Global| Apr 30 2007

Global| Apr 30 2007US Consumer Spending Flounders in March but Trend Still Mostly Firm

Summary

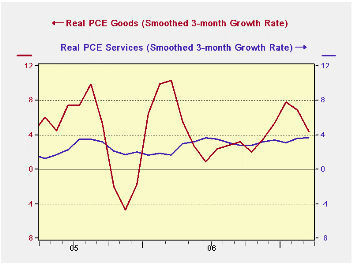

The trend to spend took a hit in March but the quarter was still strong for the consumer, as we already say in the GDP report. Three-month trends show us that spending is cooling to a 2.2% pace led by a slowdown in nondurable goods [...]

The trend to spend took a hit in March but the quarter was still strong for the consumer, as we already say in the GDP report. Three-month trends show us that spending is cooling to a 2.2% pace led by a slowdown in nondurable goods where spending dropped to a -0.6% rate of growth. Spending on durable goods still rose a robust 3.5%. Services spending continued its mild acceleration with a three-month rate of growth of 3.3%. Consumer real disposable personal income backed off in the month to a pace of 2.6% (SAAR) compared to a year/year pace of 4.1% and a three- month growth rate that is still at 3.8%.

On balance, these trends are still good and we know that monthly income and spending are subject to some volatility. So monthly declines should be taken in that spirit.

The savings rate continues negative but the rate of decline in the saving rate has switched and although the rate itself is still negative, the savings rate is headed back toward zero and perhaps into positive territory. This trend may reflect less equity extraction on the part of consumers whose houses are losing value but there is no evidence that it is affecting the pace of spending.

If we adjusted the various income components for inflation, we see steady acceleration in all these groups except for nonfarm proprietors. Real income generation trends are on solid footing and that should underpin spending as we move ahead. This trend is more important to consumer spending trends that home values.

Spending trends for goods and service are still solid. Goods spending is decelerating after a very strong increase and while services spending has been more modest it is still mildly accelerating.

With the flat core PCE deflator this month, inflation is starting to return to the Fed’s comfort zone.

| Percentage Changes At Annualized Rates: Various Horizons | |||||

| Inflation-adjusted | 1-Mo | 3-Mos | 6-Mos | 1 Year | Q1/Q4 |

| Consumption | -2.3% | 2.2% | 3.7% | 3.1% | 3.1% |

| Goods | -0.5% | 0.8% | 4.5% | 3.3% | 1.7% |

| Durable Goods | 1.4% | 3.5% | 5.5% | 4.0% | 3.2% |

| Nondurable Goods | -1.4% | -0.6% | 4.0% | 3.0% | 1.0% |

| Services | -3.4% | 3.3% | 3.2% | 3.0% | 4.1% |

| Consumer Income | |||||

| Real DPI | 2.6% | 4.6% | 4.1% | 2.9% | 4.1% |

| Per Capita | 1.8% | 3.8% | 3.2% | 1.9% | -- |

| Memo: | Mar 2007 | 3-Mos | 6-Mos | 1 Year | -- |

| Savings Rate (Pct) | -0.8 | -1.0 | -1.1 | -1.3 | -- |

| Annual Rates Of Growth | |||

| 3-mos | 6-mos | 12-mos | |

| Personal Income | 7.7% | 5.4% | 3.5% |

| Wages and Salaries | 7.2% | 5.9% | 2.4% |

| Proprietors' Income | 0.5% | 4.1% | 3.1% |

| Non Farm (prop) | -3.4% | 0.2% | 1.5% |

| Rental Income | 28.4% | 21.8% | 9.3% |

| Dividend Income | 11.4% | 10.2% | 11.0% |

| Interest Income | 11.5% | 11.9% | 1.2% |

| Transfer payments | 7.9% | 11.5% | 7.2% |

| Social Insurance Payments | 4.6% | 10.1% | 7.3% |

| Total Non-farm Income | 6.1% | 7.7% | 5.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief