Global| Jul 18 2013

Global| Jul 18 2013UK Retail sales stay off to the races

Summary

Retail sales in the United Kingdom edged higher by 0.2% in June after surging by 2.1% in May. The May rise more than offsets a 1.3% drop in April. Putting the tangled trail of retail sales together still leads the UK to a 4.1% growth [...]

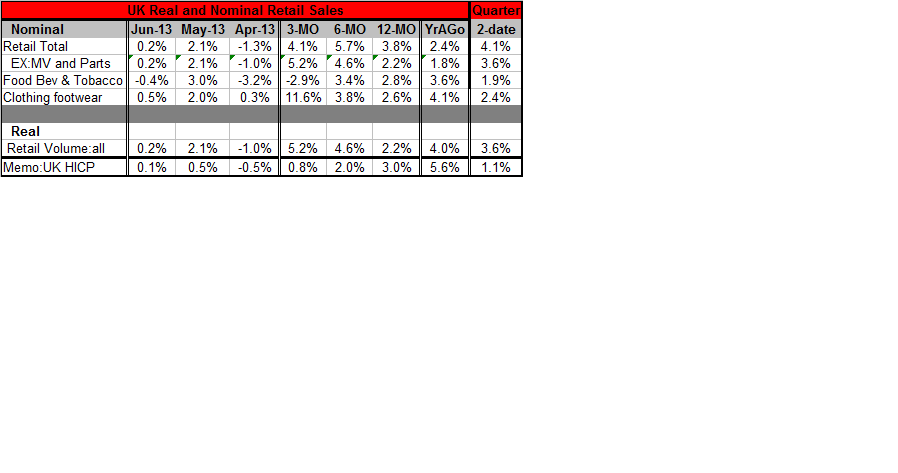

Retail sales in the United Kingdom edged higher by 0.2% in June after surging by 2.1% in May. The May rise more than offsets a 1.3% drop in April. Putting the tangled trail of retail sales together still leads the UK to a 4.1% growth rate in nominal retail sales over three-months compared to 5.7% over six-months and 3.8% over 12 months. Growth in the recent 12 month period, at 3.8%, is exceeding growth in the previous 12 month period which was 2.4%. Clearly there is an acceleration in retail sales of some sort or, a somewhat worse case, a stabilization of retail sales at a growth rate somewhere between 4% and 6%, but well above 2.4%. Neither of these outcomes is bad.

Retail sales in the United Kingdom edged higher by 0.2% in June after surging by 2.1% in May. The May rise more than offsets a 1.3% drop in April. Putting the tangled trail of retail sales together still leads the UK to a 4.1% growth rate in nominal retail sales over three-months compared to 5.7% over six-months and 3.8% over 12 months. Growth in the recent 12 month period, at 3.8%, is exceeding growth in the previous 12 month period which was 2.4%. Clearly there is an acceleration in retail sales of some sort or, a somewhat worse case, a stabilization of retail sales at a growth rate somewhere between 4% and 6%, but well above 2.4%. Neither of these outcomes is bad.

Excluding motor vehicles and parts the acceleration in retail sales is clearer. On that metric sales are up at a 5.2% annual rate over three months 4.6% over six months and 2.2% over 12 months. Food, beverage and tobacco sales have weakened somewhat in the recent three months, but the clothing and footwear purchases have accelerated sharply over the recent three months.

Retail sales volumes also tell a story of acceleration. Over three months retail volumes are up at a 5.2% annual rate compared with 4.6% annual rate over six months and 2.2% over 12 months. UK economy seems to be finding its legs.

Of course there are other signs of progress. The number of Britons claiming jobless benefit allowances posted the steepest decline in three years in June; the claimant count came in at 1.48 million down by 21,200 on the month. That was the largest drop since June 2010. And, while European auto sales have been carving out a 17 year low, car production in the UK continued to advance on increased demand in both the local and the export market as car production UK is up by 10.4% year-over-year.

Looking at the what-have-you-done-for-me-lately metric, the behavior of sales in the current quarter, where data have just come in for June to complete the quarterly picture, we see retail sales running at a 4.1% annual rate in nominal terms and 3.6% in real terms. That nominal increase of 4.1% is reduced to 3.6% when we look at retail sales excluding motor vehicles and parts.

On balance UK sales are slightly weaker in real terms in the second quarter than they been over three months and over six months. Still, the 3.6% rate of increase is quite solid. It is buttressed by firm trends outside of motor vehicles and by performance in terms of demand for automobiles that has come from both inside and outside the United Kingdom. Of course, external demand does not boost UK retail sales but it boosts the UK economy overall and indirectly supports UK economic growth and demand. The recent plunge in jobless claims seekers is clearly good news for the labor market and potentially for income growth prospects as well. However, optimism on the UK needs to be tempered by the fact of its close association with countries in the euro-Zone where demand overall is flagging, economic growth is challenged, where domestic demand is weak, and where there is a good deal of political turmoil still in train.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief