Global| May 03 2007

Global| May 03 2007Upward Surprise on U.S. Productivity

Summary

Productivity mustered a larger gain than we had expected in Q1 but the trends still show productivity is on a deteriorating trend. Just as a refresher, recall that productivity is important because it governs the pace at which the [...]

Productivity mustered a larger gain than we had expected in Q1 but the trends still show productivity is on a deteriorating trend.

Productivity mustered a larger gain than we had expected in Q1 but the trends still show productivity is on a deteriorating trend.

Just as a refresher, recall that productivity is important because it governs the pace at which the economy can grow and it is an endogenous variable (one determined by the economic system not imposed upon it). Coupled with labor force growth, productivity sets the growth pace for the economy. Population growth is given to an economy. Labor force growth is the result of demographics (including population growth) tempered by economic decisions such as labor-leisure tradeoffs. Labor force growth can be augmented in small amounts by immigration. But the big variable that an economy controls that can alter its growth trends is productivity. All G-7 countries - indeed OECD countries and many developing nations - are seeing the same withering trend to population growth and advancing aging of the population. Slower population growth undercuts the base for growth in the labor force and therefore in the economy. Aging generally erodes labor force participation rates. So the key to keeping growth up is productivity.

A fading pace of productivity growth is bad news for a nation like the US with huge needs to pay for its national medical insurance program, a burdened Social Security system, an ample stock of debt already on the books plus running large current fiscal deficits. Aging will place more burdens on younger workers. Low productivity growth will only make hard choices even harder.

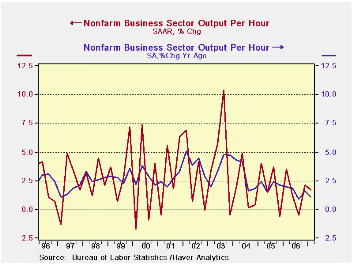

The trend to productivity growth is shown in the chart above using annualized quarterly changes as the red line and with the blue line guiding your eye to the predominant year/year trend. Despite quarterly volatility, the trend is clearly moving lower.

This a tough policy issue for the Fed and one it did not face under Greenspan since inflation fell and productivity rose keeping growth strong in a rare double win for policymakers that made Greenspan look as if he could walk on water. And indeed he can, but only when it is frozen. The problem for Bernanke is that the lake is warming up and he’s still in the middle. The Dilemma of Fed Policy

With the Fed having abandoned the V-G (Volcker-Greenspan) mantra that there is no inflation-growth conflict in the Fed’s mandate since low inflation boosts growth in the long run, the Fed is being forced into a bitter political dilemma. Should it to push for more growth as productivity fades or need it alter its inflation guideline? Congressman Frank continues to press the Fed to push for growth and to let wages rise. In dropping the old V-G approach to policy the Fed has fallen right into Frank’s trap.

This quarter’s numbers give the Fed some unexpected respite. While the GDP growth number is not good, productivity did revive more than expected. More helpful was the low 0.6% (annualized) rise in unit labor costs, that had been expected to be much higher. Now the trend in wage costs is much more up in the air, instead of clearly accelerating as it was previously. At 3.4% y/y (last quarter), unit labor costs were real threat to an inflation ceiling of 2%. At 1.3% (this quarter) the Fed again seems to have some breathing room. But make no mistake about it. This was a break for the quarter. Unless something changes, productivity is on a path to cause the Fed trouble. And evidence suggests that labor cost are still simmering. This quarter’s 2.3% rise in compensation costs comes after Q4’s rise of 8.5% making it hard to judge the trend. The Fed’s own recent Beige Book assessment of regional trends saw rather widespread pressure in the labor market despite this quarter’s beneficial reading in the productivity report. Quarterly numbers are volatile but the trends are telling.

| Year/Year Pct | 07/Q1 | 06/Q4 | 06/Q3 | 06/Q2 | 06/Q1 | 05/Q4 |

| Nonfarm Unit Labor Cost | 1.3% | 3.4% | 2.6% | 3.1% | 3.6% | 1.5% |

| Nonfarm Output/Hour | 1.1% | 1.6% | 0.9% | 1.9% | 2.0% | 2.1% |

| Nonfarm Comp/Hour | 2.4% | 5.0% | 3.5% | 5.1% | 5.7% | 3.7% |

| Nonfarm Real Comp/Hour | 0.0% | 2.9% | 0.1% | 1.0% | 1.9% | 0.0% |

| Manufacturing | ||||||

| MFG Unit Labor Cost | -2.0% | -0.5% | -2.3% | 0.1% | 2.0% | -1.2% |

| MFG Output/Hour | 3.6% | 3.9% | 4.2% | 3.6% | 4.1% | 4.6% |

| MFG Comp/Hour | 1.5% | 3.4% | 1.8% | 3.7% | 6.1% | 3.4% |

| MFG Real Comp/Hour | -0.9% | 1.4% | -1.5% | -0.3% | 2.3% | -0.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief