Global| Mar 16 2021

Global| Mar 16 2021ZEW Expectations Continue to Climb

Summary

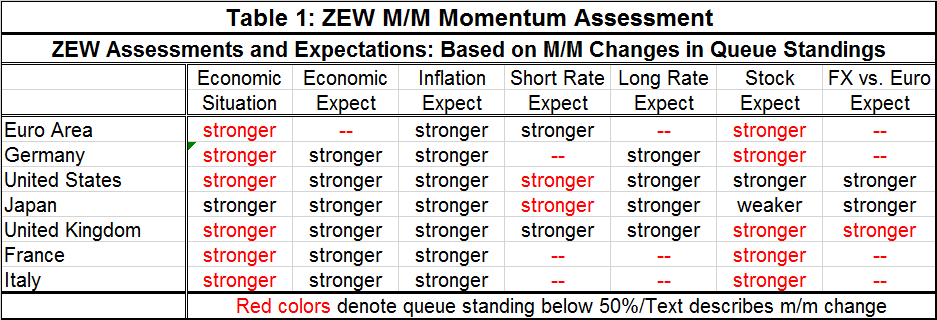

The table suggests that the operative word for the ZEW survey this month is 'stronger.' Readings improved in 34 of 35 non-foreign exchange related categories that assess macroeconomic conditions, markets and inflation. In fact, the [...]

The table suggests that the operative word for the ZEW survey this month is 'stronger.' Readings improved in 34 of 35 non-foreign exchange related categories that assess macroeconomic conditions, markets and inflation. In fact, the report was amazingly strong and consistent this month as the average change across categories was eight points 'plus change' except for the stock market where the average gain was about half that at 3.9 points- again I excluded the FX assessments from this summary statement. The use of color in the table is a proxy for the behavior of the underlying diffusion rankings being above their medians (50%) vs. below their medians. Once again only 13 of 35 macro, market and inflation readings were below their respective medians. So the absolute readings are on firm ground and momentum is very solid.

The table suggests that the operative word for the ZEW survey this month is 'stronger.' Readings improved in 34 of 35 non-foreign exchange related categories that assess macroeconomic conditions, markets and inflation. In fact, the report was amazingly strong and consistent this month as the average change across categories was eight points 'plus change' except for the stock market where the average gain was about half that at 3.9 points- again I excluded the FX assessments from this summary statement. The use of color in the table is a proxy for the behavior of the underlying diffusion rankings being above their medians (50%) vs. below their medians. Once again only 13 of 35 macro, market and inflation readings were below their respective medians. So the absolute readings are on firm ground and momentum is very solid.

The current and the future

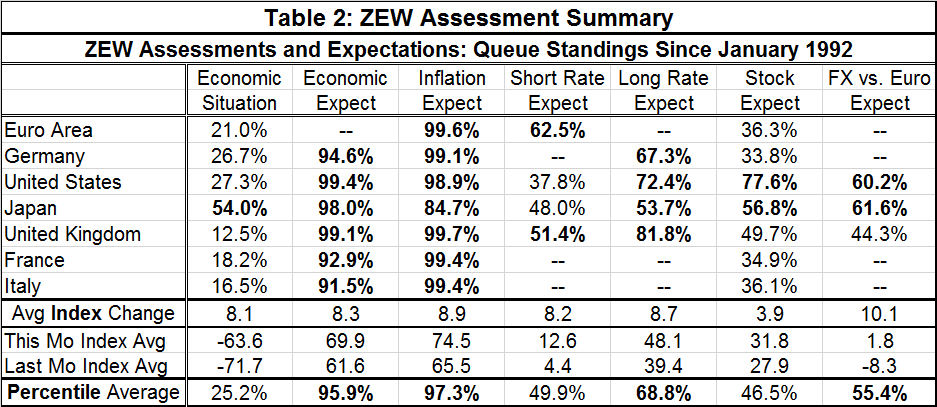

Table 2 below reveals the magnitudes behind the Table 1 results. Here we see some remarkable trends. While the 'economic situation has been steadily improving since it collapsed in April of last year, the road higher has been very slow going. The average current diffusion reading is only -63.6 with a percentile standing average at a 25.2 percentile standing. Expectations average a much higher 69.9 diffusion reading with an extraordinary 95.9 percentile standing. That is a huge standing for an average. The name percentile standing sounds like what they are, or represent, standings range from zero percent to 100% and they place the raw diffusion value in a queue of historic values to give it a percentile standing and to imbue the diffusion reading with more meaning. An average diffusion reading of 69.9 sounds like it might be pretty good, but when we associate it with a percentile standing of 95.5% the interpretations is considerably more precise and meaningful. Moreover, the table value represents the average of all the percentile standings of the seven jurisdictions in the table. That makes the high percentile values that much more impressive.

Room to move?

One thing that the table clarifies is that while the diffusion readings have space to grow (diffusion metrics are bounded by -100 and +100) the percentile standing that pertains to the readings on that scale already is quite near its technical maximum. For inflation the results are even more impressive as FIVE underlying countries/areas have standings in the top 1% of their respective historic queues of value. And while these values mean that inflation is very widely expected to pick up, inflation currently is extremely low. If inflation expectations were to shift markedly higher, there would really be no way even to represent that in the standings data. The underlying diffusion readings could rise, however.

Interest rates

Interest rate expectations show milder paths expected (the forecast for hikes is less widespread) for short rates compared to long rates. Of course, short rates are controlled by central banks and long rates are controlled by markets. Markets are expected to be reacting to expected inflation and expected growth even as central banks act in what is clearly expected to be lagging behavior. And equity markets are expected to be much less ebullient with an average percentile standing below the median and with only small gains in train for this month.

The future...

Clearly expectations are geared up, but the virus continues to circulate and hold back current levels of activity. This is why the continued ramp up in expectations does not have any impact on current assessments. While there is a current issue dogging the AstraZeneca vaccine, other vaccines are in a heavy use mode and making strong progress. There is optimism about the future, but in 'real time' the virus exists and hampers economic activity even in the face of optimism. The difference between the current and expectations modes is amazing not just because it is so great but because it has persisted for so long. The ZEW experts are so sure of recovery that they are also sure of inflation even though inflation has not been able to gain any real footing in over a decade. But these expectations are strongly held. Since bond markets yield expectations are not as nailed to the ceiling, we can infer that expectations for inflation, while strongly held, are not for inflation to get wildly out of control but apparently to seep in and creep up. Still, forecasts are just that and most forecasts are wrong most of the time.

Summing up

What we do not know is what part of the current forecasts will be wrong. How will today's expectations differ from tomorrow's actual outcomes? There is never an answer to that question because if we knew, it we would change our forecasts. What we do know is that we have a relatively strong consensus (a widely held view). What we don't have is a clear and unimpeachable timeline to normalcy. But we do have strong expectations that we are headed to normalcy. And there is endless speculation about what the finalized 'new normal' will look like. That remains an open issue.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief