Global| Oct 28 2005

Global| Oct 28 2005World Inflation Apparently No Worse in October

Summary

Inflation appears to be no worse for October than it was in September, according to very preliminary data released today and, for Germany, this past Tuesday. The overall Euro-Zone harmonized CPI (HICP) "Flash" was up 2.5% on the year [...]

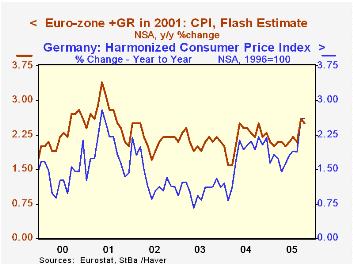

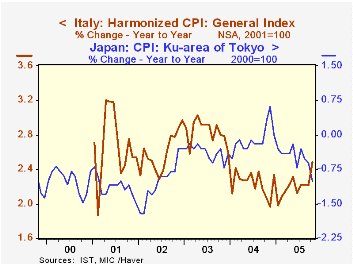

Inflation appears to be no worse for October than it was in September, according to very preliminary data released today and, for Germany, this past Tuesday. The overall Euro-Zone harmonized CPI (HICP) "Flash" was up 2.5% on the year ago, compared with 2.6% in September. An increase in the base-period amount is partly responsible for this month's downtick in the 12-month inflation rate, but even after accounting for that, prices did not accelerate in October. Among the countries available so far, Germany's 12-month inflation was stable in the two months at 2.6% and Spain's decreased to 3.5% in October from 3.8% in September. In Italy, by contrast, October's rate is 2.5%, relative to 2.2% the previous month. [All figures here reflect the HICP definition of CPI.]

Elsewhere, the Japanese sub-index for the Tokyo region fell more, 1.0%, this month than the -0.6% in September.

Little detail is available with these early reports, so it is hard to analyze the forces producing the latest reading on world inflation. Two regions provided some breakdown, Italy and Tokyo, Japan. Considering Tokyo first, where prices weakened, there was a notable advance in the base period level, establishing a bias toward a drop in year-on-year inflation. Weaker prices appeared in food, housing, apparel and recreation; they firmed for utilities -- hardly surprising -- furniture and "other". Pretty much of a mixed bag, then. The same seems to be the case in Italy. First, the base-period effect contributes to the increase in the 12-month pace, as inflation slowed in October last year. This year, the month-to-month CPI change was 0.5% in both September and October. In Italy, prices accelerated in housing, transportation and hotels and restaurants, and they fell less in health care and communications. They increased at basically a steady rate in food and "other" categories. On the other side, they slowed in apparel, recreation and culture, and education. So a mixed performance here too. There is one encouraging note that applies to both of these far-flung places: food and apparel costs remained slow. Thus, as people face a squeeze on their energy bills this winter, the budget burden from other basic necessities seems to lighten. Further, energy itself may have already started to moderate.

| Consumer Price Index: Yr/Yr % Change, NSA |

Oct 2005 | Sept 2005 | Aug 2005 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Euro-Zone "Flash" | 2.5 | 2.6 | 2.2 | 2.4 | 2.0 | 2.3 |

| Germany | 2.6 | 2.6 | 1.9 | 2.2 | 1.1 | 1.1 |

| Italy | 2.5 | 2.2 | 2.2 | 2.3 | 2.6 | 3.0 |

| Spain | 3.5 | 3.8 | 3.3 | 3.3 | 2.7 | 4.0 |

| Japan: Tokyo Area | -1.0 | -0.6 | -0.5 | 0.0 | -0.4 | -0.3 |

| Japan: Total | -- | -0.3 | -0.3 | 0.2 | -0.4 | -0.3 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief