Global| Dec 11 2018

Global| Dec 11 2018ZEW Assessments Shift and Weaken in December

Summary

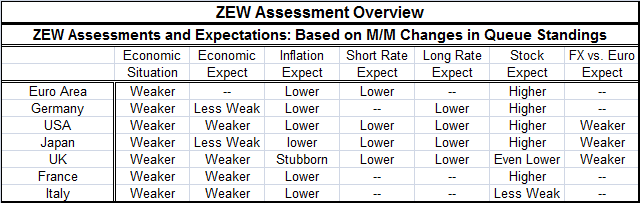

The 'text' table below summarizes the shifts in the ZEW assessments for December. Presented in this from with the magnitudes stripped out the month-to-month change in the assessments is starkly clear. • The economic situation has [...]

The 'text' table below summarizes the shifts in the ZEW assessments for December. Presented in this from with the magnitudes stripped out the month-to-month change in the assessments is starkly clear.

The 'text' table below summarizes the shifts in the ZEW assessments for December. Presented in this from with the magnitudes stripped out the month-to-month change in the assessments is starkly clear.

• The economic situation has worsened everywhere.

• Expectations are declining everywhere and only slightly less eroded in Germany and Japan.

• Inflation expectations everywhere are lower, usually sharply lower, except in the U.K.

• Short-term rates are seen lower (i.e., central bank policy swerves are expected).

• Long-term rates are seen lower, not surprising with reduced inflation expectations.

• Equities are better off than in November except for the U.K.

• The euro is seen as mostly stronger as a result.

The story this month is more about sweeping global macroeconomic changes and expectations than about country-level developments. Although there still are (obviously) differences by country, the assessment changes this month are wholly in one direction by category with just a few notable exceptions. The exception is often the U.K. as Brexit issues wash over and through the economy and as the pound sterling responds to various rumors or changes in circumstance. The other 'sometimes exception' is Italy with its weak economy and plan for fiscal largesse to the horror of the EU Commission.

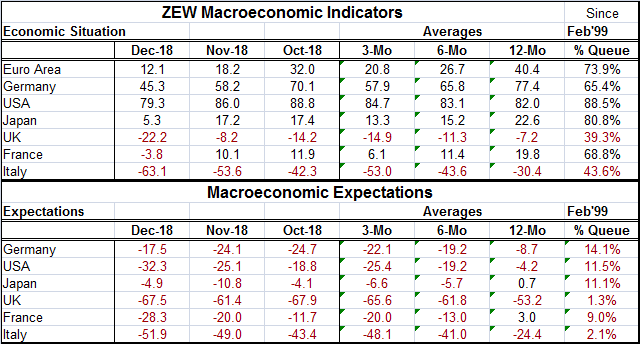

Macroeconomic conditions

Macroeconomic conditions now are fading across the board. Three economies reflect negative assessments and the downgrade for France has pushed it into a declining mode for the first time since September 2017. And with the protests that are going on there with yellow vests, conditions will continue to deteriorate despite President Macron's throwing bits of raw meat to the protestors. He apparently has fed them enough that there is some division of the ranks of the protestors already. But this is a fluid situation. The next phase will be to see how all these tax rescissions and the weak growth cause France to line up against Maastricht rules. Will France be a violator like Italy?

Year-on-year the largest deterioration in conditions is from Italy (-48.6 on actual monthly data), followed by the euro area (-38.6), followed by Japan (-23.9). Year-on-year the U.S. is the only country whose performance actually improves. Hail, hail, fiscal thrust…but pay us back someday you must!

Expectations

Expectations are highlighted by an improvement in Germany and Japan, the only ones showing improvement month-to-month and a real surprise at that. However, all assessments point to deterioration in December compared to November. Expectations year-on-year have deteriorated the most for Italy (-67.2), France (-60.1), and the U.S. (-47.4). But the queue standings show that evaluated relative to their individual histories all assessments lay somewhere in the lower 15% of their historic queue of data – no exceptions.

Some Specifics from the ZEW Survey Current and Expected Conditions

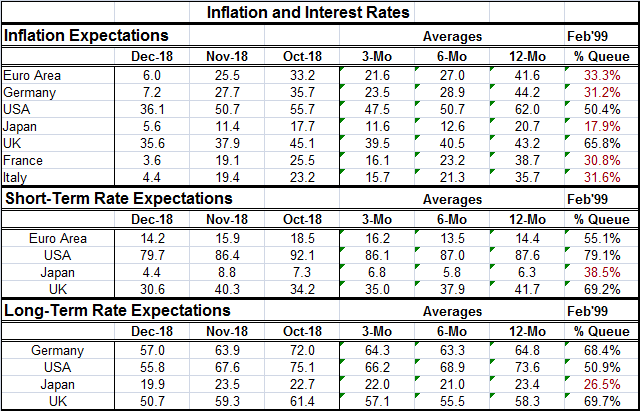

Inflation expectations

Inflation expectations are generally low, but all are positive and that is probably a good thing since deflation expectations usually go hand-in-hand with a very weak economic outlook. The inflation outlook 'improved' everywhere. I put 'improved' in quotes since Japan would prefer to see its inflation rising rather than falling by more. Queue standings for inflation expectations are below their medians (50% queue standing) everywhere except in the U.K. and in the U.S. For the U.K., this is a Brexit issue coupled with exchange rate weakness. For the U.S., it reflects the fact that U.S. inflation is at its Fed-desired goal. That observation may be a touch out of date with some of the recent inflation developments. But there is no doubt that U.S. inflation is higher than inflation in the EMU, which remains substandard. For the U.S., the inflation assessment is barely above its median value. For most table-members, the inflation assessment is near its one-third queue-ranking (the euro area, Germany, France, and Italy). For Japan, it has a 17th percentile standing.

Interest rates short-term

Short-term interest rate expectations, essentially a proxy for monetary policy, show vastly different queue standings but all of the readings did fall in December. And the euro area, the U.S. and the U.K. all have readings that lay above their respective historic medians; only Japan has a below-median reading for short-term rate expectations.

Interest rates long-term

As for long-term rates, all assessments are lower in December and readings are clustered within the 50-60 range for the raw diffusion metrics except for Japan that is lower. However, on a queue standing basis, the U.K. and Germany are at nearly the same queue standing even though German short-term rates (euro area) are lower in diffusion terms and lower in queue standing. The U.S. has the second lowest queue standing for long rates despite having the highest by far standing for short-term rates. Thus, ZEW participants seem to be very aware of the flatness of the U.S. yield curve. But at the same time, they don't seem to know what it means since they also have a relatively high (50.4 percentile) queue standings for U.S. inflation expectations. No one really seems to have a good grip on why U.S. long-term rates are so low.

The gathering storm

IMF First Deputy Managing Director David Lipton warns of storm clouds gathering over the global economy, an ominous allusion to the title of Winston Churchill's famous book about global geopolitical conditions in the period ahead of the onset of World War II. Whether that allusion was purposeful or not, I cannot tell. But in his talk, Mr. Lipton warned of central banks being caught without the proper tools to fight back. How big is the risk? It's massive. But whether we will be visited by such harsh realities or not depends on whether rogue nations will come to heel and obey the rules necessary to conduct fair trade on an international scale. On this we may be hopeful, but in truth we have no reason to be.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief