Global| Jan 30 2008

Global| Jan 30 2008US 4Q GDP Weaker Than Expected At 0.6%. Exports & Inventories Added Less

by:Tom Moeller

|in:Economy in Brief

Summary

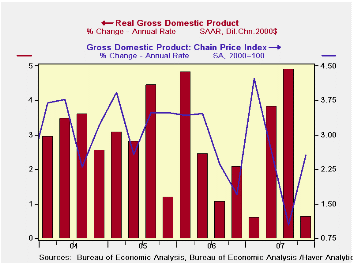

U.S. real GDP in the last quarter of 2007 rose at a 0.6% annual rate. The figure from the Commerce Department contrasted slightly with the Consensus expectation for a 1.2% advance. The figure contrasted sharply, however, with an [...]

U.S. real GDP in the last quarter of 2007 rose at a 0.6% annual rate. The figure from the Commerce Department contrasted slightly with the Consensus expectation for a 1.2% advance. The figure contrasted sharply, however, with an average rate of growth during the prior two quarters of 4.4%.

Each of the economy's sectors including domestic demand, foreign trade and inventories contributed to the slowdown. Inventories subtracted 1.3 percentage points from 4Q GDP growth as a rate of accumulation turned negative. That contrasted with an average 0.6 percentage point addition during 2Q & 3Q. An improved foreign trade account added much less to real GDP growth last quarter. The 0.4 point addition was down from an average 1.4 percentage point contribution during the prior two quarters. Growth in exports slowed to a still quite firm 10.2% rate from 18.3% and that meant that exports contributed just 0.5 percentage points to GDP, half the 1.5 point add during the two prior periods. Real imports grew 13.1%, a very slight pickup from 10.5% growth during 2Q & 3Q. That sapped 0.1 points from GDP growth, the same as during the prior two quarters.

An improved foreign trade account added much less to real GDP growth last quarter. The 0.4 point addition was down from an average 1.4 percentage point contribution during the prior two quarters. Growth in exports slowed to a still quite firm 10.2% rate from 18.3% and that meant that exports contributed just 0.5 percentage points to GDP, half the 1.5 point add during the two prior periods. Real imports grew 13.1%, a very slight pickup from 10.5% growth during 2Q & 3Q. That sapped 0.1 points from GDP growth, the same as during the prior two quarters.

Financial Globalization and the U.S. Current Account Deficit from the Federal Reserve Bank of New York can be found here.

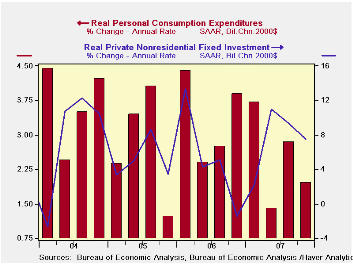

Growth in final sales to domestic purchasers totaled just 1.4%, down from a 2.3% rate of advance during the prior two quarters. The decline in residential construction at a -23.9% rate was an acceleration from a -16.3% rate during the prior two quarters. It was notable in that it pulled 1.2 percentage points out of GDP growth versus a 0.9 point lowering during 2Q & 3Q. The slowdown in growth in business fixed investment to a 7.5% rate from a 2 Qtr change of 10.2% also was notable in that it added a lesser 0.8 percentage points last quarter versus 1.0 points during the prior two. Growth in real personal consumption held fairly steady at a 2.0% rate of growth versus an average of 2.1% in 2Q & 3Q. That added 1.4 percentage points to growth last quarter in contrast to a 1.5 point add during the prior two.

The GDP chain price index rose 2.6% (AR), up from a 1.8% rate of advance during the prior two quarters. The PCE price index grew at a 3.9% rate. That was up a point from the prior two quarters not only due to higher energy prices. Less food & energy, a measure relevant to those who don't eat or drive, rose at an accelerated 2.7% rate versus an average 1.7% rate in 2Q & 3Q.

| Chained 2000$, % AR | 4Q '07 | 3Q '07 | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| GDP | 0.6 | 4.9 | 2.5 | 2.2 | 2.9 | 3.1 |

| Inventory Effect | -1.3 | 0.9 | -0.2 | -0.3 | 0.1 | -0.2 |

| Final Sales | 1.9 | 4.0 | 2.7 | 2.5 | 2.8 | 3.3 |

| Foreign Trade Effect | 0.4 | 1.4 | 0.8 | 0.7 | -0.1 | -0.2 |

| Domestic Final Demand | 1.4 | 2.5 | 1.9 | 1.8 | 2.7 | 3.3 |

| Chained GDP Price Index | 2.6 | 1.0 | 2.6 | 2.7 | 3.2 | 3.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief