Global| Jun 18 2019

Global| Jun 18 2019Zew Expectations are Beaten Back Again

Summary

The Zew experts' assessments of the global economy have taken a set-back in June. The set-back is broad in nature across countries/regions and across the surveyed gauges that the Zew experts assess. After some stabilization the [...]

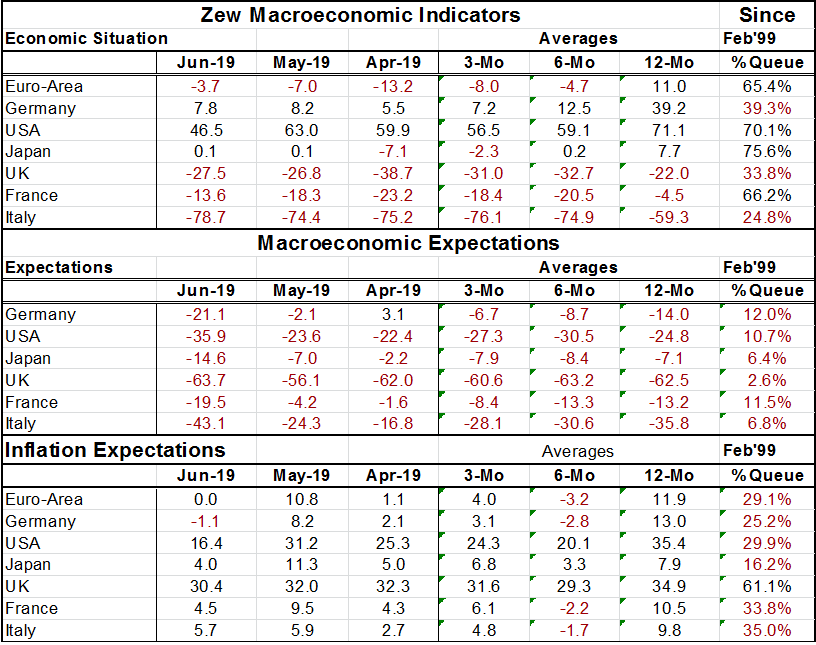

The Zew experts' assessments of the global economy have taken a set-back in June. The set-back is broad in nature across countries/regions and across the surveyed gauges that the Zew experts assess. After some stabilization the current assessment is weakening again. Macroeconomic expectations that had hit lows around the turn of the year for many of the surveyed countries are now back at readings of extreme weakness but only Japan has a new low in its Zew assessment on this horizon. Inflation expectations are low and generally fell sharply for members in June compared to May. Italy and the UK show a small decline in inflation expectations between the two months. For the group inflation expectations have fallen by more month-to-month only 17% of the time. For the US inflation expectations have fallen by more only 6% of the time back to 1992. For Japan inflation expectations have been cut month-to-month by more only 10.3% of the time, for Germany, the percentage is 17.6%.

The Zew experts' assessments of the global economy have taken a set-back in June. The set-back is broad in nature across countries/regions and across the surveyed gauges that the Zew experts assess. After some stabilization the current assessment is weakening again. Macroeconomic expectations that had hit lows around the turn of the year for many of the surveyed countries are now back at readings of extreme weakness but only Japan has a new low in its Zew assessment on this horizon. Inflation expectations are low and generally fell sharply for members in June compared to May. Italy and the UK show a small decline in inflation expectations between the two months. For the group inflation expectations have fallen by more month-to-month only 17% of the time. For the US inflation expectations have fallen by more only 6% of the time back to 1992. For Japan inflation expectations have been cut month-to-month by more only 10.3% of the time, for Germany, the percentage is 17.6%.

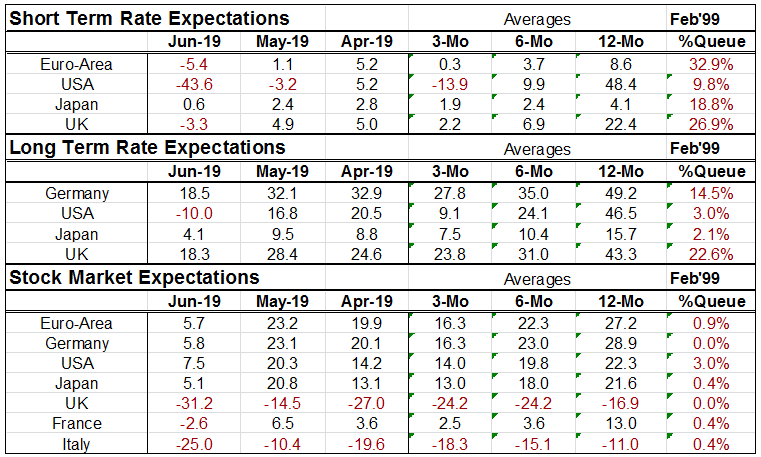

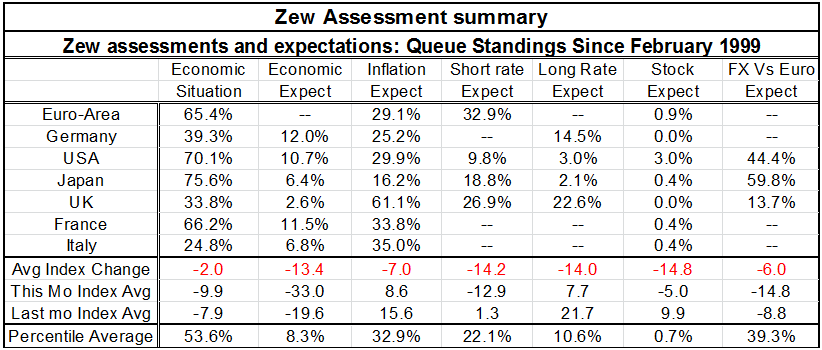

The average index change shows that monthly assessments were cut across the board in each category. The economic situation eroded just bit month-to-month but economic expectations, short rate expectations, long rate expectations and stock market expectations all fell double digits in terms of their average month-to-month survey assessment. Inflation expectations fell by a significant 7 points on average held down by small changes in the UK and Italy against a very large deterioration in the US.

Mario Draghi's remarks today dove-tail well with the new Zew survey that seems to echo Mr Draghi's concerns. Draghi's comments have caused the Euro to fall and that has raised one thing, the ire of US President Trump who accuses Europe of beggar-thy-neighbor policies. But that simply shows the President's misunderstanding of events. He is right about the impact on competitiveness which is his singular focus at the moment. But he is wrong to stew over it since markets have to move to reflect events and this is hardly a currency ‘manipulation event.' Still, it's an example of where we are in international policy. The US President is a bit of bull in china shop trying in one fell swoop to retrieve competitiveness lost by decades of poorly designed US policy and trying to reverse bad practices by US trade partners that have been tolerated for too long.

The "good news" on the day is that Trump as Xi are scheduled to meet soon at the G20 summit. However, we will not know until after that meeting whether that is truly good news or not. For now it is a potentially positive development.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief