Global| Oct 16 2008

Global| Oct 16 2008US IP Plunges in September and Plummets in the Quarter

Summary

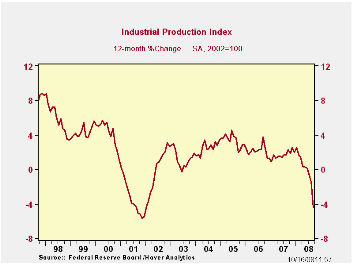

US industrial output, an index of real output, is off by 2.8% in September but the drop is exaggerated by the impact of two hurricanes and a job action at aircraft manufacturer Boeing. The Federal Reserve Board reported that the [...]

US industrial output, an index of real output, is off by 2.8%

in September but the drop is exaggerated by the impact of two

hurricanes and a job action at aircraft manufacturer Boeing. The

Federal Reserve Board reported that the disruptions from the hurricanes

contributed about 2.25 percentage points to the decline while the

Boeing strike contributed 0.5 percentage point.

The drop is beginning to look like the drops IP made in the

last recession. Declines in output are widespread in September.

For the quarter which is now complete based on preliminary

data the drop in output is at a rate of -6%, a substantial pace of

decline for a quarter (saar). Consumer goods output is down at a -6%

pace with consumer goods ex-auto output down at a pace of -8.2% and

consumer energy off at a -12.6% pace. In this framework auto output

rose in September but fell in the quarter at a pace of -5%. The

consumer vehicle sector is not what is leading us lower.

The business sector is leading us lower. The business sector

saw a sharper decline with business equipment output off by -8.4% saar

led by a whopping decline of -41% (saar) for transportation. Materials

output was off at a pace of -6%.

The weakness in the industrial sector clearly is widespread.

The slowing in US exports will hit the sector hard. Manufacturing has

been shedding jobs but at a slower pace than it has in most recessions.

It looks like the pace of job losses in MFG is about to pick up. That

in turn that will send waves of repercussions throughout the economy as

a vicious circle of job cuts is likely to ensue since workers that lose

jobs also are consumers that lose income. As that happens spending

drops and that leads to more job cuts. It is vicious circle time: Not

Miller time.

| Industrial Production | |||||||

|---|---|---|---|---|---|---|---|

| Monthly Pct. Changes | At Annual Rates of Change | SAAR | |||||

| Month-to-month Pct. Change | 3-Month | 6-Month | Year/Year | 08-Q3 | |||

| Industrial Output | Sep-08 | Aug-08 | Jul-08 | %Change | %Change | %Change | Pct Change |

| All Prod&Materials | -2.8% | -0.9% | -0.1% | -15.1% | -8.4% | -4.5% | -6.0% |

| All Products | -2.3% | -1.1% | -0.2% | -14.1% | -7.9% | -4.9% | -5.9% |

| Final Products | -2.5% | -1.2% | -0.2% | -15.6% | -8.5% | -4.9% | -5.8% |

| Manufacturing only | |||||||

| MFG - NAICS | -2.7% | -1.0% | 0.0% | -14.4% | -8.6% | -4.8% | -5.8% |

| MFG-Durables | -2.4% | -1.5% | 0.3% | -14.2% | -9.2% | -4.6% | -4.8% |

| MFG-Nondurables | -2.9% | -0.4% | -0.4% | -14.4% | -7.9% | -4.9% | -7.0% |

| Consumer Goods | -1.3% | -1.7% | -0.3% | -13.1% | -6.9% | -5.0% | -6.0% |

| Durables | -0.7% | -6.2% | 1.1% | -23.1% | -13.1% | -11.7% | -6.7% |

| Automotive Prod. | 1.7% | -10.9% | 1.9% | -30.6% | -17.3% | -15.2% | -5.0% |

| Ex. Automotive Prod. | -2.7% | -1.7% | 0.4% | -15.9% | -9.0% | -8.1% | -8.2% |

| Nondurables | -1.6% | -0.6% | -0.5% | -10.6% | -5.5% | -3.1% | -5.7% |

| NonEnergy | -0.4% | 0.0% | -0.5% | -3.7% | -2.4% | -1.7% | -2.5% |

| Cons Energy | -4.4% | -1.6% | -0.5% | -25.8% | -12.2% | -5.9% | -12.6% |

| Business Equip. | -7.0% | -0.2% | 0.0% | -28.7% | -16.5% | -7.0% | -8.4% |

| Transportation | -33.6% | -4.5% | 0.2% | -145.6% | -72.9% | -38.2% | -41.0% |

| Computer & Office Eqpt | 0.9% | 0.6% | 0.1% | 6.4% | 6.7% | 15.6% | 4.2% |

| Ex. Tech.& T-port | -9.2% | 0.4% | -0.3% | -36.6% | -21.7% | -10.4% | -11.5% |

| Materials | -3.4% | -0.8% | 0.2% | -16.0% | -9.0% | -3.8% | -6.0% |

| Durables | -1.0% | -1.0% | 0.2% | -7.6% | -5.2% | -1.8% | -3.3% |

| Nondurables excl Energy | -3.3% | -0.3% | -0.6% | -16.6% | -9.4% | -6.6% | -7.8% |

| Energy | -6.2% | -0.9% | 0.8% | -25.0% | -13.2% | -4.1% | -7.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief