Global| Mar 19 2008

Global| Mar 19 2008UK Order Books are "Full".…but for How Long?

Summary

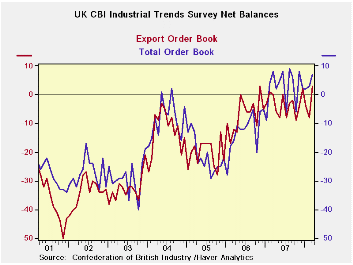

UK order books are high, in the 96th percentile of their range of values since end-2000 in terms of the net balance readings of the CBI survey. Total orders are strong and exports are the highest seen in this seven-plus year period [...]

UK order books are high, in the 96th percentile of their range of values since end-2000 in terms of the net balance readings of the CBI survey. Total orders are strong and exports are the highest seen in this seven-plus year period Output volume expected in the next 3-months is more restrained but still resides in the top 18 percent of its range (100-82=18). Stocks of product are mid range, neither too high nor too low. Price expectations will not be good news to the BOE. Prices expected in the next 3-months are the highest net balance we have sense in this period at +25, up sharply from +22 in February and average expectations of +18 over the past year.

In analyzing these trends one thing to consider is the recent choppiness of recent movements. The export order jump month-to-month lifted export orders to the top percentile of the seven plus year range from its top 20th percentile reading last month. Output volume expected jumped from the 70th percentile of the range last month to the 82nd percentile (top 18%). So before we celebrate we need to recognize that the UK industrial sector is doing better, but that the monthly readings are volatile. The one exception might be for expected prices where the monthly gains have been large and steady. It is not clear that the UK industrial sector is as strong as a top of range reading makes it seem. The chart makes it clear that there has been some recovery but that the net positive readings are relatively moderate despite their relative range position that the order readings have posted. For the most part these readings are moving sideways and are not pointing to an acceleration that might signal overheating. Still the price component is a bit unsettling.

| UK Industrial volume data CBI Survey | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Reported: | Mar-08 | Feb-08 | Jan-08 | Dec-07 | 12Mo Avg | Pcntle | Max | Min | Range |

| Total Orders | 7 | 3 | 2 | 2 | 3 | 96% | 9 | -40 | 49 |

| Export Orders | 3 | -8 | -4 | 2 | -4 | 100% | 3 | -50 | 53 |

| Stocks: Final Goods | 12 | 11 | 7 | 14 | 10 | 50% | 26 | -2 | 28 |

| Output Volume: Next 3-months | 11 | 11 | 9 | 3 | 13 | 70% | 28 | -28 | 56 |

| Avg Prices 4 Next 3-months | 25 | 22 | 21 | 15 | 18 | 100% | 25 | -30 | 55 |

| From end 2000 | |||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief