Global| May 20 2010

Global| May 20 2010UK Trade Deficit Worsens As Exports Lag Imports

Summary

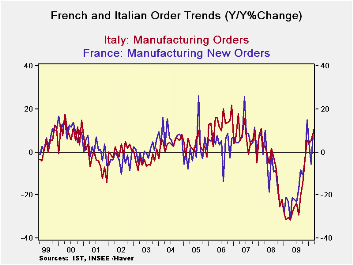

Orders growth has recovered substantially in Germany and in France. Despite the recovery in orders, with the rebounding rates of orders growth, the level of orders is still some 20% to 30% below their respective cycle highs for France [...]

Orders growth has recovered substantially in Germany and in France. Despite the recovery in orders, with the rebounding rates of orders growth, the level of orders is still some 20% to 30% below their respective cycle highs for France and Italy.

Germany posted some very strong orders. France and Italy, too, have posted some degree of orders strength in March. While France’s jump of 6.5% in one month seems very impressive (better than a 100% annual rate) orders in France still are rebounding from a 10.9% drop in January. As a result French orders are still falling on balance over three-months even with this strong monthly rebound. So are orders in Italy.

Europe is certainly due for some kick to growth as the euro has fallen over the past year and plunged sharply over the past few months. But the persisting weakness in European stocks speaks to a loss of confidence. In part the Greek stimulus plan is not fully funded and is awaiting some final votes from Germany to disburse funds. In part it is the still uncooperative tone in Greece where further strikes are planned to protest austerity. In part it is due to concern that, despite all the reluctance to obey the rule of austerity, the fiscal consolidation will prove to be too great to allow European growth to press ahead.

It is these two conflicting ideas that are driving markets into a frenzy, even though they are at odds with each other. Which is it? Are countries going to avoid austerity and not do the right thing? Or, are countries going to be so virtuous with fiscal controls that consolidation will prove to be a load too-heavy and cause growth to be set back? Or is there a middle ground with a more positive result? We have seen recent improvements in the US and European economic reports. Reports with expectations components have shown some of the weakest recent readings. Barometers of current activity have been strong, especially in the UK just outside the Euro-Area

I think we are in a region of political economic uncertainty. Markets are not happy with the stewardship of our political or economic direction in recent years. The private sector has failed us too. It is no wonder that markets feel like taking no prisoners. But it’s also true that at the end of the day the markets know that stock indices have come a long way from their recession bottoms, that interest rates had crept up and are now lower as a result of this sell-off, that central banks are not eager to tighten but are planning to discharge their responsibilities, that – at the end of the day- inflation has remained under wraps. The blow-off in commodity prices that had run well ahead of reality is a welcome event (unless you were long, of course). As we go over the final technical hurdles to get money to Greece (and to thereby protect exposed German and French banks with Greek paper on their balance sheets) we can expect things to settle down and for markets to pay attention of fundamentals again. It’s not just pabulum from a policymaker looking to calm markets. It’s true. The fundamentals are good. Even with the high debt-to-GDP levels the problems are tractable.

| Italy Orders | ||||||

|---|---|---|---|---|---|---|

| Saar exept m/m | Mar-10 | Feb-10 | Jan-10 | 3-mo | 6-mo | 12-mo |

| Total | 1.0% | -0.4% | -2.8% | -8.7% | 12.7% | 9.1% |

| Foreign | 1.8% | -0.5% | -2.3% | -4.1% | 22.0% | 21.4% |

| Domestic | 0.4% | -0.2% | -3.1% | -11.1% | 7.7% | 3.0% |

| Memo | ||||||

| Sales | 1.5% | -2.6% | 2.6% | 6.2% | 8.3% | 6.3% |

| French Orders | ||||||

| Saar exept m/m | Mar-10 | Feb-10 | Jan-10 | 3-mo | 6-mo | 12-mo |

| Total | 6.5% | -1.0% | -10.9% | -22.4% | 2.2% | 10.6% |

| Foreign | 2.9% | 1.0% | -8.7% | -19.1% | 26.7% | 28.9% |

| IP xConstruct | 0.8% | 0.3% | 0.6% | 7.0% | 3.7% | 6.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief