Global| Mar 30 2006

Global| Mar 30 2006US 4Q GDP Little Revised at 1.7%, Profits Surged

by:Tom Moeller

|in:Economy in Brief

Summary

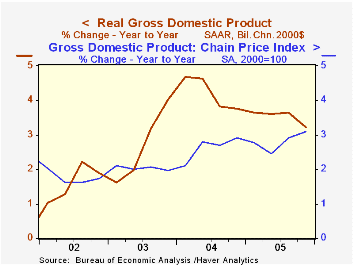

US real growth last quarter was revised up slightly, as expected, to 1.7% (AR) from the preliminary estimate of 1.6% and from 1.1% growth estimated two months ago. This quarter, growth is widely expected to bounce back with several [...]

Domestic demand was reduced during 4Q as personal consumption of motor vehicles & parts slumped 2.9% (-10.6% y/y). Lower auto consumption reduced real GDP growth by 1.9 percentage points but the GDP subtraction from lower auto output was limited to 0.6 percentage points as inventories built up. Overall, real PCE grew just 0.9% at an annual rate (2.9% y/y) during 4Q05, the slowest quarterly rate of growth in over ten years.

Defense spending is now estimated to have fallen 2.3% (+1.7% y/y) and that decline subtracted 0.4% percentage points from 4Q GDP growth.

The drag on GDP growth from a wider foreign trade deficit ballooned to 1.4 percentage points as imports grew 12.1% (AR, 5.3% y/y) while exports rose 5.0% (6.4% y/y).Countering the drag from foreign trade, inventories contributed 1.9 percentage points to GDP growth after more than a year of little or no positive contribution.

The chain price index grew 3.5%, an upward revision from the early estimate of a 3.0% rise. The upside surprise during 4Q was that the price index for private fixed investment grew 5.4% (AR, 3.7% y/y), inflated by an 8.3% (5.2% y/y) jump in residential and a 3.8% (2.8% y/y) rise in nonresidential fixed investment.

| Chained 2000$, % AR | 4Q '05 (Final) | 3Q '05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| GDP | 1.7% | 4.1% | 3.2% | 3.5% | 4.2% | 2.7% |

| Inventory Effect | 1.9% | -0.4% | -0.1% | -0.3% | 0.3% | 0.0% |

| Final Sales | -0.2% | 4.6% | 3.3% | 3.8% | 3.9% | 2.7% |

| Foreign Trade Effect | -1.4% | -0.1% | 0.0% | -0.1% | -0.5% | -0.3% |

| Domestic Final Demand | 1.1% | 4.5% | 3.3% | 3.9% | 4.4% | 3.0% |

| Chained GDP Price Index | 3.5% | 3.3% | 3.1% | 2.8% | 2.6% | 2.0% |

by Tom Moeller March 30, 2006

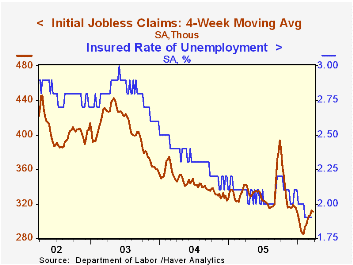

Last week, initial claims for unemployment insurance fell 10,000 to 302,000 from an upwardly revised level the prior period. The figure matched Consensus expectations.

Revisions raised the recent claims figures by roughly 10,000.

During the last ten years there has been a (negative) 75% correlation between the level of initial jobless insurance claims and the m/m change in payroll employment.

The four-week moving average of initial claims fell to 310,750 (-7.7% y/y).

Continuing unemployment insurance claims reversed most of the prior week's sharp drop, which was revised deeper, and rose 38,000 to 2.472M.

The insured rate of unemployment was stable at 1.9% for the sixth week.

| Unemployment Insurance (000s) | 03/25/06 | 03/18/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Initial Claims | 302 | 312 | -14.2% | 332 | 343 | 402 |

| Continuing Claims | -- | 2,483 | -4.4% | 2,663 | 2,924 | 3,532 |

by Carol Stone March 30, 2006

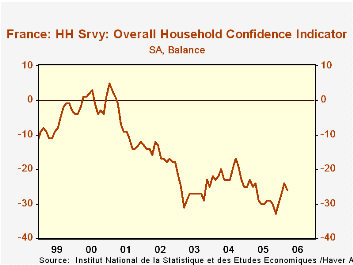

Labor policies are at the fore currently in France and Germany. France, as it tries to modify its basic "lifetime employment" work arrangements, faces massive riots by people at the other end of the economic spectrum -- who basically benefit from this policy -- from the young people who rioted last autumn because, due to this policy, they can't get a foot in the employment door. The government's proposal for a probationary employment period for young workers may sound good to these latter people, but it is not at all popular with current workers.

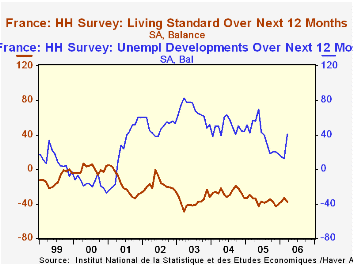

So today, the French statistics agency, INSEE, published the March household confidence survey. Does it show a reaction to these developments? Mildly so, and very specifically. The overall sentiment measure fell 2 points to -26 in March from -24 last month. These are both better than the November survey, in the midst of the labor disturbances; that figure was -33, down 3 points from October and the worst reading of the year, which averaged -28. So the current readings look "good" by comparison.

Two components showed some impact that may be related to these current disputes. Expectations about living standards fell 5 points this month to -38. In November, as well, this measure fell noticeably, to -43 from -37 in October. Expectations about unemployment also worsened each time: the new reading is +41 (meaning that 41% more people believe unemployment will increase than believe it will decrease), up sharply from February's +12. In November, by contrast, expectations about unemployment did not change from October's +20 value. Apparently, people see some fall-out from the government's current "probation" proposal, while they saw no implications from the November demonstrations.

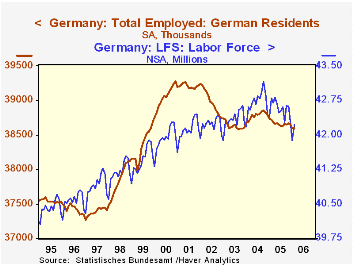

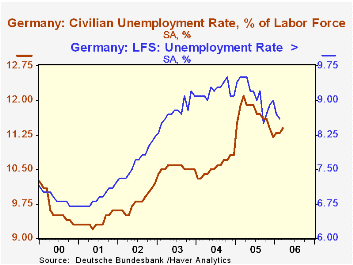

In Germany, the February labor force survey (LFS) was reported today, along with "registered" unemployment for March. In the LFS, employment remained stagnant, increasing a mere 5,000 from January's level; since mid-2003, the number of people employed has hovered in a narrow range around 38.6 million. Despite the flatness in the number of workers, unemployment rates have generally drifted lower. The rate according to the ILO definition, which is similar to that used in the United States, was 8.6% in February, down from 8.7% in January and from several months a year ago that were at or near 9.5%. The ILO definition is standard to all the Euro-Zone countries. The more widely watched local German measure, "registered" unemployment is also below year-ago levels, although it ticked up to 11.4% in the March report; its recent low was 11.2% in December. Government and private commentators attributed the March increase to cold weather, which has limited seasonal hiring for outdoor work. They anticipate a rapid rise in hiring as temperatures rise.

The combination of stagnant employment conditions and downtrends in unemployment rates is clarified through developments in the labor force as a whole. As seen in the accompanying graph, it is declining, and is down by about 1 million workers since late 2004. This allows reported unemployment to go down, even if employment is not going up.

Germany too wants to liberalize its labor laws, and its leaders are sensitive to the violent situation in France. While German business confidence rose sharply this month, as documented here earlier in the week by Louise Curley, its political leaders are waffling in the face of the dilemma the strong reaction causes them. Each of the accompanying economic reports thus takes on greater weight in view of the high political stakes.

| Mar 2006 | Feb 2006 | Jan 2006 | Year Ago | 2005 | 2004 | 2003 | |

|---|---|---|---|---|---|---|---|

| France: Overall Household Confidence (%) | -26 | -24 | -27 | -25 | -28 | -22 | -27 |

| Living Standard, Next 12 Mos. (%) | -38 | -33 | -37 | -34 | -37 | -27 | -38 |

| Unemployment, Next 12 Mos. (%) | +41 | +12 | +15 | +57 | +39 | +49 | +68 |

| Germany LFS | |||||||

| Employment (Mil.) | 38.604 | 38.599 | 38.719 | 38.668 | 38.779 | 38.631 | |

| Unemployment Rate (ILO) (%) | 8.6 | 8.7 | 9.5 | 9.1 | 9.2 | 8.8 | |

| "Registered" Unemployment (%) | 11.4 | 11.3 | 11.3 | 12.1 | 11.7 | 10.5 | 10.5 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief