Global| Dec 13 2016

Global| Dec 13 2016Zew Expectations for Germany Are Unchanged as the U.S. Is Off to the Races

Summary

The main take away from the Zew report in December The main take away from the Zew report in December is that globally conditions are in flux. Brexit is an issue, Zew experts see Italy deteriorating. The US is expected to perform [...]

The main take away from the Zew report in December

The main take away from the Zew report in December is that globally conditions are in flux. Brexit is an issue, Zew experts see Italy deteriorating. The US is expected to perform better- like him or not Trump is being credited for higher growth expectations. Inflation looks to be climbing higher everywhere except where its need most: in Japan. Growth in Europe is still moderate and expectations there are below par.

The main take away from the Zew report in December

The main take away from the Zew report in December is that globally conditions are in flux. Brexit is an issue, Zew experts see Italy deteriorating. The US is expected to perform better- like him or not Trump is being credited for higher growth expectations. Inflation looks to be climbing higher everywhere except where its need most: in Japan. Growth in Europe is still moderate and expectations there are below par.

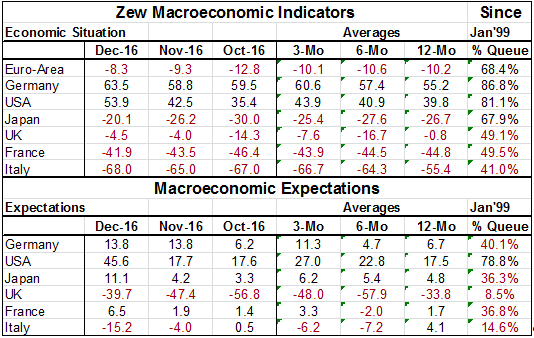

The current economic situation

The Zew economic situation for the Euro-Area and five select countries shows near median conditions in the U.K. and in France. Japan trails with a 41 percentile standing. Japan and the whole of the Euro-Area log near 68th percentile standings. But the US and Germany have standings in their respective 80th percentiles. Conditions in Germany and in the US are relatively strong, stronger than this less than 20% of the time.

Growth expectations

Expectations for the six countries are another matter. They are uniformly lower than readings for the current economic situation across the board. All except the US have expectations below their historic median (median occurs at a percentile of 50). Like other measures concerning the US, expectations jumped in the wake of the presidential elections. The US expectations index jumps from 17.7 in November to 45.6 in December and to a standing of 78.8% nearly the same as for economic conditions. Europe apparently buys into the notion that Trump will ignite growth. Most other countries show some improvement in expectations for November to December albeit small improvements. The exception is Germany where expectations are unchanged and Italy where expectations have plummeted from a -4 reading in October to a -15.2 reading in December. Still expectations for the U.K. are lower in their raw diffusion level as well as their percentile standing than for Italy.

On balance the US is on the move. Germany is solid with middling to soft expectations. The U.K. and Italy have troubled outlooks. The outlook for France and Japan more or less are the same as for Germany. This is the Zew, German financial expert, view of the world.

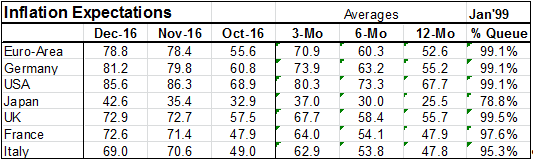

Table 2 chronicles inflation expectations. For December expectations are in the top one percentile for the Euro-Area, for Germany for the U.K. and for the US. They are in the top 5% or better for Italy and France and are only at a more moderate 78.8 percentile for Japan, where the central bank would almost kill to get inflation higher. However, these ranking are not new. Despite much more optimism on US growth, the US inflation expectation reading actually backed off a tad in December. Inflation expectations are little changed between November and December. November took a sizeable step up for all regions/countries. There was a gain in the basic indices month to month of about 20 points in November compared to October with the exception of the U.K whose monthly gain was about 15 points and Japan where its monthly gain was a meager 2 1/2 points. Still the percentile standings on inflation are much higher than they have been in some time. This explains why Jens Weidmann has been making strong statements about how the ECB needs to look only at inflation to make policy.

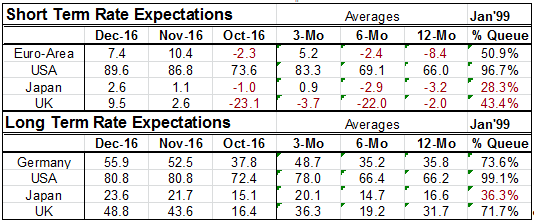

Interest rate expectations

Table 3 looks at short and long term interest rate expectations. In both cases the rate expectations were changed substantially in November as they moved up to higher levels. For short rates the main exception was Japan where a small step up occurred. In December expectations for short rates have not changed by much except for the UK. For long term rates there was a more considerable shift up in November, followed by small upward movements in December (except in the US where long term expectations are unchanged). For the US rate expectations are in the top 1% of their queue of values since early 1999. The UK and Germany have expectations standing their respective 70th percentile. Japan's long term rate expectations have a 36 percentile standing, well below their median.

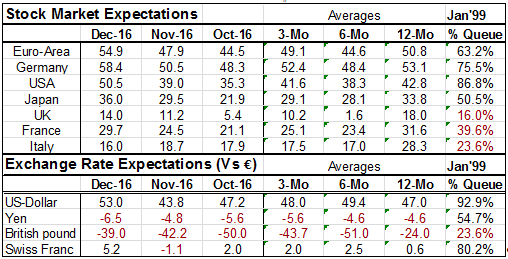

Stock markets

Stock market expectations have generally stepped up country by country and month by month except for Italy which has backtracked in December. For the UK.., France and Italy expectations are generally subpar, below their historic medians. Japan has a prototypical median report with a 50.5 percentile standing. The Euro-Area as a whole is a bit better with a queue standing in its 63rd percentile; Germany's is better still in its 75th percentile. The US has a stock expectation standing that is better historically only about 13% of the time.

Exchange rates

As to Zew expert expectations for the euro, they look for the dollar to get stronger as the dollar expectation has 92.9 percentile standing and is quite strong. No surprise with the Fed alone braced to hike rates. The Swiss franc has an 80th percentile standing, also relatively strong. The yen has a near median standing at its 54th percentile but the pound sterling is expected to continue to be weak as it has a standing that has been weaker less than 25 percent of the time.

Oil

The Zew experts also weigh in on oil prices. Despite the recent OPEC announcement the Zew assessment for oil prices actually fell in December relative to November. Either forecast submissions to Zew from the experts were made ahead of the recent Saudi announcements or the Zew experts are Saudi skeptics. Still, at their December level, Zew expectations are higher less than 15% of the time. So that even though the Zew experts' outlook for oil price did not change much in the current month the Zew survey is looking for oil prices to rise and that expectation is relatively strongly held.

Summing up

There are for various reasons big changes in the recent months in both conditions and expectations. We see in the Zew survey the impact of Brexit on the UK market, on inflation, on interest rates, and on the exchange rate. For Italy we see downgraded expectations in the wake of its failed referendum and the resignation of its Prime Minister. In the US we see a huge upward revision in growth expectations coinciding with the election of Donald Trump. In the last two months inflation expectations are up relatively sharply and broadly as well. Zew experts are relatively upbeat on the US and seem to see slow progress in Japan. Clearly they are more concerned about the EMU inflation situation than they have been in the recent past. Meanwhile in Europe growth is only moderate and expectations remain sub-par.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief