Global| Mar 30 2005

Global| Mar 30 2005US GDP Growth Unrevised, Corporate Profits Firm

by:Tom Moeller

|in:Economy in Brief

Summary

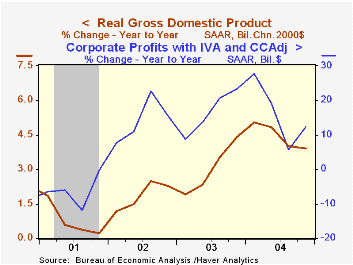

US real GDP growth in 4Q04 was unrevised at 3.8% (AR). The Consensus expectation had been for a slight upward revision to 4.0% growth. Reported for the first time, total U.S. operating corporate profits surged 13.5% (12.4% y/y) and [...]

US real GDP growth in 4Q04 was unrevised at 3.8% (AR). The Consensus expectation had been for a slight upward revision to 4.0% growth.

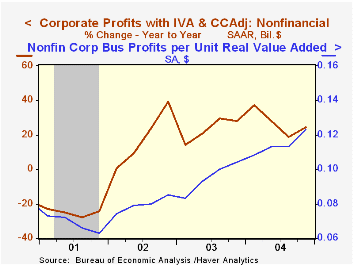

Reported for the first time, total U.S. operating corporate profits surged 13.5% (12.4% y/y) and the gain was held back by no change in profits earned abroad. Domestic profits grew 16.2% (18.3% y/y) and reflected a 30.1% rebound in financial sector profits which were depressed by hurricanes in 3Q.

Profits earned in the nonfinancial corporate sector grew 10.3% (24.2% y/y), the strongest gain since 2Q03 and were aided by continued profit margin expansion. Labor costs per unit of output fell for the first time in over a year as productivity remained strong. Non-labor costs continued the decline in place for nearly three years. Pricing power improved and real gross value added (output) grew a strong 1.6% (5.3% y/y).

Domestic demand growth was unrevised at 4.5% as growth in business fixed investment in equipment & software held firm at 18.4% (14.5% y/y). Consumer spending growth also held solid at 4.2% (3.8% y/y). Less computers real GDP grew 3.3% (3.8% y/y).

Price inflation was revised up slightly to 2.3%. The price index for domestic demand was revised higher to 2.9% (2.9% y/y) and continued to reflect a strong 5.3% (4.8% y/y) rise at the state & local government level.

Perspectives on Monetary Policy and Central Banking from New York Federal Reserve Bank President Timothy F. Geithner can be found here.

| Chained 2000$, % AR | 4Q '04 (Final) | 4Q '04 (Prelim. | 3Q '04 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| GDP | 3.8% | 3.8% | 4.0% | 3.9% | 4.4% | 3.0% | 1.9% |

| Inventory Effect | 0.5% | 0.6% | -1.0% | 0.3% | 0.4% | -0.1% | 0.4% |

| Final Sales | 3.4% | 3.2% | 5.0% | 3.6% | 4.0% | 3.1% | 1.4% |

| Trade Effect | -1.4% | -1.4% | -0.1% | -0.6% | -0.4% | -0.3% | -0.7% |

| Domestic Final Demand | 4.5% | 4.5% | 4.9% | 4.2% | 4.4% | 3.4% | 2.1% |

| Chained GDP Price Index | 2.3% | 2.1% | 1.4% | 2.4% | 2.2% | 1.8% | 1.7% |

by Tom Moeller March 30, 2005

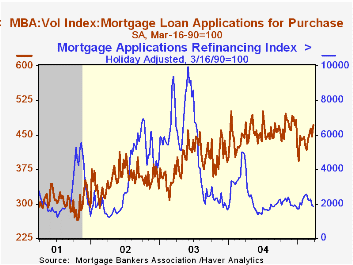

The Mortgage Bankers Association reported that mortgage applications recovered 2.4% last week following the 9.4% drop during the prior period. The average level in March 4.8% below February.

Purchase applications rose 5.5% to the highest level of the year. Purchase applications in March are 6.2% higher than in February.

Applications to refinance added 2.0% to the 16.5% decline the prior week. The decline pulled the March average down 16.1% versus February.

The effective interest rate on a conventional 30-year mortgage rose further to 6.34% from 6.19% the prior week and from 5.85% averaged in February. The effective rate on a 15-year mortgage also rose to 5.96%.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

| MBA Mortgage Applications (3/16/90=100) | 03/25/05 | 03/18/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total Market Index | 674.3 | 658.8 | -38.2% | 735.1 | 1,067.9 | 799.7 |

| Purchase | 470.9 | 446.4 | 6.1% | 454.5 | 395.1 | 354.7 |

| Refinancing | 1,857.2 | 1,894.2 | -61.8% | 2,366.8 | 4,981.8 | 3,388.0 |

by Carol Stone March 30, 2005

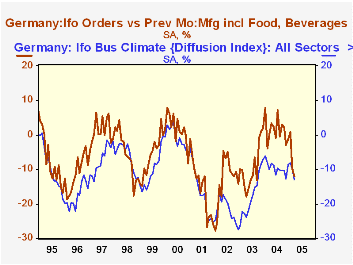

Back at the turn of the year, business prospects were looking up in Germany. December and January saw an improvement in the Ifo Business Climate Index to the highest values in almost a year; this was reflected in production, the assessment of demand and orders. However, February and March have reversed this encouraging pattern, with some gauges falling rather precipitously.

The Business Climate Index has slumped 2.4 points in the two months to 94.0 (2000=100), with the corresponding diffusion index retreating to -12.9% from -8.1% in January. The "business situation", the measure of current conditions, fell to -18.2%, a 5-percentage-pointing deterioration since December. Expectations also decreased, reaching down to -7.4% in March from -1.5% in January. Orders are a source of the worsening outlook, led by the domestic sector.

Most industry groups have participated in the renewed downturn. Among better readings, food processing increased to -6.2% from -7.0%; construction rose 3 percentage points, but, at -39.8%, this move can hardly be seen as an indication of better health in that sector. Other basic industries saw relative deteriorations: March values were generally less positive or more negative.

We can guess that rising energy prices have contributed to the erosion in business conditions; producer prices for energy were up 8.2% in the year to February, compared with a drop of 0.7% in the comparable year-ago period. Total producer prices rose 4.2% from February 2004; they had been basically unchanged in the 12-months ended in February 2004. The euro, after a pause last spring and summer, has been rising again. By contrast, other exogenous forces seem fairly supportive: German stock prices are firm or rising, some quite notably; interest rates are low. Perhaps, with this financial backstop, the current downtick in the Ifo survey will turn out to be short-lived or at least quite moderate.

| Germany: Ifo Survey | Mar 2005 | Feb 2005 | Jan 2005 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Business Climate Index, 2000=100 | 94.0 | 95.4 | 96.4 | 95.7 | 91.7 | 89.4 |

| % Balance | -12.9 | -10.0 | -8.1 | -9.6 | -17.5 | -22.0 |

| Business Situation | -18.2 | -16.0 | -14.4 | -16.9 | -27.9 | -33.9 |

| Business Expectations | -7.4 | -3.9 | -1.5 | -1.8 | -6.5 | -9.0 |

| Orders on Hand, Manufacturing | -20.8 | -19.0 | -13.4 | -21.1 | -33.2 | -35.2 |

| Foreign Orders on Hand, Manufacturing | -13.5 | -10.1 | -11.2 | -16.2 | -28.2 | -26.8 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief