Global| Apr 25 2014

Global| Apr 25 2014UK Retail Sales Continue to Climb

Summary

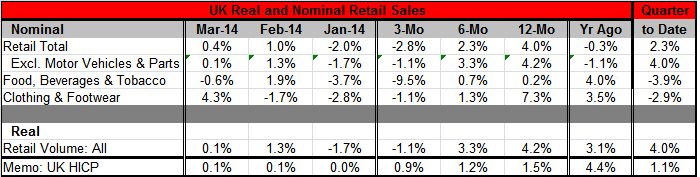

UK retail sales rose by 0.4% in March, building on a 1% increase in February. However, these gains are not enough to offset January's 2% decline, leaving the three-month growth rate at a -2.8% annual rate. That result is repeated for [...]

UK retail sales rose by 0.4% in March, building on a 1% increase in February. However, these gains are not enough to offset January's 2% decline, leaving the three-month growth rate at a -2.8% annual rate.

UK retail sales rose by 0.4% in March, building on a 1% increase in February. However, these gains are not enough to offset January's 2% decline, leaving the three-month growth rate at a -2.8% annual rate.

That result is repeated for retail sales excluding autos as March sales rose by 0.1% following February's 1.3% gain; but those gains fail to make up for January's 1.7% drop; the three-month growth rate is left at a -1.1% annual rate of decline.

Both the total and the ex-motor vehicle readings on retail sales in the UK show progressively weaker growth rates from 12 months to six months to three months. Annual sales are still at a relatively high pace and have come a long way since early 2013. While the progressive growth rates seem to show an ongoing slowdown from 12 months to 6 months to 3 months, the intra-quarterly pace shows a slightly different result. January was a weak month, with a deep decline in sales, but February and March continued to pose gains after falling into that pothole. It is not at all clear what the trend will emerge for UK retail sales.

The two components, clothing & footwear plus food, beverages & tobacco, show the same decelerating sequential growth rate patterns with the same sort of contrary intra-quarterly trend. Expressed in real terms, retail sales patterns basically show the same trends and raise the same questions.

The UK has been a strengthening economy and its retail sales chart shows that. Sales have swept up very sharply and have backed off in early 2014, but still log a relatively strong rate of spending on the year. UK auto registrations continue to be strong, one of the most consistent sales markets in Europe. On the fiscal side, the government has hit its fiscal objectives. Despite ongoing financial sector issues, UK has managed to post strong growth rates without resorting to fiscal excess.

I prefer to focus on the still strong year-over-year growth rates in this report and on the intra-quarterly pattern that shows some resilience by consumers following a January shutdown. The complete exit from winter as the UK gets into the spring and summer months will show more clearly what the patterns will dominate retail spending. The last two months together give us a positive assessment of retail trends, but the longer-term trends back of the past year not to be ignored. UK is at a bit of a decision point. Are trends in UK retail sales shifting? That's the question that will be answered over the coming months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief