Global| Dec 10 2019

Global| Dec 10 2019ZEW Assessments and Expectations Improve But Gain Less Markedly

Summary

The ZEW global macroeconomic assessments have improved along a broad front in December following a surge of improvement in November. The improvements logged this month are more modest, but they continue the direction of change as [...]

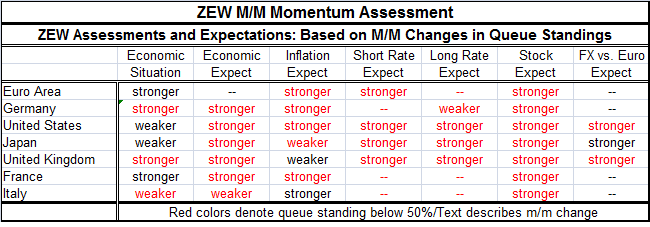

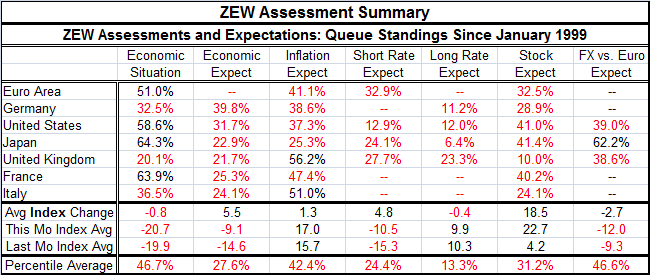

The ZEW global macroeconomic assessments have improved along a broad front in December following a surge of improvement in November. The improvements logged this month are more modest, but they continue the direction of change as positive. Of the 38 assessments made, 82% of them showed stronger readings month-to-month. The table below presents a textual overview with colors used to discern the underlying queue percentile level standings above their respective medians (above a 50 percentile standing black lettering is used). There are clearly few observations above the 50% median mark. There are none for economic expectations, none for short- or long-rate expectations or for stock market expectations. The United Kingdom and Italy have above median expectations for inflation while the present economic situation is above its median reading for the euro area, the United States, Japan, and France. Conditions of all sorts preponderantly are below their median marks, with the medians established over the period since early-1999.

The ZEW global macroeconomic assessments have improved along a broad front in December following a surge of improvement in November. The improvements logged this month are more modest, but they continue the direction of change as positive. Of the 38 assessments made, 82% of them showed stronger readings month-to-month. The table below presents a textual overview with colors used to discern the underlying queue percentile level standings above their respective medians (above a 50 percentile standing black lettering is used). There are clearly few observations above the 50% median mark. There are none for economic expectations, none for short- or long-rate expectations or for stock market expectations. The United Kingdom and Italy have above median expectations for inflation while the present economic situation is above its median reading for the euro area, the United States, Japan, and France. Conditions of all sorts preponderantly are below their median marks, with the medians established over the period since early-1999.

The table below provides more specific readings by country and area. While more countries and regions improved on the current reading than deteriorated, the deterioration was severe for Japan and Italy causing the average index change for the group to decline despite a slightly greater number of reporters improving. Economic expectations improved on balance by 5 diffusion points and inflation expectations ticked up by 1.3 diffusion points. Short-rate expectations rose by 4.8 diffusion points while the long-term average rate assessment fell by 0.4 diffusion points as the expected drop in Germany alone dominated expected gains in the U.S., Japan and the U.K. Stock market assessments improved here with a lag marking an average 18-point rise, basically reflecting the shift in expectations pronounced last month.

In terms of the raw diffusion readings...

• Only the U.S. has a current economic situation reading that is positive; all the rest of the readings are negative. However, in percentage standing terms, France and Japan have stronger relative queue readings than the U.S.

• For expectations, only Germany has a diffusion reading above zero although Japan’s reading moved up to zero in December. Germany’s positive queue standing has a near 40th percentile standing, still below its median (which occurs at a 50% standing); the U.S. has the next strongest macro-expectation with an above 30th percentile reading.

• All inflation expectations are positive – there is no deflation expected. There is above median inflation expected in the U.K. and Italy; France is pushing that envelope but still is below the 50% mark for its queue standing.

• Short-term rate expectations are mostly negative with Japan the exception having a small positive diffusion reading. The U.S. has the largest negative diffusion reading and the lowest percentile standing below its 14th queue percentile.

• In contrast, long-term rate assessments have uniformly positive diffusion readings with countries showing respective queue standings at the 12th percentile mark or lower except for the U.K. whose standing is at the 23rd queue percentile- still weak. This is consistent with the inflation expectations.

• Stock market diffusion made the largest leap of the week with market expectations now uniformly positive except for the U.K. Percentile standings for equities are in the 40th percentile for the U.S., Japan and France. Other country readings are lower with the U.K. at a 10th percentile queue standing, the weakest of all in December.

On balance...

The ZEW experts are more upbeat. The trend to improved readings is clear strong and widespread. However, while the economic situation has improved to over a 50 percentile reading in four reporters, the current experience remains uneven and even the strong U.S. standing eroded month-to-month in December. Expectations continue to improve and two of six reporters lost their negative outlooks. Still, in percentile terms, even these positive or neutral outlooks remain historically weak. While inflation expectations have crept up, they remain historically weak. After a sizeable gain a month ago, inflation expectations made only small increases in December. The interest rate outlook for both short- and long-term rates remains benign. The big improvement on the month was for equites where subpar ratings are still inforce. The pending U.S.-China trade deal has generated a good deal of optimism, especially for the fortunes of corporations trapped in the purgatory of uncertainty. Can – or will- a U.S.-China trade deal fulfill these expectations? There is also a new U.S. North American Trade treaty that is getting renewed attention and now seems likely to be adopted. With the U.K. elections nearly here, the Brexit uncertainty is expected to be swept away soon. There is reason for optimism on the corporate front. And some recent economic reports have been surprisingly firm. Still, there has been a lot of optimism injected into markets in the last few months. Will that optimism be rewarded by reality or not? That is the question.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief