Global| Apr 22 2009

Global| Apr 22 2009UK Unemployment Continues To Soar (Sour)

Summary

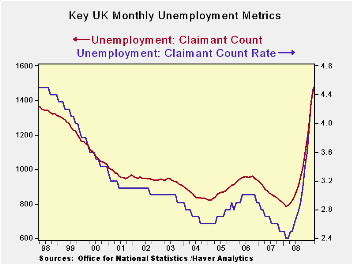

The UK claimant count and the unemployment rate continue to spurt higher. The count is the highest since the late 1990s (August 1998, for the percentage rate). Unemployment is skyrocketing. The number of unemployed persons rose m/m by [...]

The UK claimant count and the unemployment rate continue to

spurt higher. The count is the highest since the late 1990s (August

1998, for the percentage rate). Unemployment is skyrocketing. The

number of unemployed persons rose m/m by 6.6% in January, by an

outsized 10.9% in February, and by a slower but still bruising 5.3% in

March. Employment levels (available only through January) show

continuing accelerating declines.

The progressive growth rates (from 3Mo to 6Mo to 12Mo) show

accelerating rates of unemployment rising at an annualized rate of 140%

over the most recent 3-Mo period. Employment levels are dropping at an

accelerating pace which has risen to an annual rate of -1.7%. The

larger impact on unemployment growth comes about since employment

levels are high as a percentage of the labor force while unemployment

levels are low. When ‘small amounts’ are pared from the roles of the

employed they can quickly become a huge proportion of the unemployed.

Of course in historic context unemployment is hardly ‘small’ I simple

refer to ‘size’ as a proportion of the labor market and relative to the

‘employment rate’ which at over 95% is quite large compared to

unemployment at 4.5%. In that context the unemployment rate is ‘small’.

It is this size mismatch that results in most of the extreme difference

in growth rates for the employed Vs the jobless in addition to some

less mechanical labor behavior. (like labor force participation) .

In response to these worsening trends Alistair Darling

Chancellor of the exchequer has switched his budget forecast. He now

sees that the UK economy will shrink by 3.5% - the worst contraction in

modern times. The Darling also projects a deepening deflation with the

RPI gauge falling to minus 3% by September. But the forecast still

provides that the economy will begin to pick up by the end of the year,

with a moderate positive growth rate of 1.25% restored in 2010.

Darling has also announced help for jobless young people and a

car scrap-for cash scheme. A £2,000 stipend is to be paid to car owners

who trade in autos over 10 years in age for new ones. It is not clear

how much of this payment will be diverted to dealers who might offer

poorer trade-in prices and how much will actually get to the pocketbook

of those buying the new car and stimulate new purchases.

| UK job market trends | ||||||

|---|---|---|---|---|---|---|

| Level | Mar-09 | Feb-09 | Jan-09 | 3-mo Avg | 6-Mo | 12-Mo |

| Claimant count U-rate | 4.5 | 4.3 | 3.9 | 4.2 | 3.8 | 3.2 |

| U-Rate (Harmonized) | #N/A | #N/A | #N/A | 6.3 | 6.0 | 5.6 |

| % Period/Period | m/m | m/m | m/m | 3-Mo% AR | 6-Mo% AR | 12-Mo% AR |

| Unemployed (000)* | 5.3% | 10.9% | 6.6% | 140.4% | 134.2% | 84.9% |

| Employment (000)** | #N/A | #N/A | -0.4% | -1.7% | -1.0% | -0.8% |

| Note: Multi-Mo calculations are * lagged by three months; lagged by two-months | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief