Global| Jul 06 2009

Global| Jul 06 2009Worse Vs Much Worse...

Summary

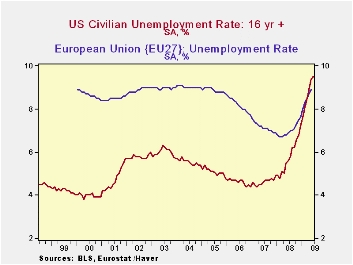

The accompanying chart makes the point that US rate of unemployment has risen a lot and Europe’s has risen by a little. Still the higher US rate of unemployment will fall sharply in recovery whereas Europe’s history suggests that its [...]

The accompanying chart makes the point that US rate of

unemployment has risen a lot and Europe’s has risen by a little. Still

the higher US rate of unemployment will fall sharply in recovery

whereas Europe’s history suggests that its rate will remain above the

rate of unemployment in America even when it falls. Europe’s labor

markets are more insulated and less flexible. That will be the next

challenge for Europe.

In Europe a few statistics show us how disparate conditions

can be even within the EMU portion of Europe. German unemployment is up

by just 0.3% points over the last 12 months. French unemployment is up

by 1.7 percentage points. Spain’s unemployment is up by 8.2 percentage

points, accounting for the bulk of the rise of the rate of unemployment

in EMU over the past year. Over the same period the US rate is up by

3.9 percentage points, and Japan’s rate is up by 1.2 percentage points.

While there are regional disparities in most large countries,

especially in the US and in Japan. But because of its single monetary

structure and split fiscal structure, regional disparities of the sort

EMU is bearing put a great deal more pressure on the system than would

be the case in a true single independent nation.

For the US, a period like this offer the economy the

opportunity to reinvent itself as old businesses are killed off and new

opportunities and needs reveal themselves. Of course, in this cycle

some old US industries were bailed out because the government thought

they were still worthwhile. Europe has had same the same experience.

Both Europe and the US will be leaving this episode of

recession with much higher levels of debt. This will be a challenge for

the period ahead. The US has showed an ability to get strong growth and

rebuild tax revenues in recoveries. Europe has not showed that same

sort of dynamism. Certain European countries, EMU members (plus the UK)

have the added burden of Maastricht criterion that quantitatively

restricts their debt levels relative to GDP. As recovery sets in, most

EMU nations will be in violation of this rule and it is not clear how

much time the authorities will allow for the rule to be put back in

force. An early imposition of the rule will lead to fiscal contraction

and could hamper recovery.

That will be an extra problems facing Europe once we turn the

corner into recovery.

| Unemployment rate and changes | ||||||

|---|---|---|---|---|---|---|

| Level | Simple Changes | |||||

| May-09 | Apr-09 | Mar-09 | 3-Mo | 6-Mo | 12-Mo | |

| EU-Urate | 8.9 | 8.7 | 8.5 | 0.6 | 1.4 | 2.1 |

| EMU-Urate | 9.5 | 9.3 | 9.0 | 0.7 | 1.5 | 2.1 |

| m/m% | % changes (ar) | |||||

| EU-U 000s | 1.8% | 2.6% | 3.2% | 7.8% | 19.8% | 31.3% |

| EMU-U 000s | 1.9% | 2.8% | 3.0% | 7.9% | 18.6% | 29.3% |

| U-Rates | Level | Simple Changes | ||||

| Germany | 7.7 | 7.7 | 7.5 | 0.3 | 0.6 | 0.3 |

| France | 9.3 | 9.1 | 9 | 0.5 | 1.1 | 1.7 |

| Spain | 18.7 | 18 | 17.3 | 2.2 | 4.7 | 8.2 |

| USA | 9.4 | 8.9 | 8.5 | 1.3 | 2.6 | 3.9 |

| Japan | 5.2 | 5 | 4.8 | 0.8 | 1.2 | 1.2 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief