Global| Feb 14 2014

Global| Feb 14 2014Valentine's Day Gift from EMU

Summary

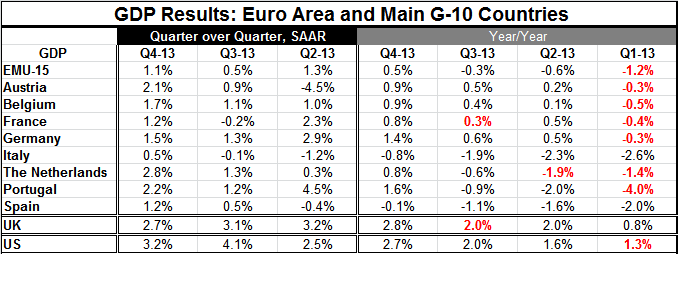

Acceleration, but very gradual acceleration, is the clear picture from the table and the chart on GDP growth. EMU GDP growth is 0.5% year over year in Q4 2013, up from -0.3% in Q3, -0.6% in Q2 and -1.2% in Q1. That is steady but also [...]

Acceleration, but very gradual acceleration, is the clear picture from the table and the chart on GDP growth. EMU GDP growth is 0.5% year over year in Q4 2013, up from -0.3% in Q3, -0.6% in Q2 and -1.2% in Q1. That is steady but also slow progress.

Acceleration, but very gradual acceleration, is the clear picture from the table and the chart on GDP growth. EMU GDP growth is 0.5% year over year in Q4 2013, up from -0.3% in Q3, -0.6% in Q2 and -1.2% in Q1. That is steady but also slow progress.

At this point I would caution about excessive optimism. This is not a recovery like any we have seen in the past. The US experience with its ongoing `recovery' is an example.

Let's remember that we refer to three economic stages: (1) expansion, (2) recession, (3) recovery, then repeat. Recovery is a special part of the growth phase, in which, after being mired in recession and that fact having created a great deal of economic slack, the economy then grows, for a time, at pace in excess of its long-term growth rate. In this phase the economy `recovers' as its high growth rate puts it back up closer to the path that it would have been on had there been no recession. During this period of unsustainably strong growth, resource utilization moves back up toward full employment, for labor, for capital, for all inputs.

One problem though in this cycle, after recession, we have not yet had such a period, even in the US that has done much better than Europe. In the US, the unemployment rate is falling on still lackluster growth and on a thick soup of discouraged workers and demographics. These same demographic trends are at work in Europe.

Nonetheless Europe is taking a turn for the better. But its turn is on four wheels, not on two. As we have seen in more recent monthly data, the engine is still coughing not simply accelerating smoothly. German industrial data have begun to backtrack. Moreover, Germany is being assailed for having what is now the biggest current account surplus in the world. It is gathering pace by being a bad global citizen and scarfing up all the demand for itself. Its recent industrial production report and a broader one for all of EMU showed that consumer goods output is not in gear in either Germany or in the euro area. More to the point: consumption is not heating up. German growth has been the kind that makes growth elsewhere weaker. That is not good. It's not a locomotive; it's a steamroller.

The table highlights changes in year-over year growth rates presented quarter by quarter back to Q1 2013. In Q1 2013 of the nine EMU member counties in the table, seven had showed deteriorating year-over-year growth compared to Q4 2014. Only Spain and Italy were `improving' and they still had negative year-over-year growth rates. By Q3 2013, all but one country was improving its year-over-year pace compared to the previous quarter. That trend continued in Q3 2013. By Q4 2013 all countries showed improvement. Even so, Italy and Spain are doing so with still-negative year-over-year rates of growth. The margin of US GDP growth above that of EMU is declining. EMU is making progress, but its progress is slow and things in Europe are not being fixed from `the ground up.'

Under the surface, Europe still has many issues to deal with. The European Central Bank is still the euro area's only real unifying force. There is some policy harmonization and free trade, but those are not the same institutional glues as a common fiscal effort. While there is a bailout plan in event of great need, fiscal policies are still separate making Europe like a big Japanese lunch box. Fiscal rules try to force fiscal policies down a common path but individual country needs and circumstances vary greatly.

In the UK, not a single currency participant, Scotland is going to have a vote later this year to see if it wants to leave that long-standing union in place.

Europe is still in flux. Its members are still arguing about what they want to be `when they grow up.' That means that a recovery as fragile as this one is still to be viewed somewhat skeptically even as the ECB tries to strengthen the glue that binds.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief