Global| May 13 2014

Global| May 13 2014ZEW Expectations Step Back Sharply

Summary

The ZEW survey of current conditions and expectations for May is producing striking results. While the current index continues to show improvement rising to 62.1 in May from 59.5 in April and 51.3 in March, expectations have been cut [...]

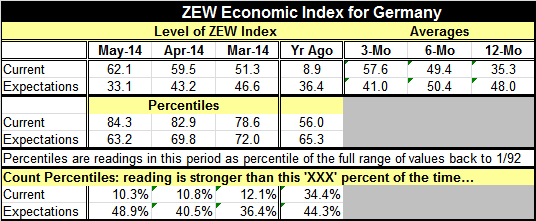

The ZEW survey of current conditions and expectations for May is producing striking results. While the current index continues to show improvement rising to 62.1 in May from 59.5 in April and 51.3 in March, expectations have been cut sharply. Against the background of steadily improving economy, the financial experts have cut their expectations for the future so sharply that historically they have cut them by more only 15% of the time. The expectations index for May fell to 33.1 from 43.2 in April. It stood at 46.6 in March. As recently as January 2014, the index stood at a level of 61.7. In just five months the expectations of the financial experts have been reduced by nearly half. The expectations index fell by 10.1 points in one month.

The ZEW survey of current conditions and expectations for May is producing striking results. While the current index continues to show improvement rising to 62.1 in May from 59.5 in April and 51.3 in March, expectations have been cut sharply. Against the background of steadily improving economy, the financial experts have cut their expectations for the future so sharply that historically they have cut them by more only 15% of the time. The expectations index for May fell to 33.1 from 43.2 in April. It stood at 46.6 in March. As recently as January 2014, the index stood at a level of 61.7. In just five months the expectations of the financial experts have been reduced by nearly half. The expectations index fell by 10.1 points in one month.

At a level of 62.1, the current index post a stronger reading only 10.3% of the time historically. At a reading of 33.1, the expectations index shows a stronger reading about 51% of the time. That means it has a weaker reading about 49% of the time. Those metrics imply the German view of the future getting better or worse, at a faster-than-normal pace, is essentially a coin toss.

Despite the strong markdown in expectations, there's been little impact on the outlook for profitability in the stock market by the ZEW experts. Stocks are rated at a +3.5, up slightly from their +3.3 reading in April. The reading for stocks was last higher in January and prior to January the readings had been persistently higher. The readings for bonds also improved slightly to -7.2 from -7.8. This is a negative reading and not a very strong reading for the bond market.

Of the 13 stock sectors that the financial experts evaluate, only four of them improved in May compared to April: chemicals and pharmaceuticals rose to the highest relative standing with their profitability expectations above their May rating at a value that is higher only about 15% of the time. Expectations for profitability in the services sector also improved. There are improvements for insurance and telecoms although both of those sectors continue to be evaluated at levels that are still historically weak.

Although the current conditions continue to be marked as improving by the financial experts, recent important German reports ranging from new orders to industrial output have showed a setback in economic conditions in Germany.

Germany is at risk if further sanctions are placed on Russia for its actions in Ukraine. Although the German economy is not heavily dependent on Russian purchases, there are parts of Germany that are very dependent. There is always a political vehicle for such regions to seek redress. Angela Merkel has been outspoken about her reluctance to approve any further sanctions on Russia. German business groups have been quite outspoken about their opposition to any further sanctions. On the other hand, events in Ukraine, including the tampering by Russia in Ukraine's domestic affairs, seem to continue to worsen. Undoubtedly, the financial experts are looking at things like this when they downgrade their view of the future.

Expectations are at a position where they can be considered `equivocal'. They are still positive (more experts see things improving than seeing things deteriorating), but the positive level of the indicator which nets pessimists against optimists is only where it has been historically. The current value sits almost on top of its historic median. We take this to mean that the ZEW financial experts look for some modest growth, but they are uncertain about what happens next. Since they are the experts, maybe we should take their concerns to heart.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief