Global| Apr 21 2015

Global| Apr 21 2015ZEW Expectations Are Set Back As the Current Index Surges

Summary

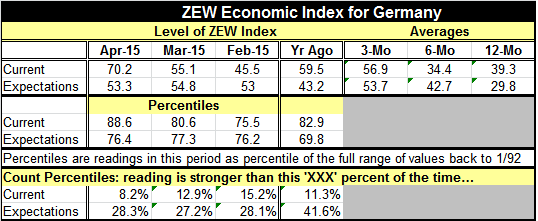

The ZEW expectations index was set back unexpectedly in April as it backtracked to 53.3 from March's 54.8. But at the same time the current index moved sharply higher. The one month rise in the current index is the fifth largest one- [...]

The ZEW expectations index was set back unexpectedly in April as it backtracked to 53.3 from March's 54.8. But at the same time the current index moved sharply higher. The one month rise in the current index is the fifth largest one-month gain since 1995. The current index has been moving up very sharply, in fact, its three-month gain is the fifth largest since late 1995.

The ZEW expectations index was set back unexpectedly in April as it backtracked to 53.3 from March's 54.8. But at the same time the current index moved sharply higher. The one month rise in the current index is the fifth largest one-month gain since 1995. The current index has been moving up very sharply, in fact, its three-month gain is the fifth largest since late 1995.

Any preoccupation with the small setback in the expectations index seems out of place. Expectations are formed relative to where the economy is. Since the current position of the economy has been moving higher, that would put greater strains on the ability of expectations to continue to see further advances.

At its April level, the current index has been higher only 8% of the time while expectations index has been higher 28% of the time. The current index is relatively stronger in the sense of its position in its historic range and it is appropriate that expectations for the future would begin to trim back as current economic performance is evaluated as some of the best ever. After all, how long can an economy continue to operate at the top of its game?

Against this background we are much less disturbed by the survey results from the ZEW financial experts and see the monthly backtrack as something that is wholly appropriate.

In this month's assessment, the evaluation of corporate earnings potential has improved to its third strongest reading in 18 months. The evaluation of the bond market is tied for its best in the last 74 months. Among 13 sectors evaluated, earnings expectations are improved month-to-month in five of them: utilities, construction, consumption/trade, steel/metals, and chemicals/pharma. The evaluation of the vehicles sector is weaker coming off its highest reading ever last month. Electronics and machinery, while lower on the month, still have extremely high earnings expectations.

On balance, the ZEW officials tell us that a number of industries are doing quite well and that the current environment is excellent. Against this background, some small setback in the expectations reading hardly seems to be the real news of this report.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief