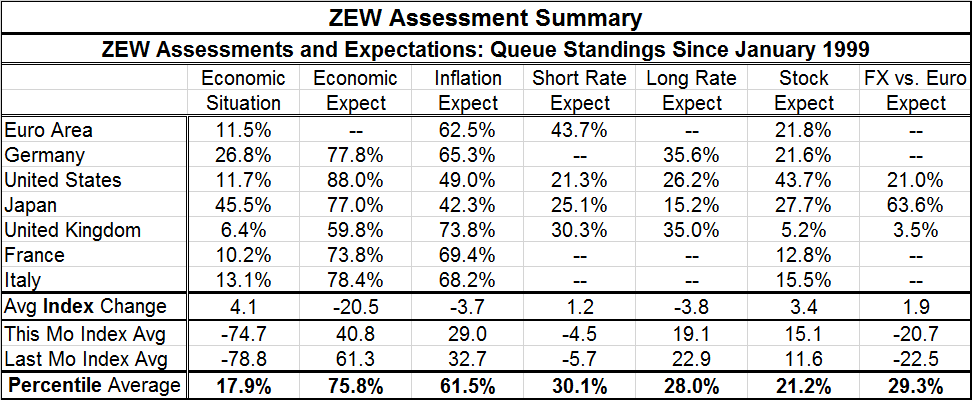

Macroeconomic assessments are stronger in the euro area, Germany, the U.S. and Japan, while slightly weaker elsewhere. And all retain quite low queue standings (except Japan).

Viewed in the aggregate (unweighted for country size), the economic situation improved by an average of four diffusion points. Economic expectations weakened by an average of 20.5 diffusion points. Inflation expectations weakened by an average of 3.7 diffusion points. Short-term rate expectations rose by 1.2 diffusion points on average while long-term rate expectations fell by 3.8 diffusion points. Stock market assessments gained by 3.4 diffusion points.

The average percentile queue standings show weak economic assessments of the current situation, and substantial optimism on the outlook. Moderate (just above median) inflation expectations are in force, still quite low short-term interest rates and long-term rates, to about the same degree, also are expected. Stock markets remain with weak readings.

The European outlook is being cut because soon Europe will be slowing as new antivirus procedures are being implemented across the continent. It is hard to handicap how long this next phase of procedures will be in place and even if it will need to broaden its net. For now all we know is that 'slower' is coming and that some countries are worse off than others. Of course, this refers to the spread of infection which is growing and not necessarily to any draconian increase in deaths or in hospitalizations.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief