Global| Jan 21 2014

Global| Jan 21 2014ZEW Expectations Back Off in January

Summary

The ZEW index which is the result of a survey of financial experts in Germany revealed a slight back off and expectations in January compared to December. The back-office light, but again had been expected. The current conditions [...]

The ZEW index which is the result of a survey of financial experts in Germany revealed a slight back off and expectations in January compared to December. The back-office light, but again had been expected.

The ZEW index which is the result of a survey of financial experts in Germany revealed a slight back off and expectations in January compared to December. The back-office light, but again had been expected.

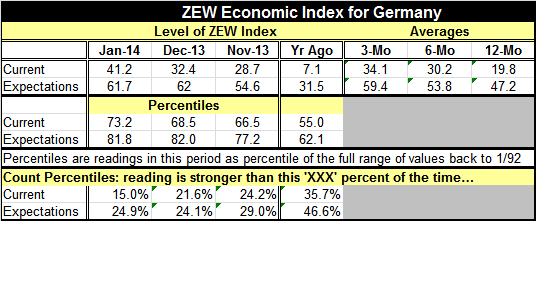

The current conditions portion of the survey made another strong gain, rising to 41.2 from December's 32.4. On the face of it, it may be curious that the economy can be thought to have improved so sharply and also expectations cut back slightly. However, the two assessments always are related.

The current index level of 41.2 is higher than this position only 15% of the time. Expectations, at a level of 61.7, are higher than this slot only about 25% of the time.

What the ZEW respondents seem to be saying is that the current economy has gotten to be so strong, higher only 15% of the time, that they are not so sure that it is going to continue to improve as fast in the future. Still, the expectations index is hardly weak. It is at the threshold of the top quarter of its historic queue. Despite the back off in the expectations reading, the German stock market continues to rise sharply.

When we compare the expectations for earnings across the major German stock market segments, we find declines from December to January only in the category consumption and trade. In December, there were increases from November in every category except for steel and metals, and that category has jumped sharply in January compared with the December level. On balance, expectations across the stock market segments are improving smartly and only utilities, insurance, and telecoms have readings that are below the midpoint of their respective ranges for ZEW earnings expectations. Banking, a sector that has lagged for some time, moved up sharply in December, and has moved up strongly again in January.

On balance, conditions in the European Monetary Union continue to improve. The environment around Germany is improving. The United Nations has increased its outlook for world economic growth as it sees a growth rate of 3% in 2014, up from 2.1% in 2013. Other news today tells us that European housing market continues to recover; that is another sign that the environment around Germany is improving and there should be positive feedback effects for the German economy from this pick-up.

However, the European Bank for Reconstruction and Development tells us that the emerging economies in Europe are still limping and are likely to continue to grow slowly.

The ZEW reading is for January and as such it is a new reading on the new month. We can't use previous observations to try to check what the ZEW reading is telling us. While the slowdown in expectations comes as a surprise, I think when viewed in tandem with the strong increase in current conditions the back off on expectations is more than understandable. The German economy is doing well, but the ZEW experts are telling us that they do not expect the economy to continue to build that kind of the head of steam. Germany after all is still operating in a flawed environment in the midst of a flawed euro zone run in part by a central bank whose policies are not fully supported by its members.

We should make sure to not overreact to the drop in the German expectations index. All the data that we have on Germany, and on the euro zone, tell us that growth continues to progress. One thing we know about economic indicators is that it is not a good idea to obsess over every single report. Some new data are telling us something and other observations are simply part of statistical noise. Ironically, I think the ZEW expectations index is telling us something, but to understand that, we need to consider the expectations reading in tandem with current conditions and the salient trends for the German economy. When we do this, I think we wind up with still a positive view of the German economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.