Global| Nov 17 2015

Global| Nov 17 2015Zew Expectations Rebound but Do Not Change the Story

Summary

Zew expectations jumped in November, rising to an index level of 10.4 from 1.9 in October. Still, the level in November is below the level in September which stands at 12.1. The November expectations index standing has been stronger [...]

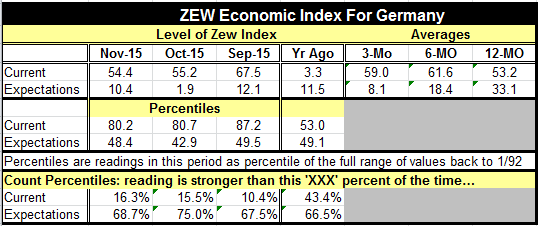

Zew expectations jumped in November, rising to an index level of 10.4 from 1.9 in October. Still, the level in November is below the level in September which stands at 12.1. The November expectations index standing has been stronger 68.7% of the time. Despite the rebound, the level of expectations is still quite near the bottom one-third of its historic queue of ordered data.

Zew expectations jumped in November, rising to an index level of 10.4 from 1.9 in October. Still, the level in November is below the level in September which stands at 12.1. The November expectations index standing has been stronger 68.7% of the time. Despite the rebound, the level of expectations is still quite near the bottom one-third of its historic queue of ordered data.

The Zew current index has edged lower to 54.4 from 55.2 in October. The current index is down sharply from its September level which stands at 67.5. So the two-month stability is at a much-reduced level, but the percentile queue standing is not reduced by nearly that much. The percentile standing of the current index is positioned at the 16.3 percentile implying that it - and the German economy- are stronger only 16.3% of the time. Despite the relatively low standing of the expectations index, the current index is at a relatively elevated level. The German economy is still doing just fine.

The Zew index shows that Germany is not being battered in the wake of the problems at Volkswagen. Not only that, but car registrations were still strong across Europe in October. Registrations rose by 2.9% from one year ago, slower, of course, than the previous month's torrid 9.8% rise, but still a very solid pace of expansion. However, there is now another threat to growth, and not just in Germany.

The terrorist attacks in Paris have put all of Europe on notice. Victor Constancio, ECB vice president, has warned of potential adverse consequences. As far away as the United States of America programs that had been put in place to absorb migrants are being halted. Stoppages are occurring across a number of states by their governors. Governor Rick Snyder of Michigan said he was suspending the acceptance of new refugee arrivals until a review had been conducted. Alabama, Texas and several other states have issued similar statements. However, a State Department spokesman said the legality of these actions was still unclear. Do the states have rights or is this a matter of federal jurisdiction? President Obama in a speech from Turkey yesterday admonished people to not cower and instead to step up and provide aid and shelter where it is needed to these refugees.

The threat of terror is now seen as palpable in the wake of the Paris attacks which may have employed some migrants but seem to have leaned heavily on operatives already in place. In Germany the head of the German police force said that there is no evidence that Islamist militants posing as refugees have entered Germany to launch an attack. However, other European countries are building fences on their borders to control the flow of migrants. There is still a very country by country sense of approach to this problem despite the fact that the EU is trying to impose general policies for the treatment of migrants.

There are many economic cross currents battering the global economy and now special concerns are afoot in Germany's most important corporation and because of geopolitics all across all of Europe.

The economic footing is still not solid. The rise in Germany's Zew index this month is encouraging but conditions are still reduced from what they were just a few short months ago and with heightened risks in play.

Christopher Kent, Assistant Governor of the Reserve Bank of Australia, today warned that there are factors that continue to hold back commodity prices. Inflation is still undershooting in Europe, where the central bank has only an inflation mandate, and in the US where the October CPI just showed a year on year rise of 0.2%. While the ECB is probably set to undertake more stimulus, the Federal Reserve seems on a set path to hike rates. If these two central banks do actually head out on divergent courses we can expect some considerable reactions by markets. Central bank activity is far from being fully discounted by markets. Draghi still faces opposition in Europe. At the Fed there seem to be as many opinions on what to do and how to do it as there are FOMC members. All this means that markets still have unanticipated events to react to. Be prepared.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief