Global| Aug 21 2013

Global| Aug 21 2013UK Orders and Expected-Orders Show Strength

Summary

Despite some lingering skepticism, the UK economy continues to register strong readings and in some cases fabulously strong readings. The Confederation of British industry, or (CBI), survey shows exceptional order strength in August. [...]

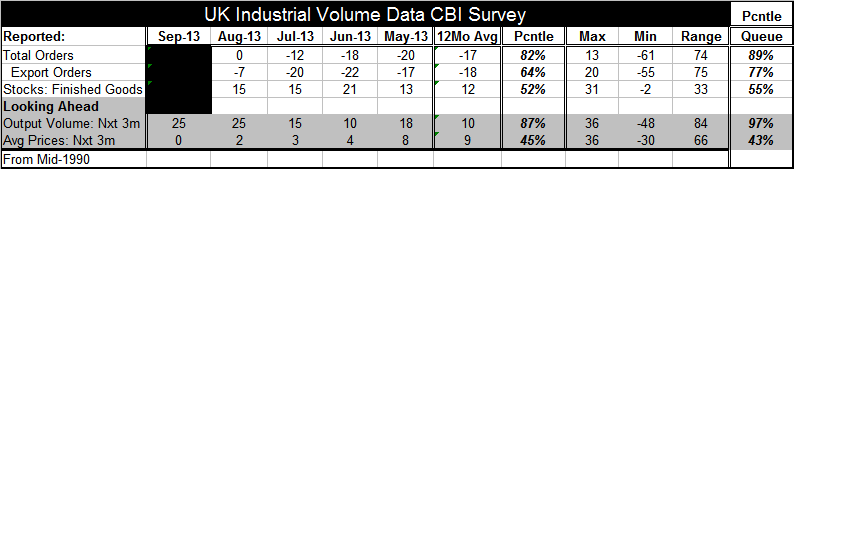

Despite some lingering skepticism, the UK economy continues to register strong readings and in some cases fabulously strong readings. The Confederation of British industry, or (CBI), survey shows exceptional order strength in August. Technically the diffusion value does not look very strong, as the August value for orders is only zero- in the diffusion index lexicon that indicates neutrality for orders with the expectations for increases washing out the expectations for decline. But, with diffusion indices what you see may not be what you get -- as I have argued for some time-and THIS is a prime example of that effect. Virtually ALL the news stories play this as a strong report and RIGHTLY SO. It is strongest order reading since August 2011. And it's a reading in the context of its historic queue that is within the top 11% of all historic readings. This is another case where the actual diffusion value seems to have less meaning than the placement of the value in its historic queue. Similarly, exports orders at -7 have improved sharply from -20 in July. The level for export orders in August sits in the 77th percentile or top 23% of its historic queue. Stocks of finished goods register a +15 which is a middling, 55th percentile historic standing by that metric.

Despite some lingering skepticism, the UK economy continues to register strong readings and in some cases fabulously strong readings. The Confederation of British industry, or (CBI), survey shows exceptional order strength in August. Technically the diffusion value does not look very strong, as the August value for orders is only zero- in the diffusion index lexicon that indicates neutrality for orders with the expectations for increases washing out the expectations for decline. But, with diffusion indices what you see may not be what you get -- as I have argued for some time-and THIS is a prime example of that effect. Virtually ALL the news stories play this as a strong report and RIGHTLY SO. It is strongest order reading since August 2011. And it's a reading in the context of its historic queue that is within the top 11% of all historic readings. This is another case where the actual diffusion value seems to have less meaning than the placement of the value in its historic queue. Similarly, exports orders at -7 have improved sharply from -20 in July. The level for export orders in August sits in the 77th percentile or top 23% of its historic queue. Stocks of finished goods register a +15 which is a middling, 55th percentile historic standing by that metric.

Expectations this month are also rather robust. Output volume expected over the next three months registers a +25 in September the same as in August. In August that number had moved up from plus 15 in July, so there is a little bit of a legacy of strength and growing momentum here. The reading of +25 is a 97 percentile or top 3% reading in the history of this particular statistic. The reading for expected prices three months ahead is at zero; that is a 43rd percentile reading, below its historic median. It is somewhat unusual for the forward orders metrics to continue to get stronger as the forward price expectations metric continues to get weaker but that's exactly what the survey is telling us.

Much of the strength logged by the CBI reading is recent. The month-to-month change in orders is the 16th largest month-to-month increase in the last 250 months- that's better than 20 years. The four-month change which sees orders move to zero from a reading of -25 in April is unprecedented over the interval; it is the largest four-month net gain in the history of the statistic. Export orders have been a big part of the strength as their month-to-month change of +13 ranks as the ninth largest increase in the history of that series on the same time-line.

The UK is an interesting case to watch because it has its own dynamics in politics plus its own currency and central bank yet it is importantly linked into the economies of the European Monetary Union through trade. The UK current orders, export orders and expected output volume all speak to strength. And while the UK also has the US is an important trading partner, it's hard to imagine it posting this kind of strength if Europe were not doing better as well. And, of course, the European data have been showing improvement as we saw from the recent positive GDP growth figure for the European Monetary Union in 2013-Q2. While we continue to get mixed readings for the various countries of the Monetary Union UK exports only need to find enough pockets of strength to show improvement. The message from the UK industrial survey is that whatever stirring is going on in the Monetary Union it appears to be somewhat broad-based despite the clear irregularity being posted by the economic statistics.

This report on the UK fits in with other positive readings we've seen ranging from the UK services sector to the housing market to UK GDP. However as we know, the UK is importantly linked to the European economy and despite the fact that it's doing better, German finance Minister Wolfgang Schaeuble just today has added his voice to the chorus before him that has said that Greece is going to need another bail out. Were that to happen we would certainly have to wonder what else might come unglued in the Monetary Union. Such events usually have repercussions. For the time being, the UK figure fits in with the notion of an upswing in Europe. We have an increasing number of people getting more optimistic on Europe's fortunes. And I see no reason to be opposed to this short-term optimism although I caution that a more guarded viewed needs to take hold as we approach the period for the German elections. Too many European economies simply have too many problems to think that they can continue to move ahead and steamroll over them ignoring their pressing needs. Therefore, I do view the situation in Europe as a bounce rather than as indication that all is on the mend. Time will tell on that judgment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief