Global| Mar 01 2010

Global| Mar 01 2010Unemployment Rate Steadies In The Euro-Area .... But Not Much Else

Summary

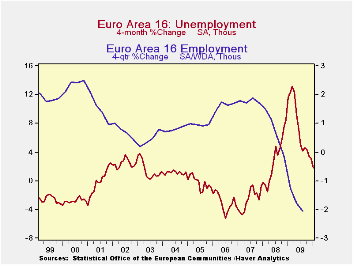

The unemployment rate in the Euro-Area has flattened out just under 10%. And while the number of unemployed continues to rise the increase is at a decreasing pace- a good sign or at least a logical first step. In the larger EU area [...]

The unemployment rate in the Euro-Area has flattened out just under 10%. And while the number of unemployed continues to rise the increase is at a decreasing pace- a good sign or at least a logical first step. In the larger EU area the pace of the increase in unemployment over three months is 1.9% well below the 5.4% pace over six months and 19.8% annual rate over the last 12-monhts.

EMU is doing better still. While all EMU countries are in the EU, the EMU set is a smaller group that shares a common currency, the euro. For this group the number of unemployed is rising at a 1.1% pace over three-months a 4.2% pace over six-months and a 16.4% pace over twelve-months. EMU unemployment is rising more slowly than in the EU over all these horizons.

Still the EMU’s Spain continues with a horrific 18.8 percent rate of unemployment as Spain’s property market boom and bust has proved to be very difficult to remedy.

The focus of attention in the Zone continues to be Greece with its ongoing problems. Talk from Germany and from the EU Commission continues to be tough. Greece says it needs help, not money. But the markets are improving and the euro itself is rising on rumors that some deal has been cooked up. It is hard to see how Greece can re-group without financial aid and perhaps some added credit backing. German and French banks already are greatly exposed to the Greek credit making them likely participants in a bail our or ‘assistance package’ for Greece. In any event it is clear that Europe does not want Greece to be the Lehman Brothers of Europe but they do want Greece to do more for itself so the pain is obvious to any other euro-member that might contemplate the same path that Greece took. Still, Europe does not want to let Greece go down and see what else is dragged into the resulting whirlpool. There are too many other potentially weak euro-members, enough that it could really stretch the ability of the monetary union’s strongest members to help them all. Holding the line on Greece is what makes the most sense. So look for a deal.

It is easier to do this in an environment, in which the economies are improving. With the slight nudge up to the market MFG PMI for the Zone today there is a new cycle high for the MFG index and reason for hope that he dig-out from recession continues. Sometime this week we should get some clearer news on the fate of Greece. The fat is in the fire and it is sizzling.

| Unemployment rate and changes | ||||||

|---|---|---|---|---|---|---|

| Rate | Level | Simple Changes | ||||

| Jan-10 | Dec-09 | Nov-09 | 3-Mo | 6-Mo | 12-Mo | |

| EU-Urate | 9.5 | 9.5 | 9.4 | 0.1 | 0.4 | 1.5 |

| EMU-Urate | 9.9 | 9.9 | 9.9 | 0.1 | 0.4 | 1.4 |

| Unemployment rate and changes | m/m% | Changes (ar) | ||||

| EU-U 000s | 0.6% | 0.7% | 0.6% | 1.9% | 5.4% | 19.8% |

| EMU-U 000s | 0.2% | 0.4% | 0.4% | 1.1% | 4.2% | 16.4% |

| U-Rates | Level | Simple Changes | ||||

| Germany | 7.5 | 7.5 | 7.5 | 0 | -0.1 | 0.3 |

| France | 10.1 | 10 | 10 | 0.2 | 0.6 | 1.4 |

| Spain | 18.8 | 18.9 | 18.9 | -0.2 | 0.4 | 3 |

| USA | 9.7 | 10 | 10 | -0.4 | 0.3 | 2 |

| Japan | #N/A | 5.1 | 5.2 | #N/A | #N/A | #N/A |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief