Global| Sep 30 2015

Global| Sep 30 2015Unemployment Rates Frozen at High Levels in Europe; Growth Frozen at Low Levels

Summary

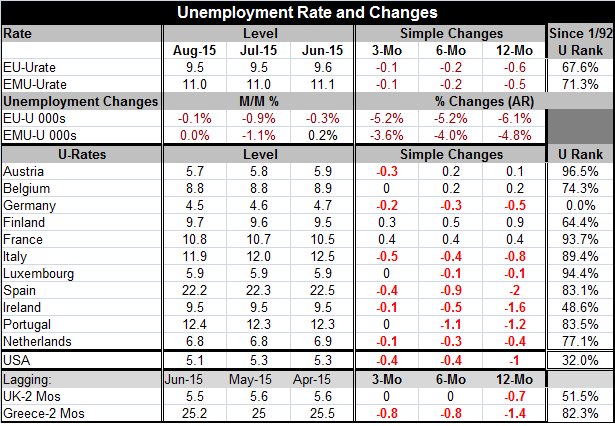

Europe gets another taste of deflation as its unemployment rate hangs high. European (EU) unemployment came in at 9.5% for the second consecutive month in August. In the EMU, the unemployment rate is lodged at a much higher level, at [...]

Europe gets another taste of deflation as its unemployment rate hangs high. European (EU) unemployment came in at 9.5% for the second consecutive month in August. In the EMU, the unemployment rate is lodged at a much higher level, at 11.0%. The EU rate is lower by 0.6 percentage points over 12 months while the EMU rate is lower by 0.5 percentage points over 12 months. Neither economic bloc is making a lot of progress on unemployment reduction. Now inflation has turned to deflation as Mario Draghi warned. EU unemployment sits at the 67th percentile of its historic queue of rates while EMU unemployment sits at its 71st percentile. Both economic groups have their respective unemployment rates at or near the top 30% of their historic queues of data. This is, of course, a number of years into what is supposed to be an economic recovery. This is not what recovery is supposed to look like.

Europe gets another taste of deflation as its unemployment rate hangs high. European (EU) unemployment came in at 9.5% for the second consecutive month in August. In the EMU, the unemployment rate is lodged at a much higher level, at 11.0%. The EU rate is lower by 0.6 percentage points over 12 months while the EMU rate is lower by 0.5 percentage points over 12 months. Neither economic bloc is making a lot of progress on unemployment reduction. Now inflation has turned to deflation as Mario Draghi warned. EU unemployment sits at the 67th percentile of its historic queue of rates while EMU unemployment sits at its 71st percentile. Both economic groups have their respective unemployment rates at or near the top 30% of their historic queues of data. This is, of course, a number of years into what is supposed to be an economic recovery. This is not what recovery is supposed to look like.

There is recovery in the EMU, however. You see it in Germany. The German unemployment rate stands at the lowest point in its queue of historic unemployment rates back to 1992. And the rest of the EMU is entirely different. While German has its lowest rate since at least 1992, only Ireland among the other EMU members has an unemployment rate below its median for that period as the Irish rate stands at its 48.6 percentile in its historic queue. After Ireland, Finland has the lowest unemployment rate, standing in the 64th percentile, followed by Belgium in its 74th percentile and the Netherlands in its 77th percentile. After that, all remaining members in the table have standings in their 80th or 90th percentiles. The U.S. by comparison has an unemployment rate in the bottom one third of its historic queue over the same period.

Not only are European unemployment rates largely high, there is still a good deal of divergence among them. We can look at the standard deviation of rates of unemployment across countries since 1992. We find that the divergence has been higher that it is now only about 20% of the time and all of that is in this cycle. The progress toward seeing less divergence has stopped as the standard deviation among rates of unemployment in August is the same as it was one year ago. Of course, divergence means that it is hard to run one monetary policy in this economic region which has only one central bank, the ECB.

Moreover, because most EMU nations have high levels of debt and relatively high deficits (Germany, of course, excluded) fiscal policy is not a tool that is available to address the differences within the EMU. This accounts for very slow progression of growth in the EMU and the lingering high rates of unemployment.

Of course, with the euro weak (and it fell again in the wake of the report that the EMU price level is now lower year-over-year and deflation has set in again), the EMU is hoping to be able to export itself to prosperity. At the recent G-20 meeting, finance ministers agreed not to pursue beggar-thy-neighbor policies of currency devaluation. But ongoing weakness in Europe and its current falling price level are again putting downward pressure on the exchange rate. In this weak growth environment, there is actually not much scope for a weak currency to provide a jolt of growth. Today the WTO announced its expectation that world trade would grow by only 2.8% this year, a miserably weak pace. It also said that the pace could be further reduced by a U.S. rate increase, China's economic slowdown or Europe's refugee crisis. That's right it did not name any factor that could cause an upside to its estimate.

With that we have poor prospects for global growth to stimulate anybody's exports. In Japan today the MOF seeing the weak trade environment and the unresponsive Japanese economy to extreme monetary stimulus warned against using deficit spending to boost the economy, looking back at how that had crippled the economy in the past.

Thus, what we have is a global mess. Growth is weak and not likely to see a virtuous circle come in the form of trade gains. In Europe, Japan and U.S. - all for different reasons - fiscal stimulus is out of the question. Monetary policy has been overused and seems to be no longer effective although Japan and Europe may yet step up their monetary stimulus. While the world has weak growth and conventional fiscal work-outs are off limits, the Federal Reserve in the U.S. is poised to raise rates to fight inflation- an inflation that seems a near impossible development in this environment. Europe and Japan both are suffering deflation. U.S. inflation is 0.3% year-over-year. Commodity prices are still weak and undermining many mining firms and others close to the commodities business. It would seem to be a time for stimulus rather than austerity. But that is not on the policy menu.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief