Global| Oct 17 2014

Global| Oct 17 2014Vehicle Registrations Continue Annual Gains But....

Summary

European auto registrations continue their year-over-year gains in September, rising by 2.6% year-over-year. But this growth rate is slipping, falling from a year-over-year gain of 3.7% last month and of 4.6% the month before. Vehicle [...]

European auto registrations continue their year-over-year gains in September, rising by 2.6% year-over-year. But this growth rate is slipping, falling from a year-over-year gain of 3.7% last month and of 4.6% the month before.

European auto registrations continue their year-over-year gains in September, rising by 2.6% year-over-year. But this growth rate is slipping, falling from a year-over-year gain of 3.7% last month and of 4.6% the month before.

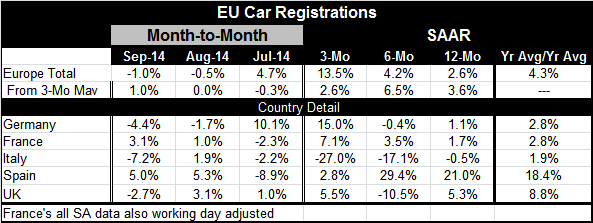

Vehicle registrations have fallen in each of the last two months as well, dropping by 1% in September and by 0.5% in August. Trends in vehicle registrations are little bit difficult to pin down because the series is so volatile. In the table, we show country level data and you can see how extraordinarily volatile those figures are.

Even with the pace of registrations from three months to six months and 12 months, growth rates still see a great deal of volatility at the country level. Some of this is because governments have instituted programs to spur auto sales from time to time and while those programs work, they don't last; and when they're taken off, the auto sales that were overstimulated then plunge. We have to be careful to always acknowledge that there are sometimes artificial elements to the pickup and to the letdown of auto sales and therefore to the registration data.

On the chart, we plot the levels of registrations to try to get around some of the difficulties in presenting growth rates of registrations. What that chart shows is that registrations are much lower than they were before the recession and financial crisis. The chart also shows that while sales are on a rebound, that rebound is beginning to slow compared to its pace earlier on. You can see the slowing on the chart, as you note that the upward gradient begins to flatten out in recent months; in addition to that, you see a little bit more volatility setting into the auto registrations series.

Auto sales and registrations are important because they represent a big consumer purchase. The industry is important, and auto sales serve a very good benchmark of consumer confidence and consumer capability in terms of the consumer's ability to spend. In that respect, the auto sales figures are still encouraging for Europe. But we have to be mindful that sales are showing this evidence of slowing growth and that also seems to be a reality.

If we look at the year-over-year growth statistics for Germany, France, Italy, the U.K. and Spain from October 2013 to May of 2014, we have five countries in a period of eight months. That gives us 40 observations of year-over-year registrations. Over that span, there were only five instances of year-over-year declines in auto sales and three of those were from Italy at the beginning of this period. If we take those same five countries over the last four months, we have 16 observations - not 40- and already four instances of year-over-year growth in registrations turning negative (one-quarter of the time).

Year-over-year momentum still shows that vehicle registrations in Europe are advancing. However, as we look closely at the timeline and put the country level data their proper perspective, it is also evident that registrations are slowing. The auto industry in Europe is still under pressure and there is much more capacity than the industry currently needs to serve and yet no one in the industry has taken steps to eliminate excess capacity. However, as the pace of registrations slows, automakers in Europe will be put under increasing pressures. Despite the year-over-year gains in September, the sector seems to be headed for harder times ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief