Global| Sep 11 2009

Global| Sep 11 2009University of Michigan Sentiment Makes Surprising Jump

Summary

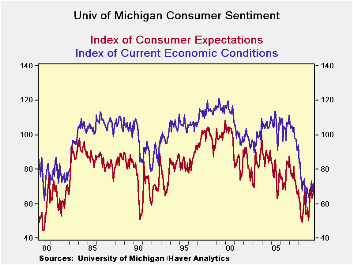

Consumer sentiment rose sharply to 70.2 in August in the U of M consumer sentiment preliminary report. The month’s rise in sentiment was the 42nd largest monthly rise out of the last 380 monthly changes. It was the fourth largest [...]

Consumer sentiment rose sharply to 70.2 in August in the U of

M consumer sentiment preliminary report. The month’s rise in sentiment

was the 42nd largest monthly rise out of the last 380 monthly changes.

It was the fourth largest monthly rise in the index in this

recession/recovery period. The current index rose sharply making the

second highest jump in this cycle. Expectations rose by 4.2 points

marking a solid rise that is the sixth largest gain for expectations in

this cycle. The move in August preliminary report is led by the

substantial gain in the current situation.

Still in terms of cycle levels the current situation is weak

standing at the 38Th percentile of its recession cycle range, while

expectations are just off their cycle peak reading of 70.8 (June 2009).

Both expectations and the current situation are some 30% shy

of their respective past cycle peaks. Still the day’s report represents

a sharp gain from the cycle lows and builds some well-needed momentum

into this report after a period of being mired below peak and sinking.

The consumer remains the key to this economic recovery since

there will be no investment of note until consumer spending picks up.

Exports which are doing well are simply too small to lead recovery.

Dropping imports are fools gold for growth since they only drop if

domestic demand is weak and that is the road to perdition not to crisis

contrition.

Near term we look, not inventory building, but to less cutting

to boost GDP growth. But that will not spur growth unless final sales

pick up requiring more restocking and spurring new rounds of hiring.

The consumer sentiment report may not dictate consumer spending

month-by-month. But the broad sweep of consumer moods do set the stage

for and reflect true changes in consumer spending habits.

In the month consumers have seen their personal finance

situation improve and the buying conditions are said to be the best in

three months and better than anything 15 months before that. It is an

important rise in this assessment. Importantly, expected business

conditions in the next 12 months are the best in 24 months.

This is a good solid report. As the back-to-school season

kicks in, the month of September is a key one for assessing how well

the economy is mending. So far it looks good.

| U of M Consumer Sentiment-Prelim | |||

|---|---|---|---|

| Sentiment | Current | Expectations | |

| Prelim | 70.2 | 71.8 | 69.2 |

| Last Month | 65.7 | 66.6 | 65.0 |

| Mo/Mo % | 6.8% | 7.8% | 6.5% |

| 2-Mos | 6.4% | 1.8% | 9.5% |

| Yr/Yr% | -0.1% | -4.3% | 3.0% |

| In Recession: Max,Min, Avg & Percentile | |||

| Max | 78.4 | 94.4 | 69.4 |

| Min | 55.3 | 57.5 | 49.2 |

| Average | 64.6 | 72.2 | 59.7 |

| Percentile | 64.5% | 38.8% | 99.0% |

| Cycle peak | 103.8 | 113.5 | 100.1 |

| % of Peak | 67.6 | 63.3 | 69.1 |

| U of M Consumer Sentiment-Prelim | |||

| Sentiment | Current | Expectations | |

| Max | 112.0 | 121.1 | 108.6 |

| Min | 51.7 | 57.5 | 44.2 |

| Average | 86.2 | 98.4 | 78.8 |

| Percentile | 30.7% | 22.5% | 38.8% |

| Rank % | 14.6% | 4.2% | 23.7% |

| Since January 1970 | |||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief