Global| Dec 08 2020

Global| Dec 08 2020ZEW Assessments Are Mixed in December with Expectations on the Mend

Summary

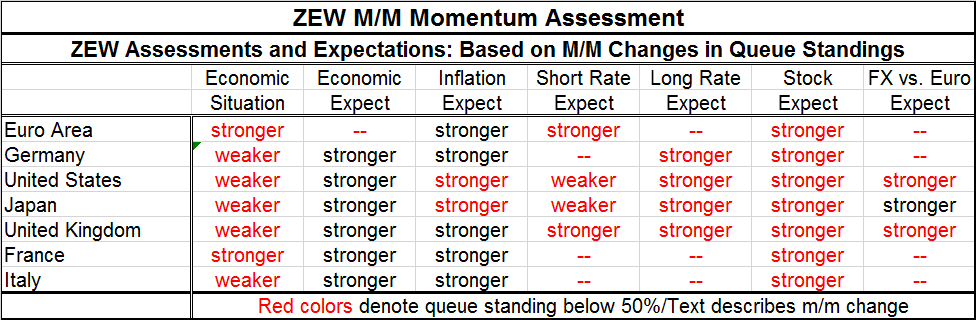

The economic situation in December is assessed as mixed by the ZEW experts with two regions (the EMU and France) deemed stronger and the rest weaker. Economic expectations are firmer across the board, however. Inflation is seen as [...]

The economic situation in December is assessed as mixed by the ZEW experts with two regions (the EMU and France) deemed stronger and the rest weaker. Economic expectations are firmer across the board, however. Inflation is seen as stronger than it was a month ago. Expectations for short-term rates are mixed across countries and regions while long-term rates are expected to be higher everywhere. Stocks are gaining a firmer hold and their percentile standings are moving closer to a reading of normalcy (50%) and the average stock market standing is now above that mark (France, Italy and the U.K. are not there yet).

The economic situation in December is assessed as mixed by the ZEW experts with two regions (the EMU and France) deemed stronger and the rest weaker. Economic expectations are firmer across the board, however. Inflation is seen as stronger than it was a month ago. Expectations for short-term rates are mixed across countries and regions while long-term rates are expected to be higher everywhere. Stocks are gaining a firmer hold and their percentile standings are moving closer to a reading of normalcy (50%) and the average stock market standing is now above that mark (France, Italy and the U.K. are not there yet).

On balance, there is a lot of consistency here and reason for some underlying or general optimism. The current situation is mixed as noted above because of the current impact of the virus. But lockdowns that created that weakness are coming off in Europe and so quite apart from the current impact expectations are more upbeat. In addition, there is the expectation of the vaccine which is actually being rolled out and administered in the U.K. today. This also explains why short-term rate expectations are mixed but long-term expectations are rising since the vaccine is supposed to help restore economic normalcy. Stocks also are stronger across the board consistent with a more upbeat future; their average percentile standing above 50% a clear signal of more normal times ahead being expected.

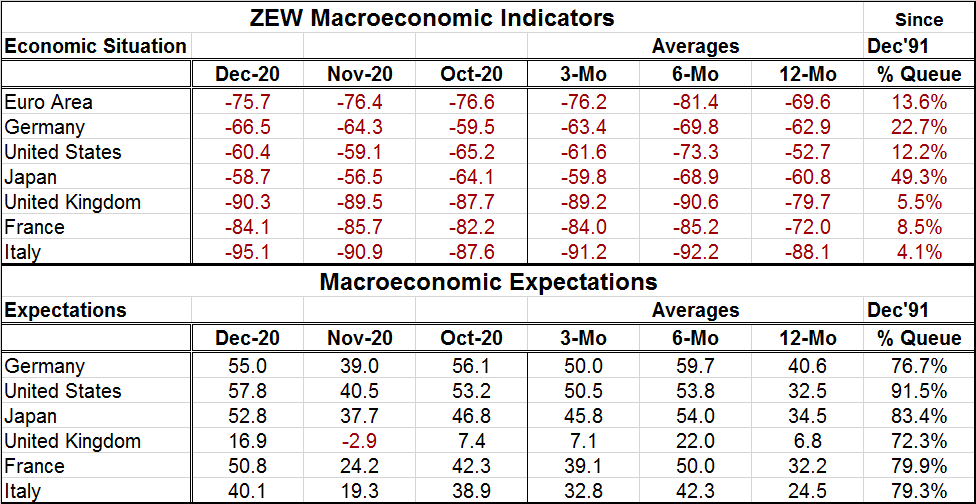

Still, the table below reminds us of how weak the current readings remain. While monthly improvements were present in only 2 of 7 reporters, in truth here was little change anywhere in December (exception: Italy more significantly worsened). In fact, the three-month averages are generally weaker than the 12-month averages (Japan excepted) and those two averages are also usually close in value. The virus has kept all these economies on the wrong foot since April. The current queue standings are miserable, weak everywhere except for Japan where they are close to normal with a 49.3 percentile standing.

Expectations are strong on the month and are better by a good measure everywhere. The queue standings of the expectations reading range from a 72.3 percentile low in the U.K. to a 91.5 percentile high in the U.S. Current readings are well above three-month average and three-month averages are well above 12-month averages. Expectations clearly are gaining momentum and expectations have relatively high values to boot.

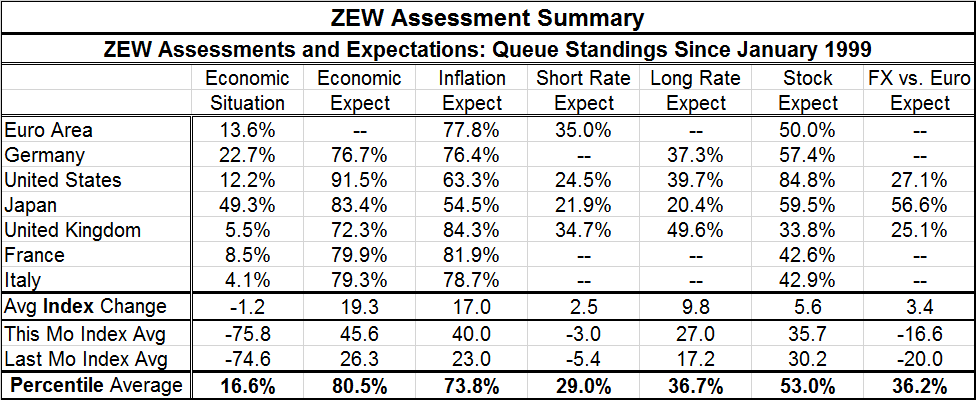

The table below reports the summaries of the various readings The average current percentile standing is at 16.6% compared to avera.ge expectation at 80.5%. That’s a huge difference. Inflation expectations are climbing to and on average are up to a 73.8 percentile standing, well above their median which occurs at a 50 percentile standing. The U.K and France have the highest inflation expectations standings followed closely by Italy, the euro area and Germany. Japan and the U.S. are low on this metric. While all short-term rate expectations are low and well below their respective medians, the U.S. and Japan are a bit lower than the rest. However, for longer terms rates, the U.K., the U.S., and Germany have the highest expectations (still below their historic medians) with Japan on the weak side. Stock expectations indicate the view of coming normalcy and represent the degree of hope placed on the vaccine.

Vaccine hope or madness?

Vaccine rollout has begun in the U.K. and may be starting in China and in Russia soon. The U.S. is preparing for emergency rollout and then we will be in the hands of the stock of vaccine, logistics, prioritization, and manufacturing. And as you tick through that list, you get the idea that the process is going to move ahead at a moderate speed because some things just can’t be rushed. There is some controversy about how much vaccine the U.S. has bought and will be able to get beyond the 100 million doses it has pre-purchased (that number is good to immunize 50 million people in a country of 330 million). Some vaccine optimism makes sense, but we need a reality check as well.

Reality check

In addition, there is a question of ongoing government support for those who the virus has dislodged and how that support will continue as economies get up to speed. In the U.S., some special programs for those disrupted by the virus are set to end and that could inject chaos in the economy including not just the expiration of extended unemployment benefits and other stimulus but rules that have allowed people to delay paying their rent and still avoid eviction. It is hard to see how that set of rules can be normalized without harming the people it is has so far protected. At the same time, landlords, some of them, themselves small businesspeople, need rent checks to pay their expenses. So there is still a tangle of trouble ahead. Vaccines may be a ‘cure’ but they will not be a cure-all. Legacy effects from the virus and actions to contain it will continue to haunt the global economy in various ways.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief