Global| Oct 21 2016

Global| Oct 21 2016What's Goin' On? The PPP PPPardox

Summary

Why do things continue to go off-track in the global economy? It is very simple to understand really and one of the main reasons is embodied in the chart and the table. First, let me describe what you are looking at. The chart shows [...]

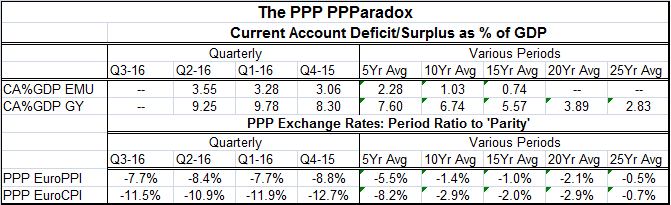

Why do things continue to go off-track in the global economy? It is very simple to understand really and one of the main reasons is embodied in the chart and the table. First, let me describe what you are looking at. The chart shows that since 2000 the EMU and German current accounts as a ratio to their respective GDPs have swung from deficit to surplus and the surpluses have continued to get larger year by year. The table documents that for Germany on a longer smoothed (5-year increment) basis the move to greater surpluses is even longer.

Why do things continue to go off-track in the global economy? It is very simple to understand really and one of the main reasons is embodied in the chart and the table. First, let me describe what you are looking at. The chart shows that since 2000 the EMU and German current accounts as a ratio to their respective GDPs have swung from deficit to surplus and the surpluses have continued to get larger year by year. The table documents that for Germany on a longer smoothed (5-year increment) basis the move to greater surpluses is even longer.

The table also depicts the exchange rate value calculated relative to its parity condition. Now parity is hard to know. For this table, I have used a simple well-worn device. The notion is that if exchange markets are reasonably efficient they should get the exchange rate right over the long haul. So while exchange rates will oscillate, the trade weighted real (price level adjusted) exchange rate between a region like the EMU and its various trade partners should over time be a good estimator of actual parity. That in simpler language means that the average of the real broad exchange rate over a long period of time should be a good estimator of the currency's true parity position (JP Morgan makes these calculations and they are available in the database). So using that parity calculation, I also calculate the ratio of the real broad exchange rate for various periods to its long-term average and present that as a percentage deviation in the table. This is done using both PPI prices and then again using CPI prices. What we find is that the exchange rate for the EMU has been consistently and nearly monotonically getting weaker and weaker relative to parity.

Here is what the EMU exchange rate plot looks like for the real effective exchange rate, presented as a time series.

Here is what the EMU exchange rate plot looks like for the real effective exchange rate, presented as a time series.

What we see with the EMU are two coincident disturbing trends. In isolation either one might be disturbing, but together they are very unnerving. This is that the current account surplus relative to GDP is rising and that the exchange rate is moving in a direction to keep that happening rather than to restore equilibrium and dissipate the surplus.

For trade to work, it must be an operable system and everyone must benefit from it. You hear people talk about 'free trade' and 'comparative advantage.' Those refer to certain conditions. Free trade is an approach which to exist and to spread its benefits must also have its underlying principles being carried out. One of them is that exchange rates will be market-determined. And it is widely believed that market-determined exchange rates will act to offset current account imbalances when they arise- not exacerbate them. We see in the EMU and in Asian countries with very sticky current account surplus conditions that currencies do not move to restore their trade accounts (current accounts) to balance. The balancing 'item' in international trade is the U.S. current account which is desperately in deficit with a deficit relative to GDP having grown steadily since exchange rates were set to fluctuate in the early 1970s. The U.S. runs the never ending deficits that make never ending surpluses abroad possible. But that does not make it right or good. In fact, it is unsustainable and taking a toll on the U.S. economy, perceptions of economic fairness, politics and a lot of other American 'institutions.'

These 'never ending' events undermine the operation of the international trade and financial system. They have brought it to its knees and yet there is no movement to fix it. It's a bit like having a car with evidence of a clear mechanical problem but, since it still runs, you dive it to work every day because, well, you have to get to work. So you will drive it until it breaks down then maybe do some hasty repair to get it back in service and never take the time to fix it properly.

One problem with running these never ending imbalances is that the euro, the yuan and other currencies, in order to stay too weak, force something else (the dollar!) to be too strong. A too-strong dollar undermines the ability of producers in the U.S. to make goods even for domestic consumption and export anything. It makes imports cheap. It causes a never ending U.S. current account deficit that leaches wealth from the U.S. economy. It undercuts job creation in the U.S. and at the same time stuffs capital into the country since the current account deficit must be financed. Countries wind up buying dollars because they must to support their chosen 'currency peg.' Yet, in the U.S., there is nothing to invest in the private sector, since firms in the U.S. are no longer competitive because the dollar is too strong. This creates a huge paradox. And it is not surprising that with so much surplus capital in the U.S. it gets put to mischief. Since the U.S. cannot compete in the global environment and can't create enough jobs, consumption is kept alive by debt accumulation and government spending or support programs. But it does not take a rocket scientist to see that this is unsustainable. There is a reason that only 47% of those who file Federal tax returns pay any federal income tax. This will be system rife with problems since it is built on a very poor foundation and on flows that cannot be sustained.

China and other developing economies want to export to the U.S. because exporting one of the easiest ways to stoke growth. It is much harder to grow fast by developing your domestic economy and all the internal balance that is required. Since you must get wages and income and debt and exchange rates and prices and monetary policy right and have a functioning financial sector, the demands of balanced domestic growth are just too great for it to happen too fast. For export-led growth, you merely need a factory, some capital, cheap labor, a controlled exchange rate and (bang!) send goods off to the USA and count your profits. Of course, you will reinvest them mostly in dollars to keep the exchange rate weak and the export machine going. But that is far easier than balancing all the things that must be balanced to get sustainable domestic growth. In a command economy like China, it is highly unlikely that those in charge would pick all the right sustainable actions. Capitalism works because it is decentralized and is responsive to market signals.

To get the global economy back on track, we need to free up exchange rates - everywhere. Of course, it is not happening. There is a great deal of opposition to it: Some from our trade partners with sweet deals, some from multinational corporations with skin in the game. Some of it manifests itself as opposition to more 'free trade' deals at the grass roots level. Well, knocking down trade barriers will not help the U.S. if trade is going to occur at disadvantaged exchange rates.

We have been avoiding this-avoiding some of the necessary steps of minding the details- because they are too hard. The EMU is another example of modern economic engineering based on corner cutting. It was formed in this way and now it is big trouble. Its early issue was: how do you bond countries in one block under one currency when countries have such different inflation rates? But they did it. Then they forgot about that problem, but that did not make it go away. And now that has been the undoing of the EMU and is the cause of all the austerity programs to try to put the toothpaste back in the tube.

The Germans have created one sweet deal in which the deutsche mark is embedded in this euro and the euro block is weak so the implicit deutsche mark is getting weaker enhancing German competitiveness day by day as the German trade surplus grows. Trade has become mercantilistic. It has become exploitative. The key pillar for expanding trade - for free trade- is that it is mutually beneficial. That is no longer true. Trade has become a ticking time bomb. We need to fix the exchange rate mechanism because of all the distortions that are going on because of it. That's what's going on: distortion. And this system won't continue to go in like this forever without blowing up- again and next time the explosion might even be worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief