Global| Jan 10 2014

Global| Jan 10 2014Volatility Aside EMU IP Is Recovering

Summary

A number of European countries now have reported industrial production in the outturn appears to show relatively widespread improvement. If we look at the 12-month gains of the eight EMU members in the table and the three non-members, [...]

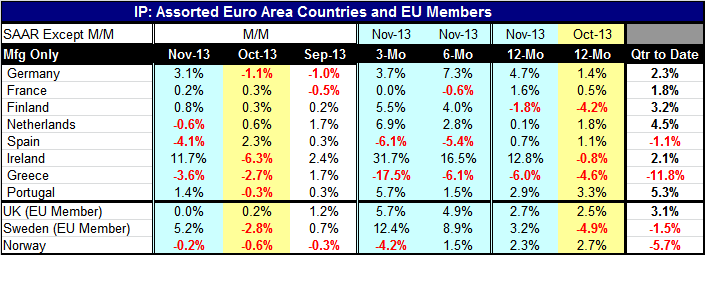

A number of European countries now have reported industrial production in the outturn appears to show relatively widespread improvement. If we look at the 12-month gains of the eight EMU members in the table and the three non-members, the table only shows year-over-year declines in industrial output in two countries. Those two countries are Greece and Finland. There were four countries with year-over-year declines in October.

A number of European countries now have reported industrial production in the outturn appears to show relatively widespread improvement. If we look at the 12-month gains of the eight EMU members in the table and the three non-members, the table only shows year-over-year declines in industrial output in two countries. Those two countries are Greece and Finland. There were four countries with year-over-year declines in October.

In November there were output declines of 0.6% in the Netherlands, of 3.6% in Greece and of 4.1% in Spain. Of these month-to-month declines, only Greece has back-to-back declines in industrial production. Greece also has net declines over three-months, over six-months and over 12-months. And the extent of the Greek output declines is getting more severe over the recent period. Greece is the one country in the Monetary Union that still seems to be backsliding. Finland also has a year-over-year decline, but it also shows industrial production increasing in a 5.5% annual rate over three months and at a 4% rate over six months.

If we look at this entire sample of 11 countries, both EMU and non-EMU members, we find preponderant evidence of increases in industrial production. Over three-months only three countries showed declines, over six-months only three countries showed declines and over 12-months only two countries showed declines. This is simple, but relatively powerful evidence.

In the quarter-to-date, a very short-term measurement that is very sensitive to the timing of the calculation, we see that 4 of the 11 countries still have output declines. They are Spain, Greece, Sweden and Norway. The Netherlands, in this period, even with an output decline in November, shows the second strongest quarter-to-date annual rate gain 4.5% exceeded only by Portugal that is gaining at a 5.3% pace. France, a country that has been struggling, has the smallest gain among those with gains in the quarter-to-date, at a 1.8% pace.

Since Europe is trying to recover from recession, finding that most of the member IP growth rates are positive is a significant finding. It helps to establish that growth is now in train. And, six of the countries with positive growth also show that growth is accelerating over three-months. Ireland leads the pack with three-month growth and a 31.7% annual rate followed by Sweden with industrial production growth in a 12.4% annual rate in the Netherlands and a 6.9% annual rate.

However, the factory sector has been the strongest sector for some time. The service sector is still lagging. The service sector is the job creating sector. We have already seen the US post some good PMI data for manufacturing and for services then come up with a disappointing employment reading as its service sector is lagging. The goods sector seems to be the first thing that the global economy is putting back to normal. But even as the global economy is mending the goods sector, the services sector is not healing very fast. This is going to be the key portion of the economy to mend since it is the job sector. The factory sector is on the road to recovery but that is not enough.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.