Global| Jul 15 2014

Global| Jul 15 2014ZEW Expectations Continue to Sink

Summary

The ZEW index in June saw its current component backtrack for the first time in eight months while the expectations reading fell for the seventh month in a row. The current reading had improved for seven months in a row until this [...]

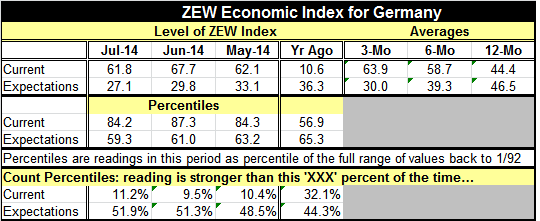

The ZEW index in June saw its current component backtrack for the first time in eight months while the expectations reading fell for the seventh month in a row. The current reading had improved for seven months in a row until this month.

The ZEW index in June saw its current component backtrack for the first time in eight months while the expectations reading fell for the seventh month in a row. The current reading had improved for seven months in a row until this month.

The current index is stronger than its current level only about 11% of the time while the expectations value is higher about 51% of the time. That means that the current situation is still considered extremely good, but expectations are at a level of relative uncertainty. Since the economy generally grows over time, a reading that is at its historic middle is one that expects growth to continue. But expectations can no longer be called `upbeat'.

The ZEW financial experts cut their expectations for earnings on stock to 2.6 in July from 2.8 in June. This is its lowest reading in 19 months. The outlook for bonds remains negative, but after improving last month it back to deteriorating. Apart for last month, it was last higher in November.

This shift, to favor stocks less, reflects some degree of pessimism. It fits with the slide in expectations, slippage in the Ifo survey, dropping industrial production and weakening Markit PMI sector readings. The slippage in ZEW expectations tells us that these weaknesses in the German economy continue.

They are accompanied by a weakening across much of the euro area, especially in the factory sector. The German current reading has finally stopped moving up and drooped back this month. The signal from expectations remains remote. Expectations that sour do not always lead to worse conditions ahead. The German Ifo expectations index does not have a good forecasting record in that regard. Still, its weakening does not stand alone and the current index does reflect some of the actual weakness we have seen in topical German activity measures.

Clearly, Europe is a place where we want to keep our eyes open. The recent weakness in Germany has been accompanied weakness elsewhere. Other nations in the European Monetary Union do not have as much growth to work with as Germany and weakening in those places could become more of a problem. Remember that Germany's own expectations are in the midst of a six-month slide.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief