Global| Jul 09 2013

Global| Jul 09 2013UK Manufacturing in a Surprising Slump

Summary

UK manufacturing took an unexpected sharp turn lower, falling by 0.8% in May. The climb was led by a sharp decline in consumer goods output which fell 2.9% on the month; that made it the second consecutive monthly drop. Capital goods [...]

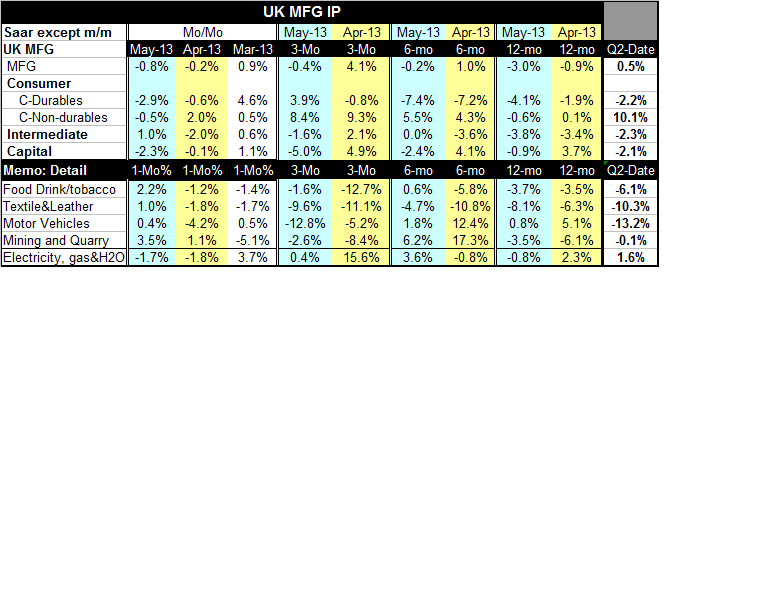

UK manufacturing took an unexpected sharp turn lower, falling by 0.8% in May. The climb was led by a sharp decline in consumer goods output which fell 2.9% on the month; that made it the second consecutive monthly drop. Capital goods output fell by 2.3% and also made its second consecutive monthly drop. Consumer nondurables output slipped by 0.5% in May.

UK manufacturing took an unexpected sharp turn lower, falling by 0.8% in May. The climb was led by a sharp decline in consumer goods output which fell 2.9% on the month; that made it the second consecutive monthly drop. Capital goods output fell by 2.3% and also made its second consecutive monthly drop. Consumer nondurables output slipped by 0.5% in May.

In terms of trends, manufacturing is now declining over three months at a 0.4% annual rate compared to -0.2% over six months and -3% over 12 months. The difference between the three of the six month rates of change is not really enough to say that manufacturing output is decelerating again. So there still seems to be progress compared to the year-over-year pace of -3%. That's something, at least.

Looking at the details, despite the sharp monthly drop, consumer durables output is up at a 3.9% pace over three-months; this is sharply better than the -7.4% over six months and the -4.1% over 12 months --clear improvement there. Consumer nondurables show a steady rate of improvement at an 8.4% annual rate over three months, up from 5.5% over six-months and -0.6% over 12 months- another clear case of improvement. The trend for intermediate goods output seems to be showing some improvement, too. Intermediate goods output rose by 1% in May after falling by 2% in April. Over three months it's falling at a 1.6% annual rate; it's flat over six months; year-over-year output for intermediate goods is down at a 3.8% annual rate. While the sustainable trend may be hard to identify for intermediate goods, clearly it is less-weak over three months than it has been over 12 months. Capital goods is the real fly in the ointment for UK output; capital goods output fell sharply in May and now is down at a 5% annual rate over three-months, steeper than its 2.4% slide over six-months which is weaker than it 0.9% rate of decline over 12 months- that's very clear deterioration. And capital goods looks to service future demand, not current demand as is the case for nondurable goods.

"Capital goods" is the category within the European monetary Zone that had seemed to show the most firmness (in output) for countries there, especially for Germany. German IP shows a sharp drop in output in May but strongly accelerating growth rates from 12-months to 3-months culminating in an annual rate of output growth of 12.7% for capital goods for the three-months ended in May. This not the UK experience at all. But for the UK what we see is the opposite clear pattern of building weakness for capital goods.

If we look at the quarter to date data which is updated through May (therefore, it reflects hard data for two of three months in the quarter) capital goods and consumer goods output are both falling at just about a 2.2% annual rate in the quarter with intermediate goods output falling at a 2.3% annual rate in the quarter; consumer nondurables lessens the blow on manufacturing output by rising at a huge 10% annual rate in the new quarter. That actually is strong enough to pull the overall quarterly output for manufacturing up to a +0.5% annual rate in Q2-to-date!

However, utilities output is responsible for helping to weaken the overall IP trend in the last two months after a surge in output in March. In manufacturing, the food and drink sector's output was up in May as was motor vehicle output. Textile and leather output was up as well as was output in mining & quarrying; each of these latter two sectors showed output up for two months in a row. But upbeat sector stories do not change the headline trend.

A holiday shift of one day to June from May to cluster holidays into the Queen's Diamond Jubilee celebrations of last year had the effect of bulking up by one day the working days for the month of May making the year over year comparison a sterner test in 2013. Still, this does not seem to be an import driver of the current trends in IP nor does it erase any recent question marks.

Despite this weakness in output, in a new development, just announced today, the International Monetary Fund has just lifted its economic growth projection for the UK for the current calendar year. The growth rate is bumped up from 0.7% to 0.9%. This is the first time since April 2012 that the IMF has actually increased its forecast for growth in United Kingdom. However, in April The Fund had cut its forecast of growth from 1% to 0.7% so despite the upgrading, growth it still seen as weaker than what the IMF had been looking for back in April.

There has been some improvement in UK business optimism and an ongoing advance in the housing market including firmer prices. UK housing demand is at a four year high according to a new metric issue is the Royal Institute of Chartered Surveyors. Still the UK remains challenged for growth. The components of its industrial production survey are not exactly reassuring.

The IMF growth upgrade comes at a time that it is also downgrading global growth. The UK will have a hard time improving its economy based on its export sector and the sort of external demand it will face in its export markets. The improved IMF outlook also comes amid somewhat more encouraging assessments by the Markit PMI gauges for the UK MFG and Services sectors. But that is part the point of the consternation over the performance of industrial output. The PMI gauges and the UK output ("real data") trends are different. The pound reacted badly to the release of industrial output. Still the UK trade gap was slightly improved in May as exports just barely outpaced imports. UK exports were helped along by strong shipments from the petroleum sector. It's hard to conclude that improved trade performance means that competiveness is maintained and that the output fall reflects weak demand. UK trends remain too conflicted to perform any detailed economic forensic work. Too many questions and contrary trends remain.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief