Global| Apr 17 2017

Global| Apr 17 2017Why Trump Backed Off on Manipulator Tags

Summary

Pursuant to the 2015 Act, Treasury in its report has found that no major trading partner met all three criteria for the current reporting period to be named a currency manipulator. Treasury also concludes that no major trading partner [...]

Pursuant to the 2015 Act, Treasury in its report has found that no major trading partner met all three criteria for the current reporting period to be named a currency manipulator. Treasury also concludes that no major trading partner of the United States met the standards identified in Section 3004 of the Omnibus Trade and Competitiveness Act of 1988 for currency manipulation in the second half of 2016.

Pursuant to the 2015 Act, Treasury in its report has found that no major trading partner met all three criteria for the current reporting period to be named a currency manipulator. Treasury also concludes that no major trading partner of the United States met the standards identified in Section 3004 of the Omnibus Trade and Competitiveness Act of 1988 for currency manipulation in the second half of 2016.

The conditions for currency manipulation to be ascertained are that, a country needs to have: (1) a significant bilateral trade surplus with the United States is one that is at least $20 billion; (2) a material current account surplus, one that is at least 3 percent of GDP; and (3) persistent, one-sided intervention, that occurs when net purchases of foreign currency are conducted repeatedly and total at least 2 percent of an economy's GDP over a 12 month period. The Treasury also adds this note to the above criteria as follows... 'In assessing the persistence of intervention, Treasury will consider an economy that is judged to have purchased foreign exchange on net for 8 of the 12 months to have met the threshold. These quantitative thresholds for the scale and persistence of intervention are considered sufficient on their own to meet the criterion. Other patterns of intervention, with lesser amounts or less frequent interventions, might also meet the criterion' depending on the circumstances of the intervention.

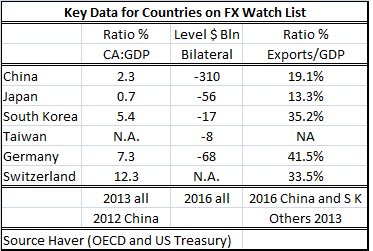

There is still a monitoring list of countries whose actions are being closely watched although they have not been found to be manipulators in this report. They are China, Japan, South Korea, Taiwan, Germany, and Switzerland. Some of their key data are presented in a table below.

Most of these countries failed the manipulation accusation on the absence of substantial action in the foreign exchange market. But in the case of China and Japan, recent surpluses have come down substantially. In the wake of Japan's Tsunami, it shut down is nuclear power plants and its fuel imports shot up substantially, wiping out its surplus. China has slowed and so have its exports. Not only is it retooling for more balance growth (or so it says...), but it has a new problem. It has been intervening aggressively to prop the yuan up, not to drive it down! This turnabout result has come as domestic conditions in China have become more difficult in the wake of the financial crisis. China is now an economy substantially addicted to debt and at a time that debt less effectively is propping up growth. And China has a major pollution problem, a coming demographic imbalance and other issues. As a result and not for currency parity reasons funds have been flowing -spilling, surging- out of China as people have sought to put wealth outside the country. Germany, of course, has a huge current account surplus that is not getting any better and it is part of the EMU arrangement putting it in a very different situation when it comes to assessing currency parity and what role German officials might be responsible for. Germany has simply reserved a place for itself in the EMU in which it has a locked in competitiveness and a trade advantage that is insulated from currency market reactions.

The German and South Korean economies are particularly dependent on exports. Germany has an export-to-GDP ratio of over 40%. Clearly the German are going to be sensitive to anything that affects trade. They have been among the most vocal to show displeasure with the U.S. stance to reassess free trade and they were also among some of the least aggressive voices against the U.K. when it voted to adopt its Brexit strategy. To be highly dependent on trade is to be highly vulnerable to international conditions and the way those winds might blow.

Germany is in a situation in which its domestic fiscal house is so orderly it pretty much stands alone on its merits, but it is achieving growth on the back of domestic demand generated elsewhere. At a time when Germany is a vocal proponent of the Maastricht criteria and enforcing European deficit and debt levels, it is adding very little to European demand and taking a lot off the table for itself. Even though exports to GDP are not part of the U.S. treasury criteria that ratio exposes some of these countries for being less than 'good neighbors.' Trade, after all, is supposed to be mutually beneficial. A country that runs high surpluses and gets an outsized proportion of its growth from satisfying overseas demand is not playing the trade game very fairly.

The U.S. Treasury had adopted this framework of rules before Mr. Trump came to office. It is clear that the treasury recognizes that it will take on pariah status globally if the U.S. attacks countries for being currency manipulators without good cause. So this set of guidelines was drawn up to provide a framework, a backbone, a justification, for action. The problem still exists, however, for countries that are more subtly abusing trade rules. Huge persistent trade surpluses per se should be reason enough to brand a country as an unfair trader if not a currency manipulator except under very unusual circumstances. Exchange rates are supposed to adjust to re-balance current accounts. When they do not, the currency system is not doing its job and something is wrong.

Mr. Trump is playing his new more aggressive and very serious game on a world stage. He has opted to not call China a currency manipulator because of some very recent changes in China's trade and foreign exchange market practices and because he wants help on North Korea. Clearly Trump is a geopolitical player that will bide no Japanese lunch-box strategy in which everything stays in its own walled-off section as in a bento box. He is quite willing to horse trade over commercial policy to obtain a geopolitical result that is dear to him. When Trump said he would run U.S. policy for American interests, I think a view of isolationism crept into a lot of minds. It may well be that Mr. Trump has a much broader view of U.S. welfare and of its place in the world than anyone suspected before electing him. It is also too soon to tell what he really wants be... He is willing to thumb his nose at political opinion and acts as though he does not care if he is elected for a second term of office. However, he seems to realize that he can't remain an outsider if he wants beltway clout which he will need to get his policies through. And he does care about that. Mr. Trump is becoming a much more fascinating person the longer he is in office. He is putting some of his early snafus behind him. He is willing to modify his campaign promises and interestingly he changes his mind but publically rationalizes why. While there are things about his presidency that are downright outrageously different, there are also ways in which it is falling into a more conventional line. As is always the case with Mr. Trump, people see what they want to see and ignore what they don't want to see. He is a complex person and a polarizing one, but he is becoming more interesting than 'that guy' who ran for office.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief